Cullen/Frost Bankers (CFR) Faces A Valuation Test After Mixed Analyst Calls

Cullen/Frost Bankers, Inc. CFR | 0.00 |

Cullen/Frost Bankers (CFR) is back in focus after its removal from the Russell 1000 Dynamic Index, alongside mixed analyst reactions that highlight differing views on valuation and future risks for the regional bank stock.

Cullen/Frost Bankers shares trade at US$154.86, with a 30 day share price return of 10.49% and year to date share price return of 20.82%, while the 5 year total shareholder return of 65.68% points to solid longer term wealth creation despite recent index removal and mixed analyst views.

If you are assessing how other parts of the market are responding to shifting sentiment around financials, it can be useful to broaden your watchlist to include 20 top founder-led companies

With Cullen/Frost Bankers trading slightly above one analyst target yet flagged by others for a premium valuation, the key question for you is simple: is there still hidden value here, or is the market already pricing in future growth?

Most Popular Narrative: 2.9% Overvalued

Cullen/Frost Bankers last closed at $154.86 against a narrative fair value of $150.47, so the widely followed model sees only a small valuation gap driven by specific assumptions on growth, margins and capital returns.

The full payoff from the branch expansion strategy is approaching, with maturing branches in high-growth markets shifting from breakeven to accretive by 2026, which will unlock operating leverage and drive faster bottom-line growth relative to the past three years.

Want to understand why this narrative is comfortable with a richer earnings multiple, modest growth forecasts and ongoing buybacks at today’s price? The numbers behind that balance are all in the full narrative.

Result: Fair Value of $150.47 (OVERVALUED)

However, this Cullen/Frost Bankers narrative still relies on branch expansion becoming more profitable and deposit costs remaining contained, and either assumption could easily be tested.

Another View: Cullen/Frost Bankers and the DCF Gap

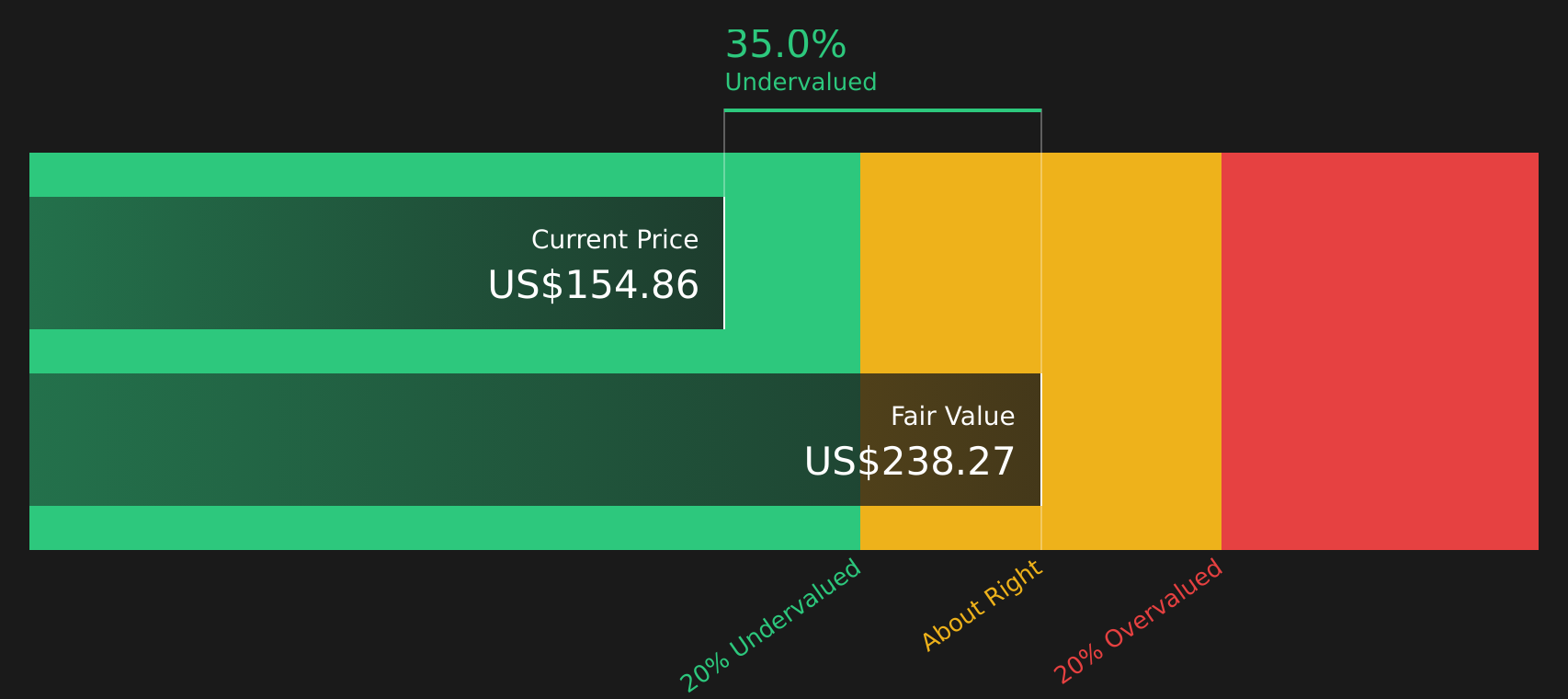

While the analyst narrative suggests Cullen/Frost Bankers is close to fair value at US$150.47, the Simply Wall St DCF model presents a different picture, with a future cash flow value of US$238.27. That implies the stock is trading at roughly a 35% discount. This raises the question of which measure is more persuasive: the view based on cash flows or the one based on the current earnings multiple.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cullen/Frost Bankers for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of fair value estimates and future assumptions regarding Cullen/Frost Bankers leaves you undecided, quickly review the complete picture and consider the 3 key rewards.

Looking for more investment ideas beyond Cullen/Frost Bankers?

If Cullen/Frost Bankers has sharpened your thinking, do not stop there. Use the Simply Wall St Screener to uncover more stocks that fit your approach.

- Target income resilience by reviewing 7 dividend fortresses that may support steadier cash flows when markets turn choppy.

- Spot potential bargains early by scanning screener containing 18 high quality undiscovered gems before they sit firmly on everyone else's radar.

- Prioritize capital preservation by focusing on 74 resilient stocks with low risk scores so you are not the one chasing story stocks after the move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.