Dave (DAVE) Raises 2025 Revenue Outlook After Strong Quarter Is Execution Matching Investor Expectations?

Dave, Inc. Class A DAVE | 172.70 | -0.43% |

- Dave Inc. recently raised its revenue guidance for the 2025 fiscal year to US$505 million–US$515 million and announced second quarter results showing year-over-year increases in both revenue and net income.

- The updated guidance and robust quarterly performance highlight strengthened business momentum, suggesting increased confidence in operational execution and the demand for Dave’s digital banking offerings.

- With Dave’s revised outlook pointing toward higher expected revenues, we'll explore how this new guidance influences the company’s broader investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Dave Investment Narrative Recap

To be a shareholder in Dave Inc., you need to believe in the sustained adoption of digital banking services, strong growth in user engagement, and the company’s ability to monetize its membership and ExtraCash offerings. The recent boost in 2025 revenue guidance suggests near-term momentum by confirming robust demand as the key catalyst, yet the primary risk of regulatory scrutiny or fee limitations on short-term advance products remains unchanged and material for now.

Of the recent announcements, the raised revenue guidance for 2025 to US$505 million–US$515 million is most relevant, reinforcing the business’s accelerating top-line growth. This update, following a quarter of strong year-over-year gains in both revenue and net income, directly supports the belief in Dave’s ability to drive efficient growth through monetizing its digital platform.

By contrast, investors should remain attentive to the possibility that regulatory changes affecting small-dollar, fee-based products could shift profit expectations...

Dave's outlook projects $685.4 million in revenue and $224.2 million in earnings by 2028. This requires 16.5% annual revenue growth and a $169 million increase in earnings from current earnings of $55.2 million.

Uncover how Dave's forecasts yield a $271.00 fair value, a 45% upside to its current price.

Exploring Other Perspectives

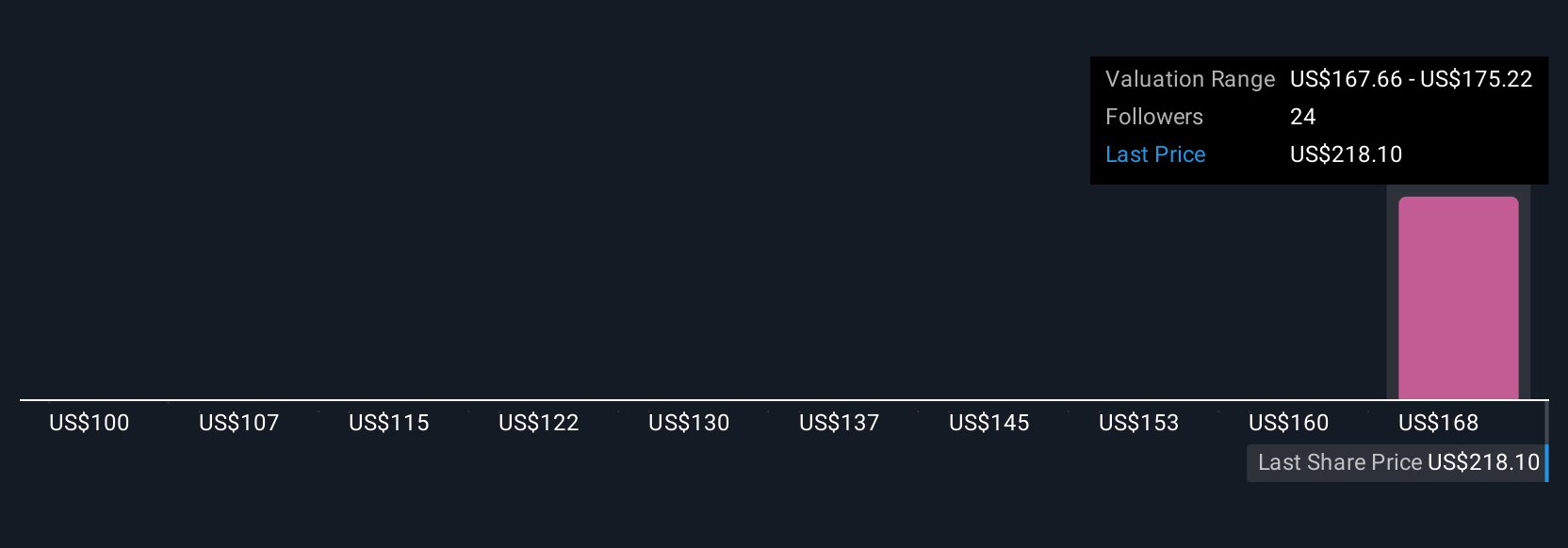

Four Simply Wall St Community members estimated Dave Inc.’s fair value in a wide range from US$99.65 to US$320. With opinions spread across ten buckets, this diversity stands out while regulatory uncertainty about fee models continues to shape the overall outlook for the company. Explore multiple viewpoints and see how your perspective compares.

Explore 4 other fair value estimates on Dave - why the stock might be worth 47% less than the current price!

Build Your Own Dave Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Dave research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dave research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dave's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.