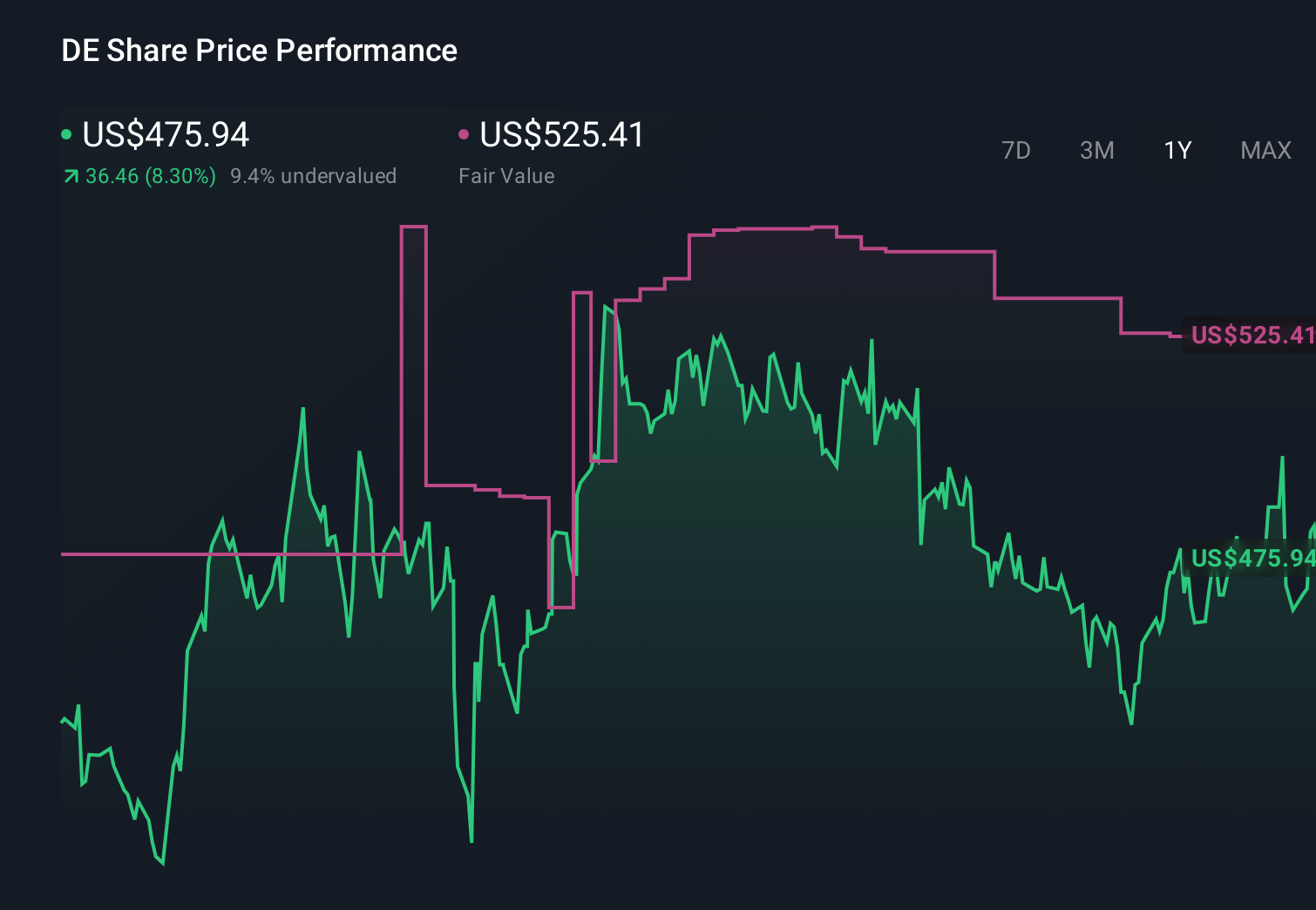

Deere (DE) Is Down 5.8% After Profit Mix Shifts Away From Large Ag Equipment - Has The Bull Case Changed?

Deere & Company DE | 0.00 |

- In May 2026, Deere & Company reported fiscal second-quarter results showing revenue rising to US$13.37 billion while net income eased slightly to US$1.77 billion, and reaffirmed full-year 2026 net income guidance of US$4.5 billion to US$5.0 billion.

- Beneath the headline beat on earnings per share, performance tilted away from large agricultural equipment toward faster-growing Construction & Forestry and Small Agriculture & Turf, highlighting how Deere’s profit mix is shifting as farm markets soften.

- We’ll now examine how this mix shift toward Construction & Forestry and ongoing pressure in large agriculture could reshape Deere’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Deere Investment Narrative Recap

To own Deere, you need to believe its mix can shift from cyclical large agriculture toward more stable, higher-margin Construction & Forestry and Small Ag & Turf, while precision technology deepens customer ties. The latest quarter broadly supports that view: construction strength and reaffirmed full year net income guidance of US$4.5 billion to US$5.0 billion help the near term story, even as the biggest current risk remains persistent weakness and pricing pressure in large ag and tariff driven cost inflation.

The most relevant update here is Deere’s May 2026 reaffirmation of its full year net income outlook at US$4.5 billion to US$5.0 billion despite mixed segment trends. That guidance anchors expectations around the key catalyst of technology driven margin resilience, while highlighting that construction and small ag growth are currently offsetting pressures from softer high horsepower equipment demand, higher input costs and a still cautious North American farm customer.

But beneath that headline guidance, investors should also be aware of how prolonged weakness in large ag and higher tariffs could...

Deere's narrative projects $47.4 billion revenue and $8.4 billion earnings by 2029. This requires essentially flat yearly revenue and a $3.6 billion earnings increase from $4.8 billion today.

Uncover how Deere's forecasts yield a $665.10 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were, before this report, assuming Deere could lift earnings to about US$10.3 billion by 2029, helped by Construction & Forestry growth. Compared with consensus, that is a much more optimistic take on how quickly construction strength and fleet replacement might offset large ag and tariff risks, and this quarter’s mix shift is exactly the kind of development that could prompt you to recheck which narrative you find more convincing.

Explore 4 other fair value estimates on Deere - why the stock might be worth as much as 26% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Deere research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.