Defence Stocks Investors May Want To Screen As Europe Reworks Funding

REV Group REVG | 0.00 |

The proposed Defence, Security and Resilience Bank could reshape how capital flows into defence and aerospace, with more than €850b in annual spending across Europe and Canada and targeted support for supply chains and smaller contractors. For investors, this raises a practical question: which stocks might benefit most from easier access to financing and potentially larger order pipelines, and which might not? This article focuses on large, established defence and aerospace companies exposed to this news and reveals 3 stocks from the screener that appear well positioned to respond to these funding and policy shifts.

REV Group (REVG)

Overview: REV Group designs and builds specialty vehicles such as fire trucks, ambulances, terminal trucks, sweepers and motorized and towable RVs, selling them under a wide range of well known brands to municipalities, government agencies, private contractors, commercial customers and consumers in North America and abroad.

Operations: REV Group generates about US$1.8b of revenue from Specialty Vehicles and US$649.2m from Recreational Vehicles, with around US$2.4b coming from North America and a small contribution from other regions.

Market Cap: US$3.1b

REV Group stands out in the defence and emergency vehicle theme because its fire and ambulance franchises are tied directly to long term municipal and government fleet needs, while analysts expect strong earnings growth and high future returns on equity. The proposed Defence, Security and Resilience Bank could make it easier for key customers and suppliers in this ecosystem to secure funding, which may support order stability for specialty fleets even when conditions are tougher for discretionary RV demand. At the same time, investors need to weigh a rich current P/E, reliance on external borrowing and exposure to cost pressures and tariffs against a refreshed board, focus on higher margin segments and a large backlog that is central to the REV Group story.

REV Group’s earnings story and high expected returns on equity sound powerful, but the real question is how much is already priced in. Examine its premium P/E, borrowing needs and backlog together with the 2 key rewards and 2 important warning signs

Hammond Power Solutions (TSX:HPS.A)

Overview: Hammond Power Solutions designs and manufactures transformers and related power quality equipment that sit at the heart of electrical systems, supplying power for data centers, factories, renewable projects, EV chargers, and critical industrial and grid infrastructure across North America and India.

Operations: Hammond Power Solutions generates about CA$961.7m from the manufacture and sale of transformers, with roughly CA$690.8m from the United States and Mexico, CA$235.6m from Canada, and CA$35.3m from India.

Market Cap: CA$4.0b

Hammond Power Solutions is attracting attention because it sits where several powerful themes meet, including data center growth, grid upgrades, electrification projects, and potentially increased defence related spending that all require reliable transformers and power equipment. Inclusion in the S&P/TSX Composite Index, a sizeable backlog and exposure to EV charging and power grid infrastructure add to its appeal. At the same time, recent margin softness, a high P/E and heavy use of external borrowing keep risk firmly on the table. For investors weighing whether the current valuation fairly reflects future earnings potential, the focus is on how the backlog, new capacity in Mexico and exposure to defence and data centers interact with those risks over the next few years.

Hammond Power Solutions sits at the crossroads of data centers, grid upgrades and defence projects. Yet the real story may be how its backlog, margins and valuation fit together in the analysis report for Hammond Power Solutions

Diploma (LSE:DPLM)

Overview: Diploma is a UK based specialist distributor that supplies technical products and services across three sectors, providing controls such as cables, fasteners and automation components, seals and fluid power solutions for industrial and aerospace uses, and life sciences equipment and consumables for hospitals, labs and critical care.

Operations: Diploma generates about £940.4m from Controls, £454.2m from Seals and £252.5m from Life Sciences, with revenue spread across the USA (£869.2m), the UK (£306.8m), the rest of Europe (£270.6m) and other markets (£200.5m).

Market Cap: £9.4b

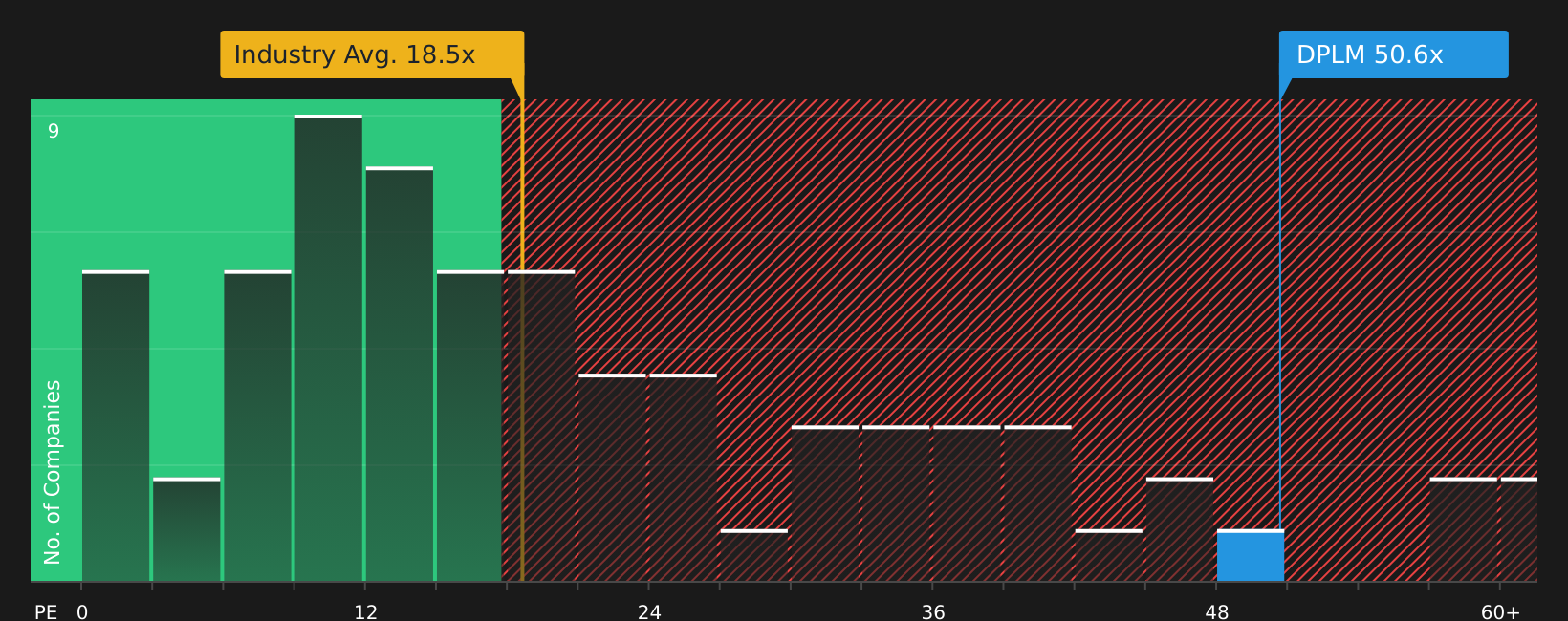

Diploma gives investors a way into defence, aerospace and healthcare supply chains through a capital light distribution model. This model has supported forecast earnings growth of about 13.8% per year and a long run record of double digit growth. The proposed Defence, Security and Resilience Bank could support demand for the high specification controls and seals Diploma supplies into aerospace and defence programs. In addition, a healthy acquisition pipeline and strong cash generation offer additional levers for compounding. On the other hand, the business trades on a rich P/E versus UK peers, has full margins that may be harder to stretch, relies on external borrowing and has a relatively new board. This leaves investors weighing quality exposure and growth against valuation, balance sheet risk and evolving governance.

Diploma’s premium P/E and capital light model suggest that the growth story might be stronger than it appears at first glance. See how the acquisition pipeline, cash generation and valuation fit together in the full narrative for Diploma

The three stocks covered here are just a starting sample, and the full Defence and Aerospace Sector Stocks screener has surfaced 30 more companies with equally compelling narratives and different mixes of defence exposure, balance sheet strength and earnings profiles in the Defence and Aerospace Sector Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts that matter to you, from defence contract exposure and cash generation to valuation and risk scores, so you can focus on the highest conviction ideas for your watchlist.

Take Control of Your Investment Journey

If Hammond Power Solutions or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Takes Off?

Fresh ideas are already building breakout momentum and could be flying higher before the crowd catches on. Check these curated lists while it still matters and act now.

- Spot resilient cash generators and stress test your watchlist against a curated list of solid balance sheet and fundamentals (48 results) that keeps financial strength front and center before volatility catches you off guard.

- Ride structural demand shifts by scanning a hand picked 33 power grid technology and infrastructure stocks built for investors watching electrification and grid upgrades accelerate, rather than reacting after the biggest moves are gone.

- Target steady income potential with a focused 7 dividend fortresses that highlights high yield opportunities so you can assess cash payouts and stability before others start chasing them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.