Defense Stocks With Long Term Contract Cover Worth Watching Now

Park Aerospace Corp. PKE | 0.00 |

Russia’s deepening fuel crisis and the spread of Ukrainian drone attacks into Moscow and key energy hubs are reshaping how risk is priced across global defense and aerospace stocks. Supply chains, military technology, and energy security are all in sharper focus, and some companies in our Global Defense and Aerospace screener sit directly in the path of this shift. For investors deciding whether to lean in or stay cautious around this theme, the details matter. This article examines 3 stocks that appear positively exposed to the current news flow, and discusses what that could mean for their risk and return profile.

Park Aerospace (PKE)

Overview: Park Aerospace develops and manufactures advanced composite materials used in aircraft structures, jet engines, missile and rocket systems, drones, and defense electronics for customers across North America, Europe, and Asia.

Operations: Park Aerospace generates about US$73.3 million in revenue primarily from Aerospace & Defense customers, with roughly US$70.2 million from North America and much smaller contributions from Europe and Asia.

Market Cap: US$702.5 million

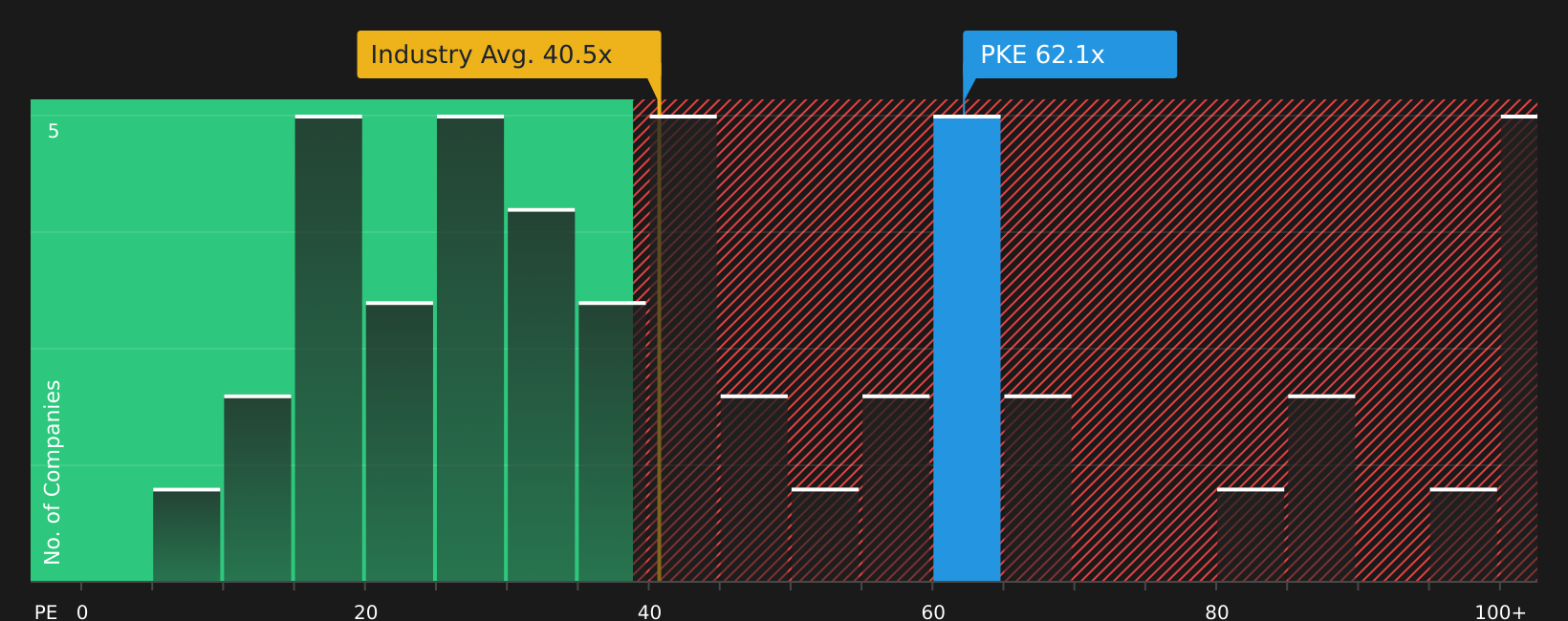

Park Aerospace operates at the intersection of rising defense spending and higher demand for precise, resilient materials in missile defense and aircraft programs. Its sole source positions in systems like the PAC 3 missile highlight its niche role in critical hardware. Recent results show higher sales and net income, and analysts see room for further revenue and earnings growth. However, the stock trades on a high P/E and relies heavily on government and aerospace program budgets, which can shift. In addition, it offers a modest dividend that is not fully covered by free cash flow and has a balance sheet funded by external borrowing. As a result, Park Aerospace is a focused defense supplier that may warrant closer scrutiny rather than a simple headline trade.

Park Aerospace’s niche missile and aircraft exposure is attracting attention, but the real question is whether current expectations fully reflect its trade off between premium P/E, program reliance, and cash coverage explained in the analysis report for Park Aerospace

Graham (GHM)

Overview: Graham Corporation supplies specialized vacuum, heat transfer, fluid, and power systems that keep refineries, chemical plants, warships, missile systems, and rockets running safely and efficiently for customers across defense, space, energy, and process industries.

Operations: Graham generates about US$245.3 million in revenue almost entirely from designing and manufacturing heat transfer and vacuum equipment, with roughly US$209.6 million from the United States and smaller contributions from Asia, Canada, the Middle East, South America, and other regions.

Market Cap: US$1.26b

Graham sits in a sweet spot for investors watching the intersection of defense, energy security, and advanced thermal management, as conflicts and data center demand keep reliability in focus. Record backlog tied to U.S. Navy and space programs, plus exposure to small modular nuclear, hydrogen, and cryogenics, provides the company with multi year visibility that many industrials lack, even as the recent Q4 showed that earnings can soften when mix shifts. The catch is a very rich P/E and heavy reliance on defense and legacy refining work, while all liabilities are funded through external borrowing, so any slip in execution or budgets could be a risk. The key consideration is whether Graham’s growth narrative and earnings profile justify paying a premium valuation for the stock at this time.

Graham’s premium P/E and record backlog suggest that investors may perceive something more significant developing beneath the surface. Get the fuller story in the analyst forecasts for Graham and what it might be overlooking.

Babcock International Group (LSE:BAB)

Overview: Babcock International Group is a UK based defense and aerospace engineering company that designs, builds, and supports warships, military vehicles, nuclear and naval systems, and mission critical training and support services for governments and defense clients around the world.

Operations: Babcock International Group generates about £5.2b in revenue, led by Nuclear at £2.1b, Marine at £1.6b, Land at £1.1b, and Aviation at £431.4m, with the United Kingdom contributing £3.6b of total sales.

Market Cap: £4.9b

Babcock International Group sits close to the center of current defense spending priorities, with long term contracts in nuclear, naval and land systems, and around 70% of revenue under contract heading into FY2027. The stock trades at a lower P/E than many aerospace and defense peers. Analysts expect faster revenue and earnings growth than the wider UK market, and buybacks have already retired about 3.4% of the share count. At the same time, earnings recently declined, returns are flattered by high debt, and all liabilities are funded through external borrowing, so the case hinges on how comfortable you are with that funding profile and the company’s ability to keep margins moving in the right direction.

Babcock International Group’s lower P/E, significant contract cover and recent earnings decline suggest investors may be missing key context on where the story goes next, so it is worth reviewing the analyst forecasts for Babcock International Group

The stocks in this article are just a starting point, and the full Global Defense and Aerospace screener surfaces 35 more defense and aerospace companies with equally compelling narratives that you have not seen yet. Use Simply Wall St to identify, filter, and analyze the specific catalysts and storylines that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Park Aerospace or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives With Real Curiosity

Fresh stock ideas can gain momentum quickly while others get caught dropping as information goes stale. Scan under the radar for now, move before the crowd, and act with care.

- Spot cash generative companies before momentum takes off by reviewing the curated 46 high quality undervalued stocks that screens for quality, pricing power, and resilient fundamentals.

- Track income opportunities that could help keep portfolios flying through volatility by scanning a curated set of high yield 8 dividend fortresses built around balance sheet strength.

- Zero in on resilient operators that may hold up when sentiment turns by reviewing a pre filtered pool of 80 resilient stocks with low risk scores designed to prioritize financial robustness.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.