Defensive Dividend Aristocrats For Sticky Inflation And Rate Uncertainty

Dollar General Corporation DG | 0.00 |

With super core inflation holding at 3.9%, the June CPI print expected to stay uncomfortable, and Middle East tensions threatening higher oil prices, many investors are looking beyond high growth stories and towards resilience. Defensive Dividend Aristocrats, with large caps, solid balance sheets, and long histories of dividend growth, can offer a different way to think about risk when S&P 500 valuations and potential Fed rate hikes point to a possible equity correction. This article examines how these inflation and rate catalysts intersect with income focused investing and highlights 3 stocks from the screener that appear positively exposed to the current backdrop.

George Weston (TSX:WN)

Overview: George Weston is a Canadian holding company that owns Loblaw grocery and drug stores and Choice Properties REIT, giving it exposure to everyday food, pharmacy, financial services and income producing real estate across the country.

Operations: George Weston generates the vast majority of its CA$65.1b revenue through Loblaw at CA$64.5b, with Choice Properties contributing CA$1.4b, and essentially all revenue coming from Canada.

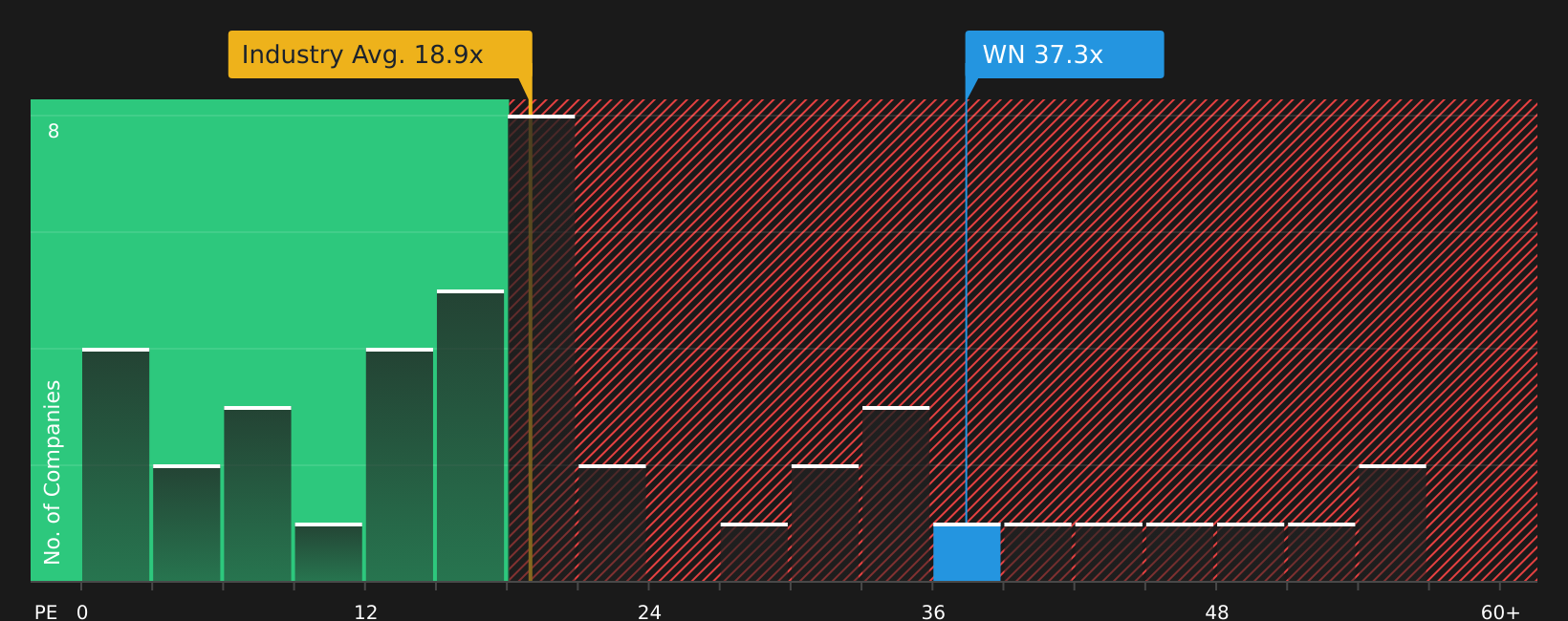

Market Cap: CA$37.3b

George Weston operates in an inflation focused, rate sensitive market and sits at the intersection of consumer staples retail and necessity based real estate, areas that many investors view as more resilient when inflation proves sticky. The company combines a long record of dividends with recent earnings momentum and active capital returns through a sizable buyback program. It also trades on a relatively high P/E and carries significant debt that could become more challenging if rates remain elevated. For investors, the interest lies in how that mix of pricing power, leverage and real estate exposure develops as inflation and policy conditions evolve.

George Weston’s mix of pricing power, leverage and real estate exposure could be masking a much bigger story for income investors. The 2 key rewards and 1 important warning sign might highlight the twist that changes how you see its resilience.

Metro (TSX:MRU)

Overview: Metro is a Canadian food and pharmacy retailer that runs supermarket, discount, neighbourhood and specialty store banners, as well as pharmacies, private label food and drug brands, and an expanding online grocery offering.

Operations: Metro generates CA$22.2b in revenue from grocery retail stores, with essentially all of its business coming from Canada.

Market Cap: CA$18.9b

Metro gives investors a way to lean into persistent inflation rather than just worry about it, as shoppers still need groceries and prescriptions when rates are rising and CPI stays uncomfortable. The company combines a long history in Canadian staples retailing with current support from private label brands, e-commerce growth and pharmacy demand, alongside ongoing buybacks and a dividend currently around 1.77%. At the same time, high debt, labour disputes such as the Laval distribution centre strike, and succession risk as a new CEO takes over in 2026 all prevent the story from being one sided. The key consideration is how those steady fundamentals and cash returns compare with these pressures for a defensive income-focused portfolio.

Metro’s steady grocery and pharmacy engine, paired with buybacks and a 1.77% dividend, could be masking a deeper income story. The 4 key rewards and 1 important warning sign might reveal the real tension investors are missing.

Dollar General (DG)

Overview: Dollar General is a U.S. discount retailer that focuses on low priced everyday essentials, from groceries and household items to basic apparel and seasonal goods, primarily serving value conscious shoppers across rural and smaller communities.

Operations: Dollar General generates about US$43.1b in revenue almost entirely from its retail store operations.

Market Cap: US$25.5b

Dollar General can be relevant when inflation stays elevated because many households, including some higher income shoppers, may trade down to its stores for consumables and basic goods. This supports its positioning as a defensive, income oriented stock with a 2.06% dividend yield. The company is investing US$1.4b to US$1.5b in remodels, new stores and technology, while growing higher margin delivery and media initiatives. These efforts are notable in the context of recent margin improvement to 3.6%. At the same time, rising labor and operating costs, heavy store expansion and competition from other value retailers keep risk firmly in view, particularly as higher interest rates affect funding conditions and consumer wallets, which is where the real debate for investors begins.

Dollar General’s remodel push, higher margin initiatives and 2.06% dividend could be masking a very different income story. The analysis report for Dollar General unpacks what that mix might really mean for long term holders.

The three stocks here are only a starting point, as the full Defensive Dividend Aristocrats screener surfaces 25 more large cap dividend payers with stories that may be just as compelling for income focused, defense minded portfolios. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter most to you so you can filter for dividend ideas that best match your own level of conviction in minutes.

Take Control of Your Investment Journey

If George Weston or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Catch On?

Fresh ideas often gain attention quickly once momentum builds. Consider using the current lull to look under the radar for potential breakouts before the crowd reacts.

- Identify early rebound stories in overlooked sectors by running the 6 high quality undervalued stocks while prices and expectations are still adjusting and attention has not fully shifted to them yet.

- Monitor where major capital spending and electrification demand may be headed next with the curated 8 top copper producer stocks before infrastructure trends significantly affect market expectations.

- Explore the next wave in automation by screening the hand picked 30 robotics and automation stocks while many of these opportunities may still be under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.