Defensive Value Stocks To Watch If AI Hype Feels Too Risky

Dollar General Corporation DG | 0.00 |

The current AI boom has pushed high profile stocks such as Caterpillar into the spotlight, with Michael Burry publicly betting against what he sees as stretched valuations. When big investors question the durability of an AI driven rally, it can be a useful moment to look at steadier ideas that rely less on market excitement. This article focuses on defensive value stocks that combine lower volatility with reasonable pricing and dividend potential. You will see 3 stocks from this screener that appear positively exposed to the latest AI sentiment shock and may appeal to investors seeking a calmer ride.

Reynolds Consumer Products (REYN)

Overview: Reynolds Consumer Products sells everyday kitchen, storage, trash, and tableware products under brands like Reynolds Wrap and Hefty, as well as store brands, supplying households and retailers in the US and internationally.

Operations: Reynolds Consumer Products generates about US$1.3b from Reynolds Cooking & Kitchen Essentials and US$851m from Hefty Home & Tableware, alongside a segment adjustment of US$1.6b.

Market Cap: US$5.7b

Reynolds Consumer Products stands out in an AI driven market because its core is simple, recurring household demand, not hype sensitive capital spending. The company is focusing on higher margin, sustainability oriented products and automation while still paying a regular dividend. It also carries meaningful debt and faces pressure from private label competitors and retailer bargaining power. Earnings and revenue growth forecasts are modest and recent profit margins have slipped, but Q1 2026 results indicate that cost control and product mix changes can influence performance. For investors considering defensive value stocks, a key question is whether Reynolds can continue using product upgrades and efficiency gains to offset input cost swings and slow category growth.

Reynolds Consumer Products looks like a quiet cash generator upgrading everyday essentials while margins and debt quietly shape the real story; see how the Reynolds Consumer Products financial health report could change your view on its resilience and risk mix

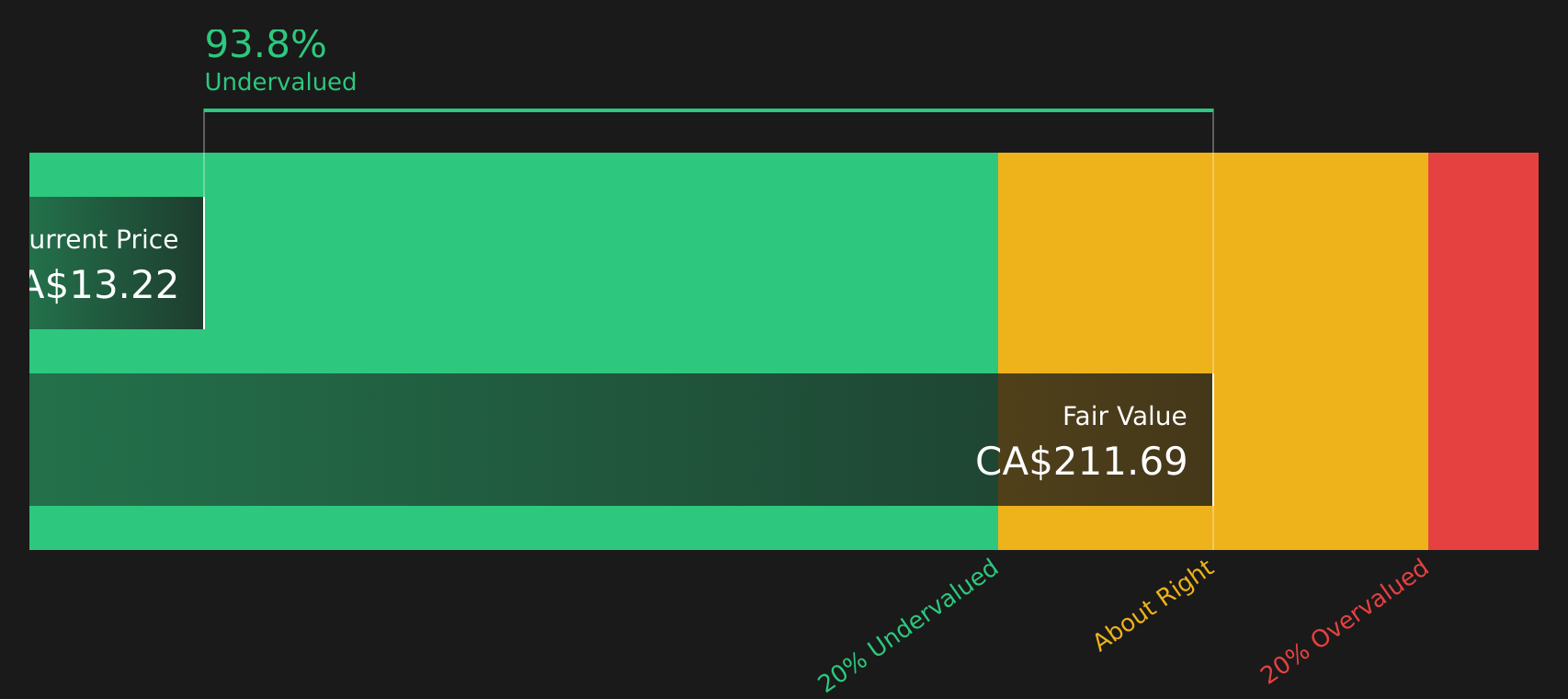

Dollar General (DG)

Overview: Dollar General is a discount retailer that runs thousands of small-box stores across the United States, stocking everyday essentials like groceries, household goods, basic apparel, and seasonal items at low price points aimed at value focused shoppers.

Operations: Dollar General generates about US$43.1b in revenue from its Retail Store Operations segment.

Market Cap: US$25.9b

Dollar General sits at the opposite end of the spectrum from high flying AI stocks, offering a large footprint in rural and small town America, resilient consumable sales, and a dividend yield of 2.05%. Earnings grew 35.6% over the past year and are forecast to rise further, while recent Q1 2026 results came in ahead of earnings expectations, which supported the stock after a period of weaker share price performance. At the same time, slower forecast revenue growth, rising labor costs, and a funding structure reliant on external borrowing all deserve attention. For investors evaluating value opportunities in a market focused on AI-related names, a key question is how far Dollar General’s remodels, private label initiatives, and digital rollout can support its role as a long term defensive holding.

Dollar General’s earnings rebound and 2.05% yield suggest a story that is still evolving, and the full picture often sits in the details. Put its remodel program, borrowing needs, and dividend side by side with the analysis report for Dollar General to see what might be hiding in plain sight.

KP Tissue (TSX:KPT)

Overview: KP Tissue (TSX:KPT) owns a stake in Kruger Products, which produces and markets bathroom tissue, facial tissue, paper towels, and napkins in Canada and the United States under brands such as Cashmere, Purex, Scotties, SpongeTowels, Bonterra and White Cloud, as well as private label products.

Market Cap: CA$136.5m

KP Tissue offers exposure to everyday tissue products that tend to hold up when excitement around AI heavy stocks fades. It has reported earnings growth of very large multiples over the past year and a P/E of 14.8x that sits below the Global Household Products industry average. At the same time, investors need to weigh its high reliance on external borrowing, relatively low 12.6% ROE, rich management pay, and recent insider selling against high quality earnings, a quarterly dividend of CA$0.21 per share, and strong revenue growth expectations. With Burry’s bets highlighting how stretched some cyclicals and chip stocks have become, KP Tissue’s mix of consumer staple resilience and a very deep discount to an internal fair value estimate makes the deeper story worth a closer look.

KP Tissue’s earnings surge and 14.8x P/E raise the question of whether its tissue cash flows are still misunderstood, and the analyst forecasts for KP Tissue hints at one forecast detail that could change how you see that story

The three stocks covered here are only a starting point, and the full screening process surfaced 21 more companies in the Defensive Value Stocks screener that share similarly compelling defensive value stories waiting to be unpacked. Use Simply Wall St to identify, filter, and analyze the specific catalysts and narratives that matter most to you so you can focus on the highest conviction ideas in this group.

Take Control of Your Investment Journey

If Dollar General or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies

Fresh stock ideas can move from quiet to crowded quickly. Once momentum catches them, ideal entry points can drop away fast. Scan these curated picks now to review them at an earlier stage.

- Spot companies quietly building staying power with a resilient balance sheet profile by running your filters through the curated list of solid balance sheet and fundamentals (48 results).

- Target income opportunities that aim to keep paying even when markets cool by checking out a curated set of high yielders in the 10 dividend fortresses.

- Explore the early stages of the AI build out by zeroing in on infrastructure suppliers screened inside the carefully filtered 51 AI infrastructure stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.