Del Monte (DMC) Flags Higher Middle East Costs, Is The Stock Trading At A Discount?

Del Monte Corporation DMC | 0.00 |

Del Monte (DMC) is in focus after CFO Monica Vicente outlined an expected $40 million to $45 million hit from higher energy, shipping and commodity costs tied to ongoing tensions in the Middle East.

The share price reaction has been weak, with Del Monte’s 30 day share price return down 13.16% and its 90 day share price return down 30.49%. The 3 year total shareholder return of 20.41% contrasts with the more recent loss of 13.35% over the past year. This suggests momentum has faded even as the company continues to highlight product stories such as its premium pineapple range.

If this kind of cost and supply chain story has you reassessing your portfolio, it could be a good moment to broaden your search with 20 top founder-led companies

So with Del Monte stock trading at $27.91 and sitting well below analyst price targets, are you looking at a potential discount here, or is the market already factoring in future growth and current cost headwinds?

Most Popular Narrative: 46.3% Undervalued

On the most followed view of Del Monte, a fair value of $52 sits well above the last close at $27.91. This raises a clear question for investors about whether current pricing reflects the full impact of recent acquisitions, rebranding and cost pressures.

Expanding premium fruit varieties, supply diversification, innovation in value-added products, and disciplined financial management are driving market leadership, stable margins, and growth opportunities.

The expansion of value-added, fresh-cut product lines and premium fruit formats is fueling higher net sales and improved segment margins, but current financial performance may overstate long-term earnings potential if investor expectations assume indefinite double-digit growth rates tied to these convenience and health-conscious consumption trends.

Want to see what sits behind that confidence in Del Monte's future earnings power? The narrative leans on ambitious revenue growth, margin repair and a lower future earnings multiple that still supports a higher fair value.

Result: Fair Value of $52 (UNDERVALUED)

However, Del Monte's story could look very different if structural cost inflation bites harder than expected or if climate related disruptions weigh more heavily on supply and margins.

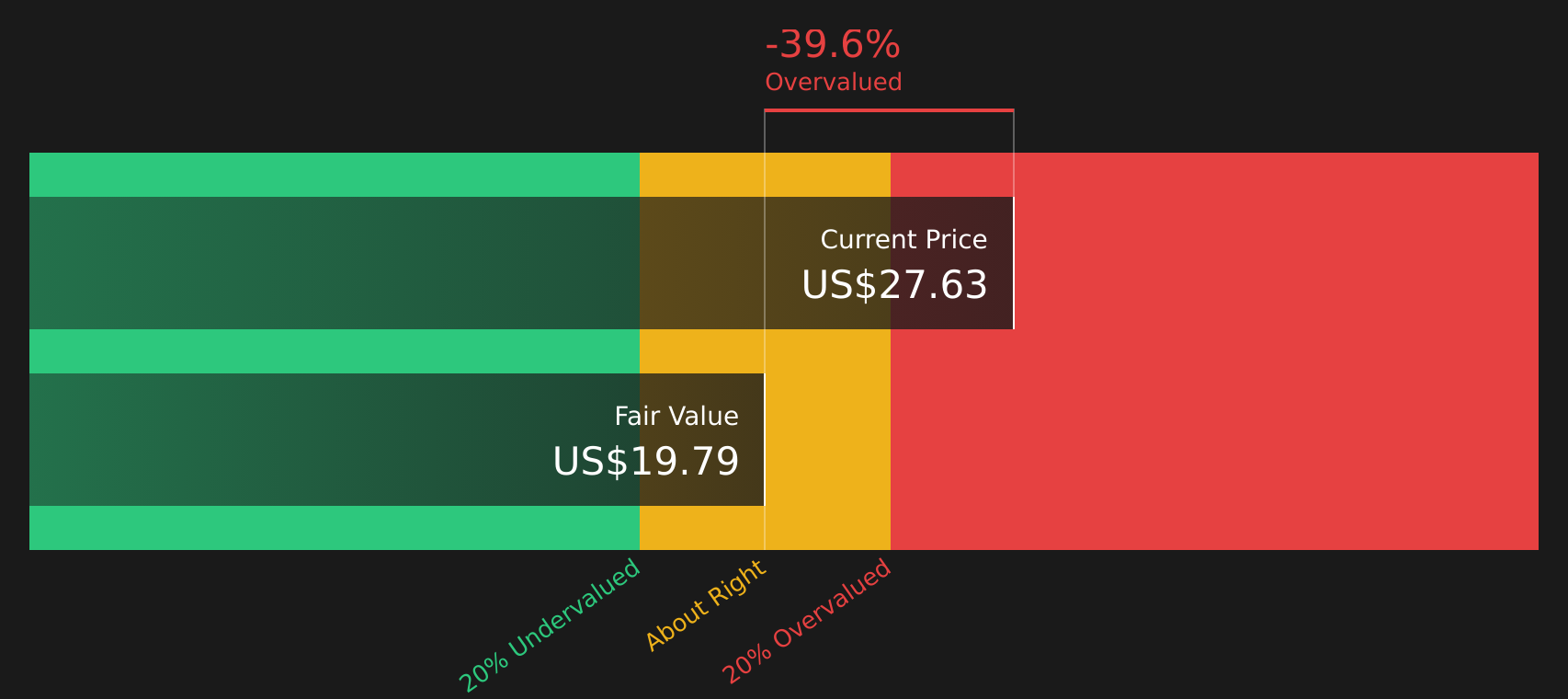

Another View: SWS DCF Fair Value Check

While many investors focus on Del Monte's $52 analyst target, the SWS DCF model paints a more cautious picture. In this view, the stock price of $27.91 sits above an estimated future cash flow value of $19.41, which points to possible overvaluation based on cash generation alone.

That kind of gap between cash flow value and market price raises a simple question: are you more comfortable anchoring on earnings-based targets, or on what the SWS DCF model says the cash flows are worth today? Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Del Monte for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Del Monte have you on the fence, now is a good time to review the data and decide where you stand, including weighing its 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond Del Monte?

If Del Monte's mixed signals have sharpened your focus, use that momentum to refresh your watchlist with stocks that match your risk, income and quality preferences.

- Target higher yield opportunities by reviewing companies in the 10 dividend fortresses that may suit an income focused approach.

- Spot potential value opportunities early by scanning the screener containing 19 high quality undiscovered gems before they appear on everyone else's radar.

- Prioritize capital protection by filtering for companies in the 74 resilient stocks with low risk scores that align with a more cautious style.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.