Delta Air Lines (DAL) Is Up 7.6% After Securing New Credit Line And Beating Revenue Estimates – Has The Bull Case Changed?

Delta Air Lines, Inc. DAL | 0.00 |

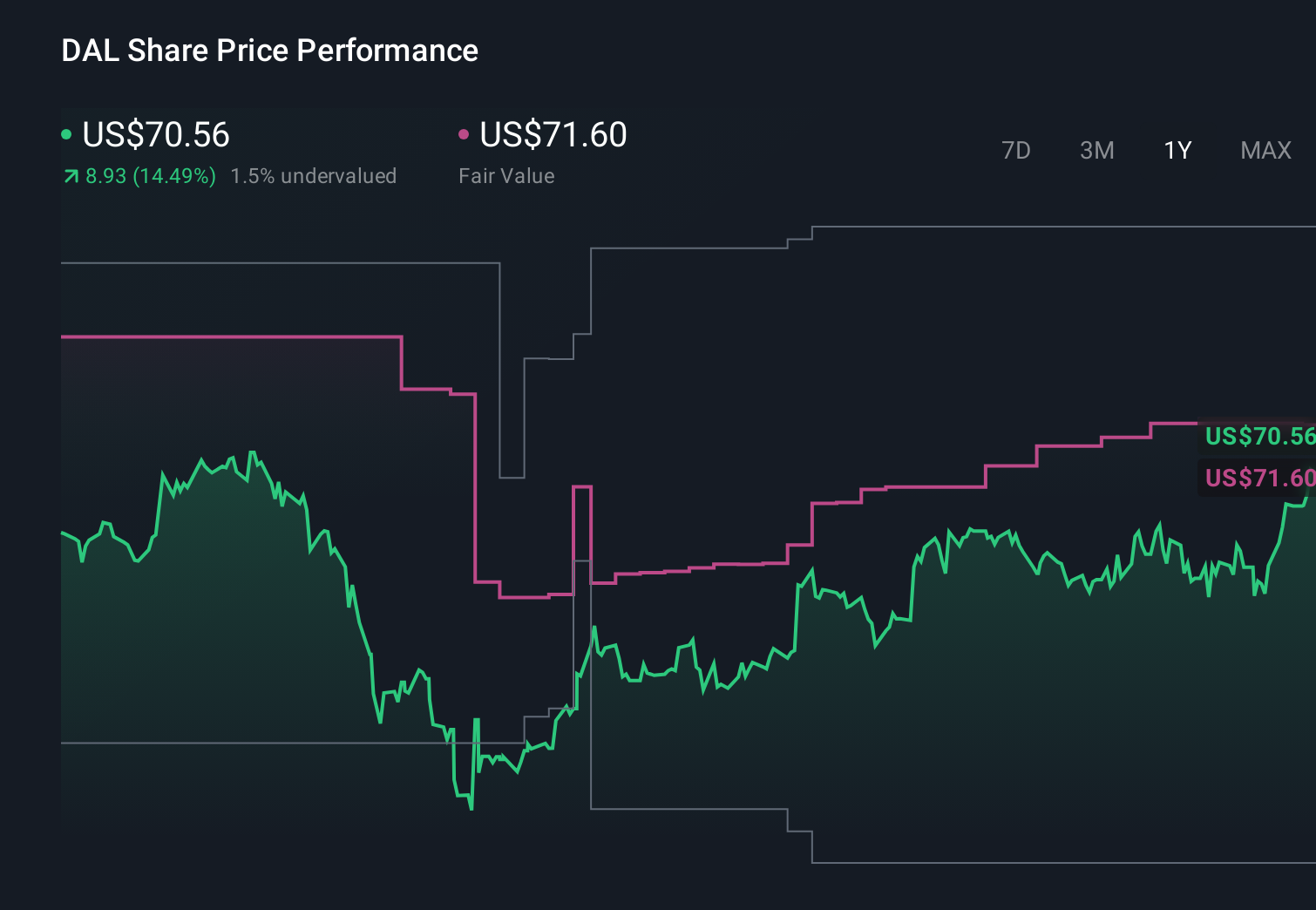

- Delta Air Lines recently entered into a new US$2.65 billion revolving credit facility with JPMorgan Chase and other lenders to refinance its prior agreement and support general corporate purposes, while also reporting quarterly revenue that exceeded analyst expectations despite an earnings miss and higher fuel and operating costs.

- The combination of stronger-than-expected revenue, expanded financing flexibility with undrawn credit and ongoing product and loyalty enhancements underscores how Delta is trying to balance growth initiatives with tighter financial discipline.

- Next, we’ll examine how Delta’s better-than-expected revenue alongside its larger, undrawn credit facility could influence its investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Delta Air Lines Investment Narrative Recap

To own Delta, you need to believe its mix of premium, loyalty and international revenue can offset a softer domestic backdrop and higher costs. The key near term catalyst is how quickly earnings can catch up with stronger-than-expected revenue, while the main risk is that fuel and operating costs stay elevated and pressure margins. The new, undrawn US$2.65 billion credit facility modestly reduces financial risk by adding liquidity support, but it does not remove those core earnings pressures.

Among the recent updates, the expanded Delta SkyMiles American Express benefits are especially relevant. They reinforce one of Delta’s key catalysts: growing high margin loyalty and co‑brand credit card revenue. More generous checked bag and rideshare perks, alongside richer welcome offers, tie directly into the premium and loyalty themes that many investors focus on when weighing near term earnings volatility against longer term cash flow potential.

Yet even with better liquidity and loyalty growth, investors should be aware of how rising non fuel costs and potential aircraft tariffs could...

Delta Air Lines' narrative projects $73.2 billion revenue and $5.3 billion earnings by 2029. This requires 3.9% yearly revenue growth and a $0.8 billion earnings increase from $4.5 billion today.

Uncover how Delta Air Lines' forecasts yield a $81.81 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming revenue stays around US$66.7 billion and earnings near US$5.2 billion by 2029, so if you worry about rising non fuel costs and softer main cabin demand, this more cautious view shows how far expectations can differ and how this new credit facility and recent earnings surprise might eventually shift those assumptions.

Explore 9 other fair value estimates on Delta Air Lines - why the stock might be worth as much as 27% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Delta Air Lines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.