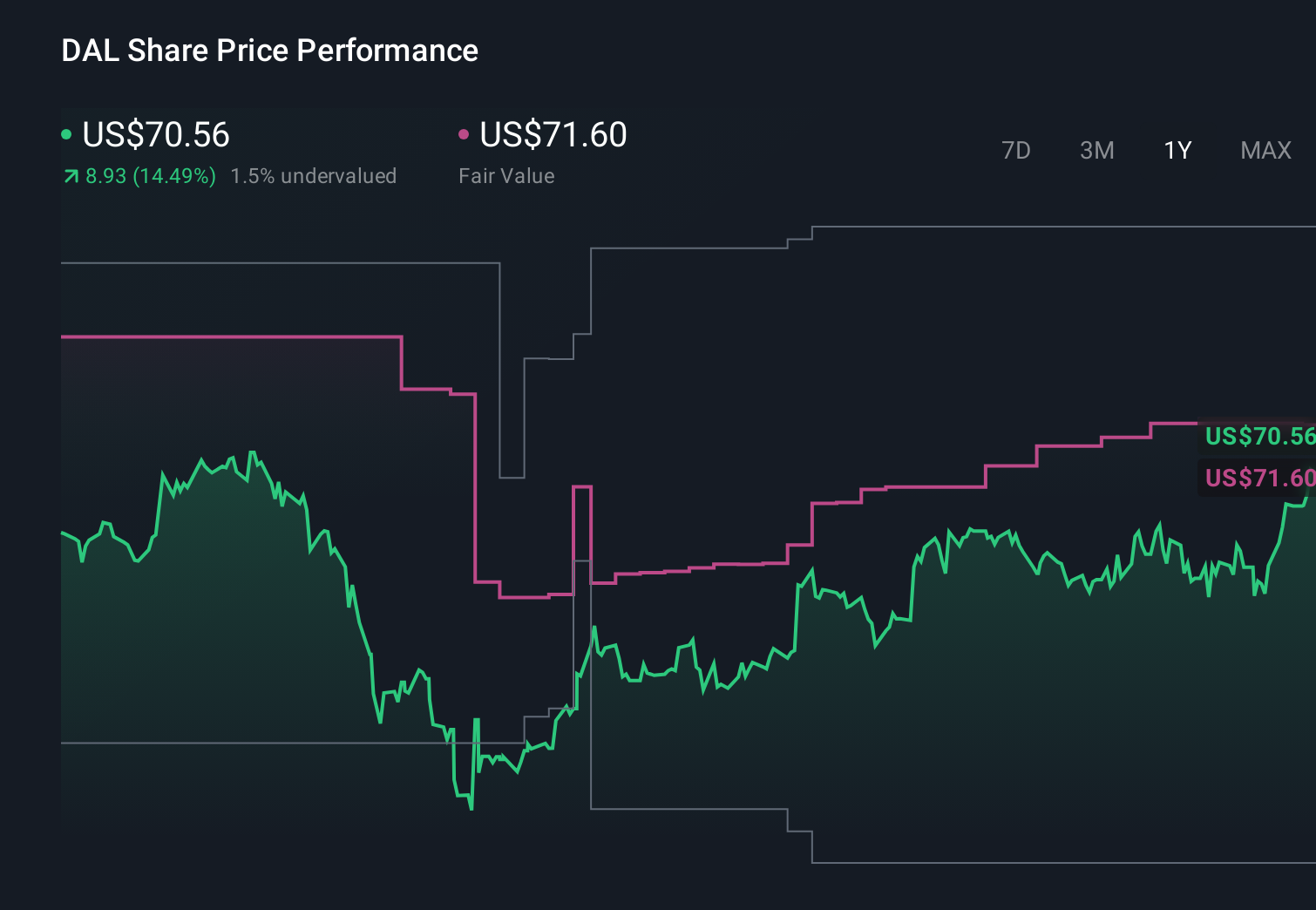

Delta Air Lines (DAL) Is Up 7.7% After Dividend Hike And Russell Growth Index Additions

Delta Air Lines, Inc. DAL | 0.00 |

- Delta Air Lines recently increased its quarterly dividend by roughly 15% to US$0.215 per share, payable on July 30, 2026, and was added to multiple Russell growth benchmarks, including the Russell 1000 Growth and Russell Midcap Growth indexes.

- Together, the higher cash payout and new index inclusions highlight Delta’s growing appeal to income-focused and benchmark-tracking institutional investors alike.

- Next, we’ll examine how Delta’s dividend increase reshapes its existing investment narrative around premium demand, capacity discipline, and earnings stability.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Delta Air Lines Investment Narrative Recap

To own Delta, you need to believe its focus on premium, loyalty, and international travel can offset softer domestic demand and cost pressures. The near term catalyst remains execution on margin protection and free cash flow, with the dividend increase and Russell growth index additions mainly reinforcing confidence rather than changing that story. The biggest risk still centers on a slowdown in corporate and main cabin demand that could pressure revenue and squeeze margins if weakness persists.

The roughly 15% dividend hike to US$0.215 per share is the clearest link to this story, because it ties directly to Delta’s ability to keep generating and returning cash even as it holds capacity growth flat and prunes weaker routes. For investors watching earnings stability, that higher payout underscores management’s comfort with current cash flows, but it also raises the stakes if economic uncertainty or domestic softness lasts longer than expected.

Yet behind the higher dividend and index inclusion, investors should be aware of the very real possibility that domestic main cabin softness and corporate travel weakness could...

Delta Air Lines' narrative projects $73.2 billion revenue and $5.3 billion earnings by 2029. This requires 3.9% yearly revenue growth and about an $0.8 billion earnings increase from $4.5 billion today.

Uncover how Delta Air Lines' forecasts yield a $81.81 fair value, a 12% downside to its current price.

Exploring Other Perspectives

Some of the lowest analysts take a tougher view than consensus, assuming revenue stays around US$66.7 billion by 2029 and earnings only reach about US$5.2 billion. They are more focused on flat domestic demand and rising non fuel costs, and may see the dividend hike and Russell growth index additions as tests of whether Delta can really deliver on its premium and loyalty story over time.

Explore 9 other fair value estimates on Delta Air Lines - why the stock might be worth as much as 14% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Delta Air Lines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.