Devon Acquisition Gives Coterra Holders A Bigger Shale Platform Bet

Coterra Energy CTRA | 34.56 | +1.89% |

- Devon Energy has entered a definitive agreement to acquire Coterra Energy (NYSE:CTRA), forming a large combined shale operator in the United States.

- The transaction will combine two oil and gas producers into a single company focused on shale assets, headquartered in Houston.

- The deal outlines the combined structure, leadership, and a plan to align benefits for shareholders of both companies.

Coterra Energy, ticker NYSE:CTRA, is an oil and gas producer with a focus on shale assets, which sit at the center of the United States energy supply. The tie up with Devon Energy comes as consolidation continues across the sector, with scale and portfolio breadth becoming key themes for larger operators. For investors, the headline point is that Coterra is expected to move from a standalone producer to part of a much larger shale focused group.

Investors may pay close attention to how the combined company approaches integration, capital allocation, and any updated shareholder return framework that follows the announcement. It will also be important to monitor how the new Houston based operator manages its shale assets, cost structure, and balance sheet once the transaction closes and additional information is provided.

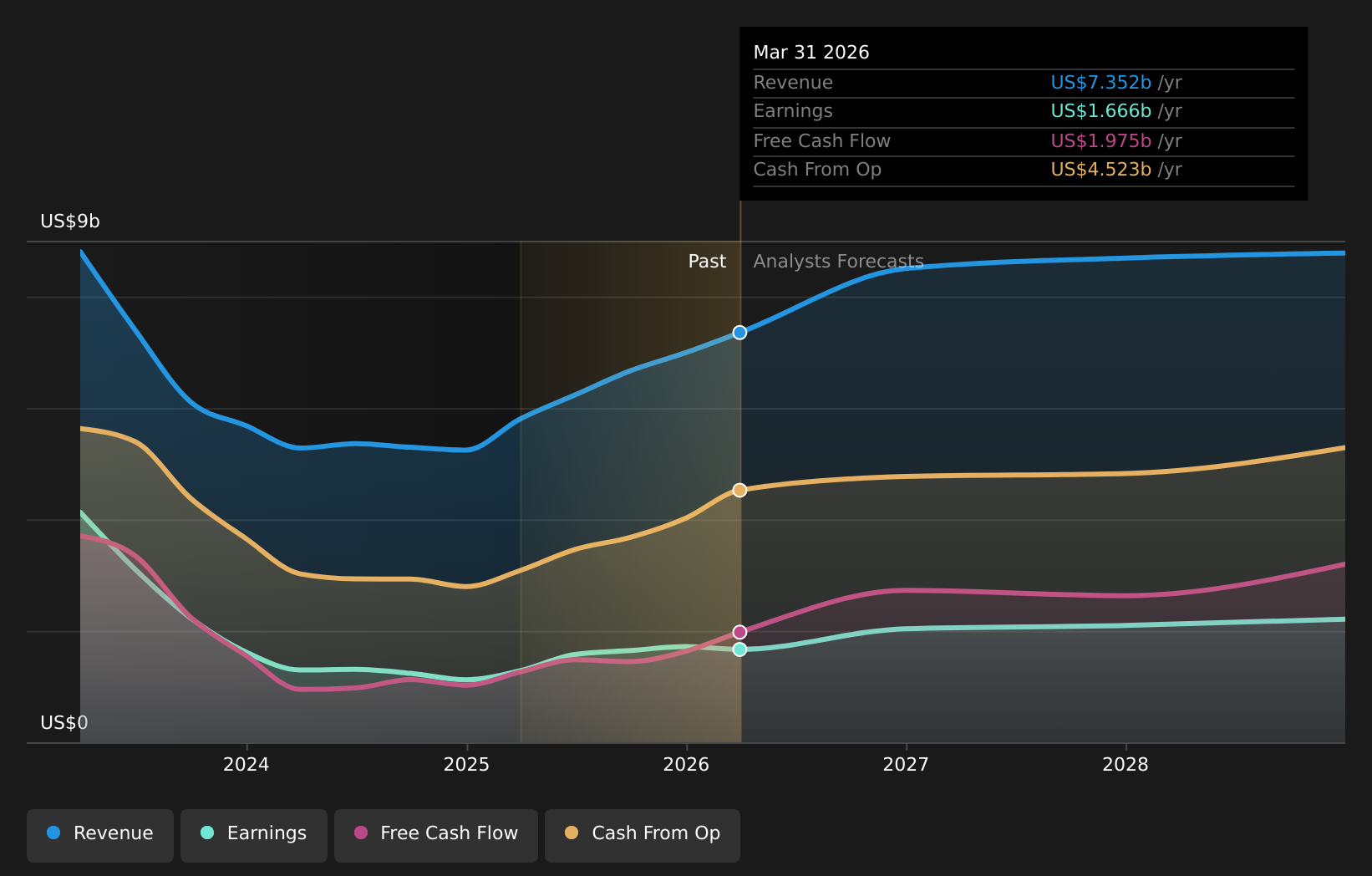

Stay updated on the most important news stories for Coterra Energy by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Coterra Energy.

For Coterra shareholders, this all stock deal at a fixed 0.70 Devon share per Coterra share effectively swaps exposure to a gas and oil balanced producer into a larger shale focused platform that will sit alongside peers like EOG Resources and Pioneer Natural Resources in scale. The combined enterprise value of about US$58b and shared board and management structure suggest Coterra’s current business model, including its Marcellus gas and Permian oil positions, will be folded into a broader multi basin plan where capital allocation decisions are set at Devon group level rather than standalone Coterra.

Coterra Energy narrative gets a new chapter

The existing Coterra narratives highlight production growth across Permian, Marcellus and Anadarko and LNG linked gas marketing as key building blocks for stable cash flow, and this transaction effectively tests how those themes play out inside a larger corporate structure. Investors who have been focused on Coterra’s inventory depth, capital efficiency and activism around governance now need to assess whether the combined Devon platform continues to prioritize those same levers or tilts more toward Devon’s pre deal priorities.

Risks and rewards for Coterra holders

- The merger creates a larger shale operator with shared executive leadership, which could support operating efficiencies and give Coterra assets more flexibility in capital allocation across basins.

- Coterra holders are set to own about 46% of the combined company, so they keep meaningful participation in any future value created by integration and portfolio optimization.

- Execution risk sits around integrating different asset bases and corporate cultures, and analysts have already flagged questions about deal structure, governance and how shareholder return policies might change.

- The transaction is subject to regulatory, antitrust and shareholder approvals, so timing or terms could shift, and a termination would involve an US$865m fee paid by either party.

What to watch next

From here, you may want to track updates on regulatory reviews, any revised production or capital plans for key areas like the Delaware Basin and Marcellus, and how the future dividend and buyback approach for the combined Devon entity is framed to both shareholder groups. If you want to see how other investors are thinking about Coterra’s role inside this deal, take a look at the community narratives on its company page for additional viewpoints.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.