Devon Coterra Merger Reshapes Shale Scale Governance And Investor Returns

Coterra Energy CTRA | 34.56 | +1.89% |

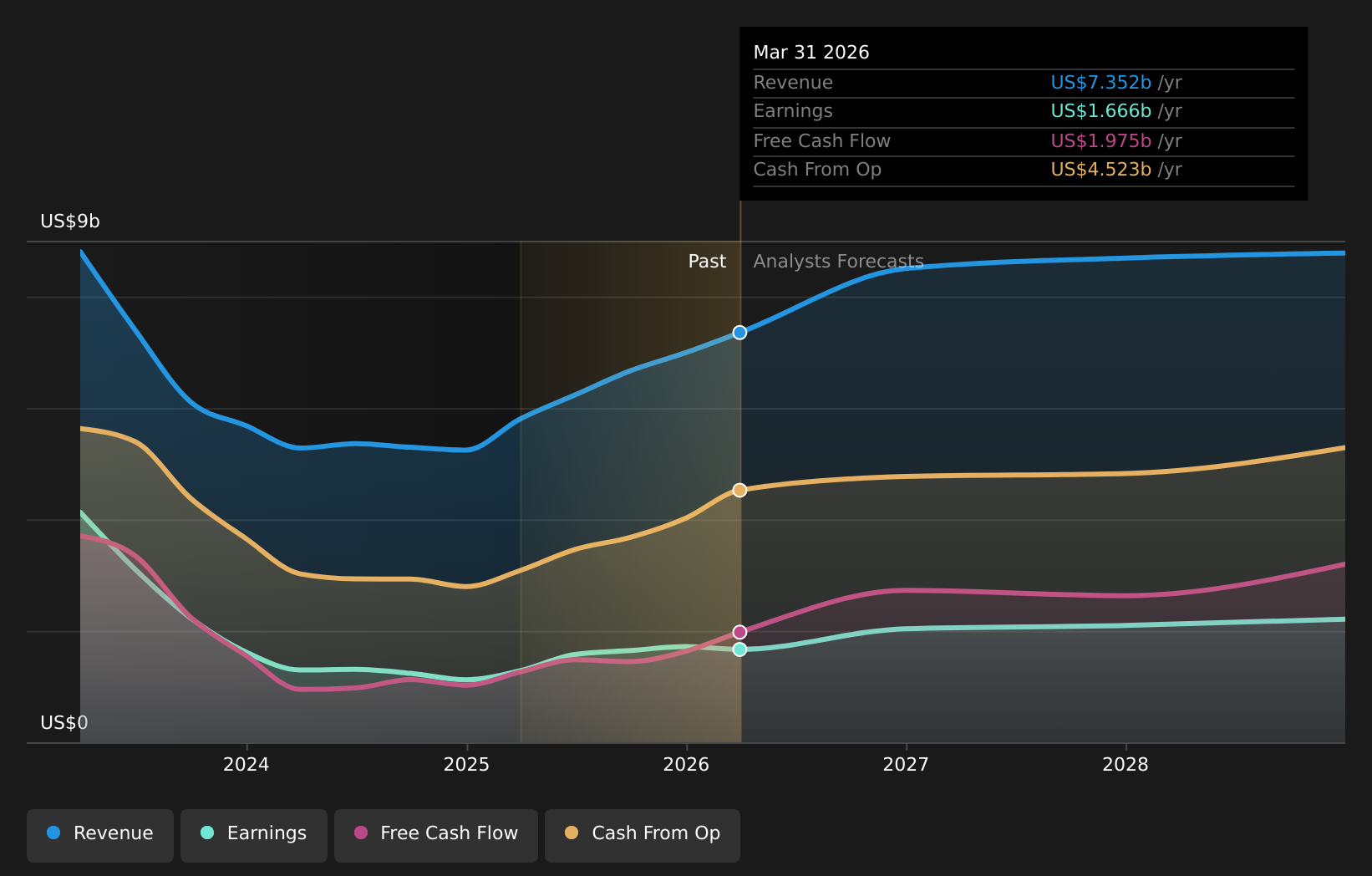

- Devon Energy and Coterra Energy (NYSE:CTRA) have entered into a definitive merger agreement, forming a combined shale operator with an estimated enterprise value of about US$58b.

- The deal includes changes to the management team and board structure for the combined company.

- The transaction terms feature higher dividends for shareholders and a sizeable share repurchase program.

- An investigation is underway into whether Coterra's Board met its fiduciary duties in agreeing to the merger.

Coterra Energy, listed on the NYSE under the ticker CTRA, focuses on U.S. shale assets, a segment that has been central to domestic oil and gas production. This merger with Devon comes at a time when scale, capital discipline, and balance sheet strength are key themes for listed energy producers. For current and potential investors, the deal reshapes how Coterra fits into the wider group of publicly traded shale operators.

Looking ahead, the combined entity is expected to operate with an expanded asset base, a revised leadership structure, and a defined capital return framework that includes dividends and share buybacks. Investors may want to follow further disclosures on integration plans, board decisions, and the outcome of the fiduciary duty investigation to understand how the merger could affect ownership, cash returns, and risk profile.

Stay updated on the most important news stories for Coterra Energy by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Coterra Energy.

For Coterra holders, this is effectively an all stock exit into a larger, more diversified operator. The fixed 0.70 Devon share for each Coterra share locks in a specific relative value, so your upside or downside now ties directly to how Devon trades through closing. Coterra investors move from owning a pure Coterra story to holding about 46% of a combined US$58b enterprise with a board and management team led by Devon, and the company name switching to Devon Energy. That shift in control, plus the Houston headquarters, means Coterra’s governance and capital allocation priorities will be filtered through Devon’s framework.

How This Fits Into The Coterra Energy Narrative

- The deal aligns with prior commentary that a combination with Devon could be a way to scale operations across the Permian and Marcellus, potentially reinforcing earlier expectations around efficiency and capital discipline.

- At the same time, Coterra’s standalone plans around activism, buybacks, and production growth now depend on how the combined company prioritizes those levers, which could differ from the original narrative.

- The ongoing investigation into whether the board fulfilled its fiduciary duties, and the US$865m termination fee, add process and governance considerations that were not part of the earlier storyline.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Coterra Energy to help decide what it's worth to you.

The Risks and Rewards Investors Should Consider

- ⚠️ Deal execution and integration risk for two large shale players, especially as governance shifts to a Devon led board and management team.

- ⚠️ The fixed exchange ratio means Coterra holders are exposed to Devon share price volatility up to closing, with limited recourse outside the merger terms and US$865m termination fee provisions.

- 🎁 Management targets for higher dividends and a planned US$5b plus buyback program could offer a clearer cash return framework than Coterra on its own.

- 🎁 Combining complementary acreage positions in the Permian and Marcellus may support operating efficiencies versus peers such as EOG Resources and Pioneer Natural Resources.

What To Watch Going Forward

From here, keep an eye on the regulatory timetable, especially antitrust review, as well as any updated financial targets the companies publish as they refine synergy estimates. Shareholder votes at both Coterra and Devon will be a key hurdle to watch, including any pushback from activists or governance focused investors. It is also worth tracking how the combined company outlines its capital return priorities, including the balance between dividends, buybacks, and reinvestment, relative to what pure play peers such as Occidental and ConocoPhillips are doing.

To ensure you're always in the loop on how the latest news impacts the investment narrative for Coterra Energy, head to the community page for Coterra Energy to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.