DICK'S Sporting Goods (DKS) Stock Looks Expensive After A 172% Run

Dick's Sporting Goods, Inc. DKS | 0.00 |

DICK'S Sporting Goods stock has delivered strong long term gains over the past five years, yet the current valuation checks lean expensive rather than cheap. With the share price at US$229.76 and the recent news flow focused on growth, margins and capital allocation, investors are weighing solid historical returns against a weaker value score and an overvalued read on market multiples.

- Over the past five years, DICK'S Sporting Goods has returned 172.2%, which puts extra focus on whether the current price already reflects much of that success.

- Recent sales momentum and ongoing investments in stores and omnichannel capabilities can support expectations for future growth, while pressure on profit margins and a cautious outlook on consumer demand may limit how much investors are willing to pay for that growth.

- DICK'S Sporting Goods scores 0 out of 6 on the broader valuation checks, which suggests the stock does not screen as a clear bargain at current levels on Simply Wall St's valuation framework.

The issue now is whether DICK'S Sporting Goods' current price still offers an attractive entry point after such a strong multi year run, or whether expectations built into the valuation leave limited room for disappointment.

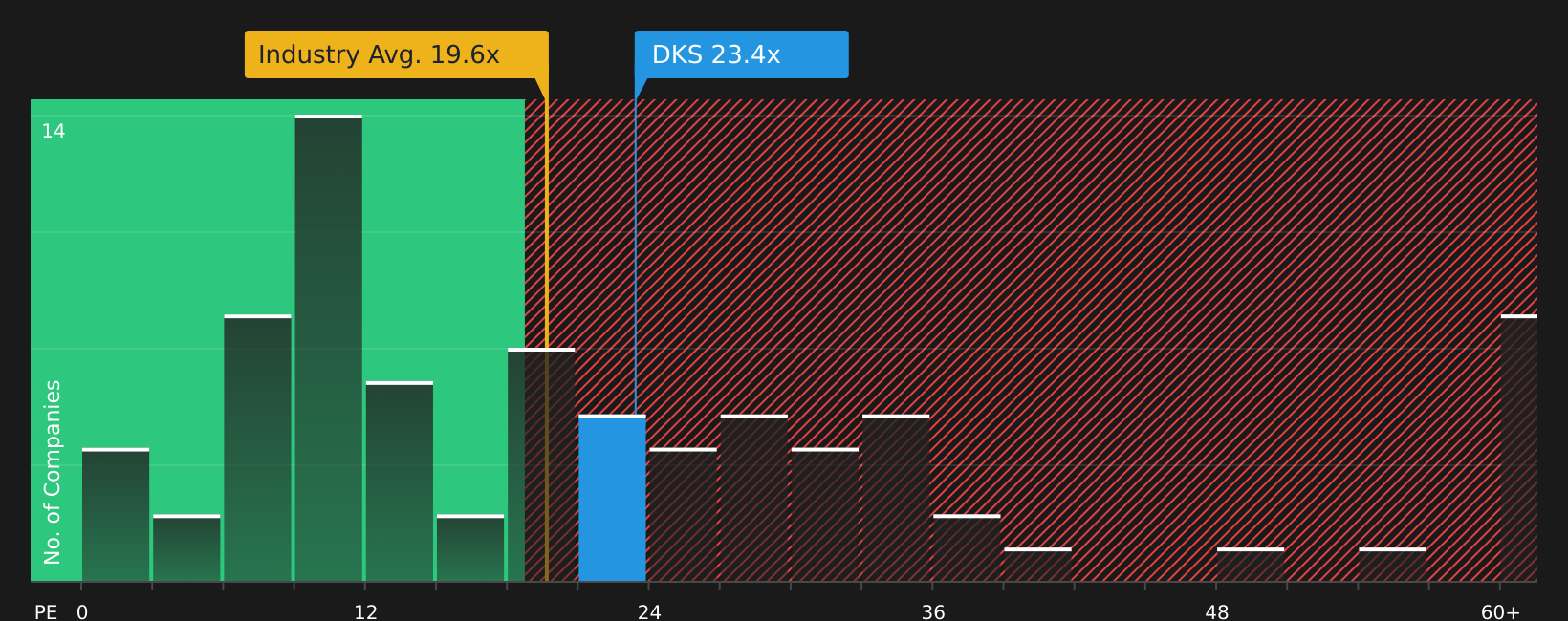

Does DICK'S Sporting Goods Look Pricey on Earnings?

The P/E ratio is a useful yardstick for DICK'S Sporting Goods because earnings remain a key focus for retailers with established store footprints and online channels. On this measure, the stock trades at about 22.7x earnings, a small premium to both the Specialty Retail industry average of roughly 19.7x and the peer group average of about 22.0x.

The tailored fair P/E ratio for DICK'S Sporting Goods is estimated at 19.9x, which sits below the current market multiple and indicates that the shares are pricing in a richer earnings valuation than this framework suggests. Despite the recent strong Q1 sales update and commentary around omnichannel initiatives, the lowered full year earnings guidance and margin pressures indicate that this higher multiple is based on expectations that may already be reflected in the price.

On the P/E yardstick, DICK'S Sporting Goods stock currently appears overvalued relative to its implied fair multiple.

The DICK'S Sporting Goods Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for DICK'S Sporting Goods pick up where the P/E discussion leaves off. They set out the specific growth, margin and earnings paths that would need to play out for DICK'S Sporting Goods' stock to be worth materially more or less than today’s price, and they sit on the company’s Community page. Instead of giving a single valuation number in isolation, they unpack the future that number is built on so you can later check whether reality is tracking that script.

Community views on DICK'S Sporting Goods sit far apart, with one camp leaning into the long term engine and another focused on integration and margin strain.

Bull case: 8% undervalued

"Expansion of high-margin vertical/private label brands (DSG, CALIA, VRST) and greater proprietary assortment are driving margin expansion and brand loyalty..."

Bear case: 25% overvalued

"Commitment to significant capital expenditures of approximately $1 billion in 2025, in parallel with maintaining a strong dividend payout and share repurchase program, could strain cash flows..."

Do you think there's more to the story for DICK'S Sporting Goods? Head over to our Community to see what others are saying!

The Bottom Line

For DICK'S Sporting Goods, the current market multiples lean overvalued, so the stock no longer screens as an obvious bargain on earnings alone. The broader valuation checks are weak, which means you are paying up today for a story that hinges on how well growth investments translate into sustained margins and earnings quality. The real swing factor from here is whether DICK'S Sporting Goods can defend profitability while continuing to invest in stores and omnichannel offerings without stretching its valuation further.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.