Did Analyst Optimism on PHVS Pipeline Outweigh Continued Losses in Pharvaris’ Latest Results?

Pharvaris N.V. PHVS | 29.45 29.45 | +4.25% 0.00% Post |

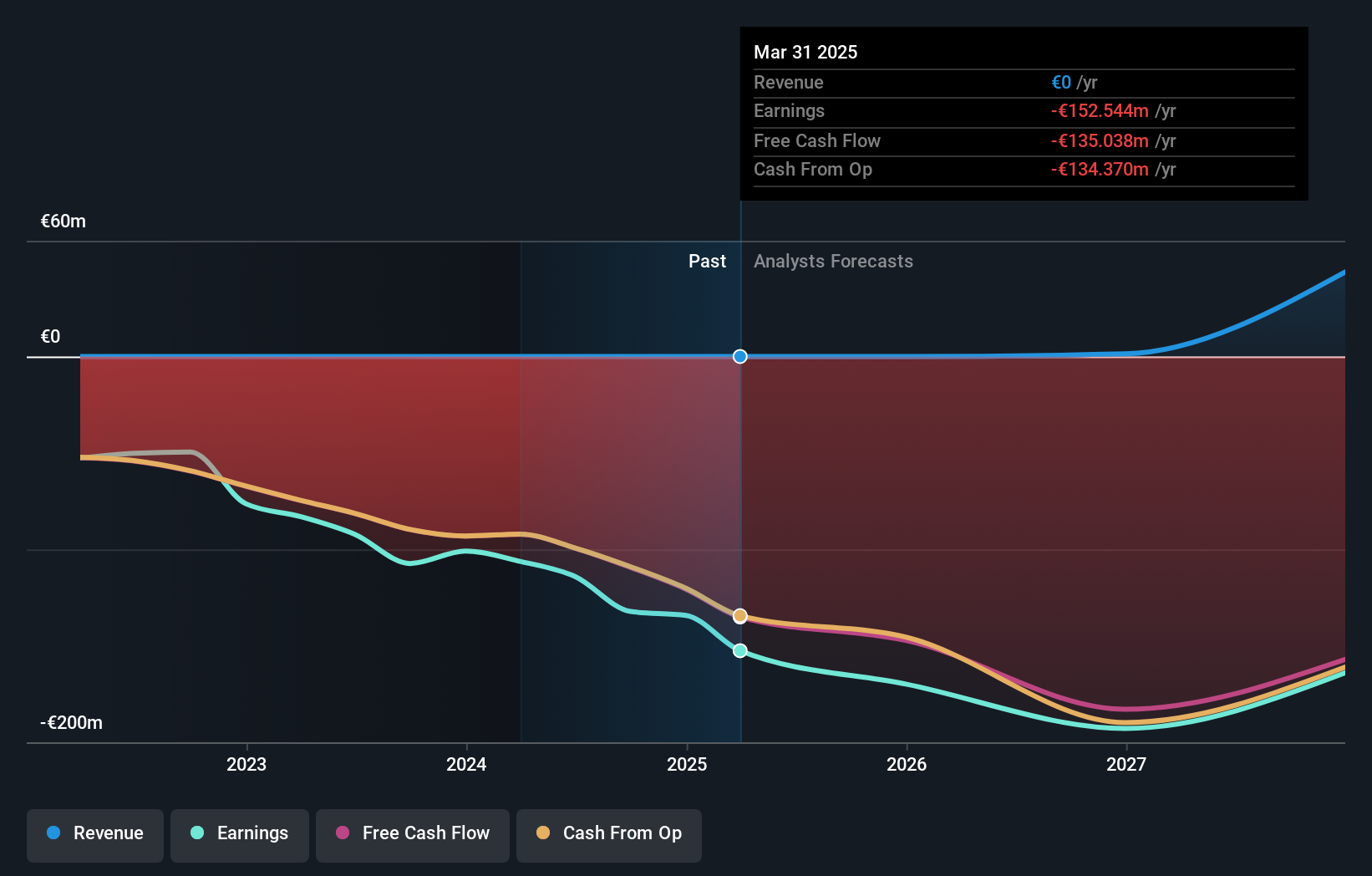

- Pharvaris reported a net loss of €37.14 million for the third quarter of 2025, narrowing from €41.71 million a year earlier, while losses for the first nine months increased to €128.96 million from €99.46 million in the prior year.

- Despite ongoing negative earnings, the company has drawn significant analyst optimism due to its differentiated oral bradykinin B2 antagonist pipeline targeting hereditary angioedema and anticipation of pivotal Phase 3 data.

- We'll examine how the high expectations surrounding Pharvaris' late-stage hereditary angioedema pipeline shape the company's investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

What Is Pharvaris' Investment Narrative?

For me, being a Pharvaris shareholder comes down to believing in the company’s ability to bring a differentiated, oral therapy for hereditary angioedema (HAE) to the finish line and secure regulatory approval. The recent earnings report narrowed the quarterly net loss, but the year-to-date loss continued to climb, reminding investors that Pharvaris is still without commercial revenue and highly reliant on its pipeline. While the latest financials didn’t deliver a big surprise, they offer a slight improvement in capital efficiency and don’t seem to shift the biggest short-term catalyst: pivotal Phase 3 data due by year-end 2025. Analyst optimism continues to center on this clinical milestone, with consensus price targets suggesting significant upside. Key risks remain unchanged, however, with clinical results, potential financing needs, and regulatory hurdles top of mind.

Yet, it's the risk of further shareholder dilution that could catch many off guard.

Exploring Other Perspectives

Explore another fair value estimate on Pharvaris - why the stock might be worth as much as 48% more than the current price!

Build Your Own Pharvaris Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Pharvaris research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Pharvaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pharvaris' overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.