Did Assurant's (AIZ) Broadened Holman Partnership Just Shift Its Growth Strategy Narrative?

Assurant, Inc. AIZ | 217.03 | -0.36% |

- Assurant, Inc. recently announced an expanded partnership with Holman, supporting thirty newly added dealership locations following Holman's acquisition of Leith Automotive Group, and providing a suite of finance and insurance products, dealership sales and training, and participation program guidance.

- This move, alongside significant leadership appointments, represents a coordinated effort to accelerate growth and operational efficiency across Assurant's expanding business lines.

- We'll explore how the broadened Holman partnership highlights Assurant's push for growth through new client channels and operational scale.

Find companies with promising cash flow potential yet trading below their fair value.

Assurant Investment Narrative Recap

For investors considering Assurant, the key narrative hinges on the company’s ability to grow recurring fee-based revenue from connected devices, homes, and auto protection, while managing competitive and regulatory pressures, especially within Global Housing. The expanded Holman partnership may serve as a near-term boost for new client channels, yet it does not materially shift the most important catalyst: sustaining premium growth in emerging service segments. The principal risk remains concentrated regulatory scrutiny in lender-placed insurance, which could impact margins if future changes are adverse.

Among the recent news, Assurant’s leadership appointments stand out as most relevant to its partnership expansion. Bringing operations and IT together under Mike Campbell as COO highlights an internal push for accelerated innovation and more seamless delivery of products and services, supporting the broader objective of operational efficiency, a catalyst strongly aligned with recurring earnings growth and the company’s ability to scale new channels, like those with Holman.

But while these growth drivers are promising, investors should also keep a close eye on the evolving risks around lender-placed insurance…

Assurant's narrative projects $14.2 billion revenue and $1.2 billion earnings by 2028. This requires 4.9% yearly revenue growth and a $483 million earnings increase from $717.0 million.

Uncover how Assurant's forecasts yield a $241.00 fair value, a 12% upside to its current price.

Exploring Other Perspectives

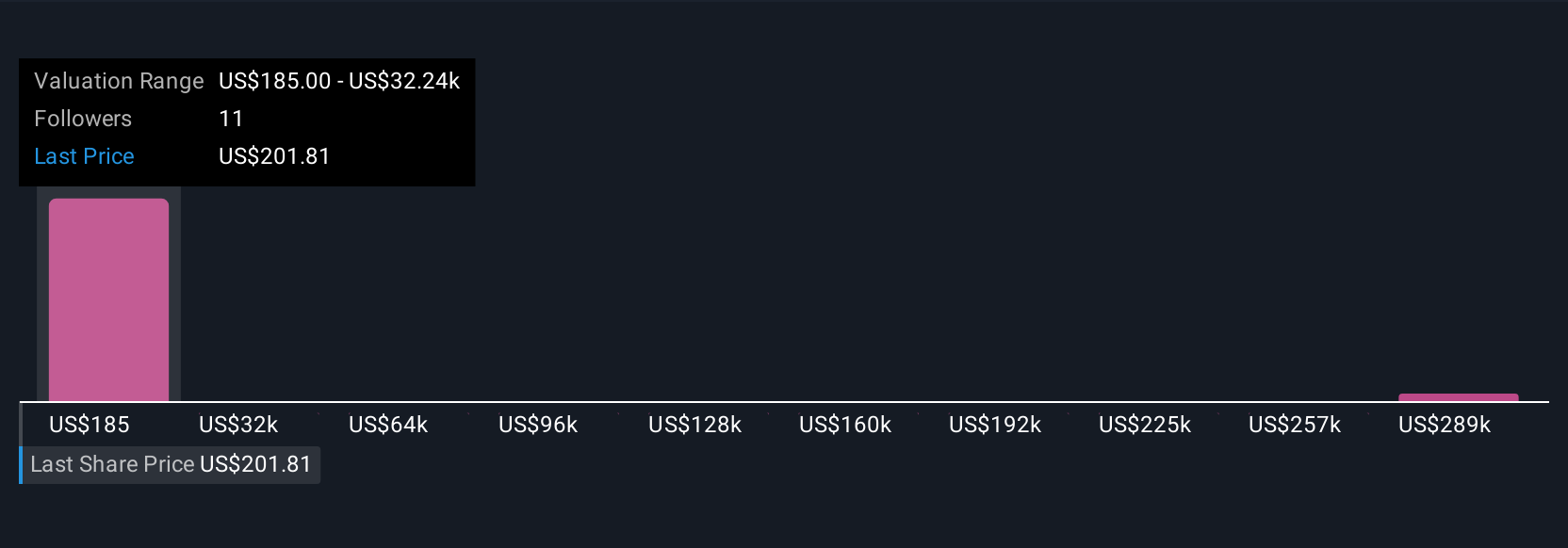

Four members of the Simply Wall St Community offered fair value estimates for Assurant, ranging from US$185 to US$320,700.23. With regulatory scrutiny persisting as a top concern, you can see how market participants’ views may differ when weighing current growth efforts against future risks.

Explore 4 other fair value estimates on Assurant - why the stock might be a potential multi-bagger!

Build Your Own Assurant Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Assurant research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Assurant research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Assurant's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.