Did Crude Above $100 and a Big 13G Stake Just Shift NOV's (NOV) Investment Narrative?

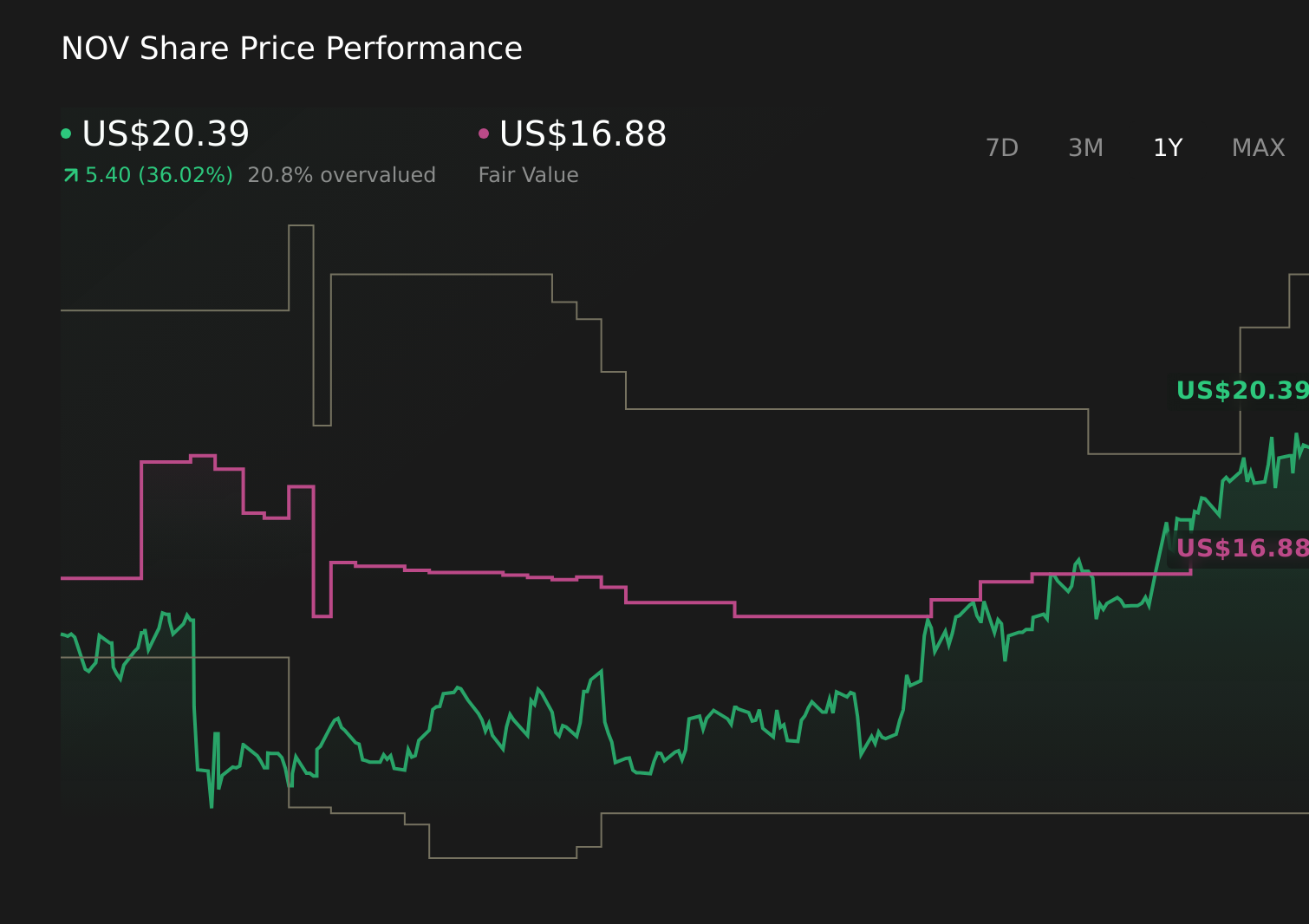

NOV Inc. NOV | 0.00 |

- In the past week, Hotchkis and Wiley Capital Management disclosed an amended passive 13G filing showing beneficial ownership of 14,919,613 NOV shares, while NOV’s oilfield services business has drawn fresh attention as crude prices moved above US$100 per barrel on geopolitical and supply concerns.

- Together, the large passive stake and renewed interest in oilfield services highlight how macro energy market conditions can quickly recalibrate investor focus on NOV’s role in supporting global oil and gas activity.

- With crude above US$100 underscoring renewed interest in oilfield services, we’ll now examine how this development reshapes NOV’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 44 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

NOV Investment Narrative Recap

To own NOV today, you need to believe that its equipment and services will remain central to global oil and gas development, even as the cycle stays choppy. The Hotchkis & Wiley 13G and the share move on US$100-plus crude highlight stronger sentiment, but they do not materially change the near term picture where softer recent results and pricing pressure remain the key catalyst and risk to watch.

The recent decision to roughly double subsea flexible pipe capacity in Açu, Brazil, backed by backlog extending into 2028, stands out here. It ties directly to NOV’s reliance on large offshore and infrastructure projects as a growth driver, but also reinforces exposure to lumpy order timing and potential project delays that can weigh on revenue and margins if conditions worsen.

Yet against the excitement around higher oil prices, investors should also be aware of the growing risk that a faster global shift toward renewables could...

NOV's narrative projects $9.3 billion revenue and $528.1 million earnings by 2029.

Uncover how NOV's forecasts yield a $20.65 fair value, in line with its current price.

Exploring Other Perspectives

While consensus focuses on incremental offshore recovery, the most optimistic analysts were assuming revenues near US$9.4 billion and earnings around US$588 million by 2029, which is a far more bullish path than today’s muted outlook and shows how differently you and other investors might interpret fresh macro shocks like US$100 crude.

Explore 5 other fair value estimates on NOV - why the stock might be worth 19% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NOV research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free NOV research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NOV's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.