Did Domino’s (DPZ) Cost Controls and Tech Investments Just Shift Its Long-Term Investment Case?

Domino's Pizza, Inc. DPZ | 358.79 356.06 | +1.66% -0.76% Pre |

- Last week, Domino’s Pizza reported a slight earnings beat amid heavy promotions, supported by strong cost controls, efficient pricing, and robust technology integration across global operations.

- Industry-leading returns on assets, rising institutional interest, and disciplined capital returns have reinforced Domino's market positioning even as some franchise operators in the sector face economic pressures.

- We'll explore how Domino's disciplined approach to technology and cost optimization could influence its long-term earnings outlook and investment case.

Find companies with promising cash flow potential yet trading below their fair value.

Domino's Pizza Investment Narrative Recap

To own Domino’s Pizza stock, you need to believe in the company's ability to drive consistent global expansion and margin efficiency through technology, while navigating an industry that’s experiencing flat traffic and rising competition. Recent news regarding franchisee bankruptcies highlights pressure on operators, but the direct impact on Domino’s core business and its main short-term catalyst, the expansion of digital delivery platforms, remains limited, since Domino’s cost discipline and technology strategy are intact. The biggest risk for shareholders is continued stagnation in consumer demand for pizza, which could constrain future revenue growth even as new channels are rolled out.

Of the latest developments, Domino’s reconfirmed its plan to grow its global store footprint towards a long-term target of 50,000 locations, emphasizing steady but measured expansion. This announcement is highly relevant, since ongoing unit growth and successful digital initiatives are central to driving incremental revenue, especially as other industry players face operational headwinds.

In contrast, investors should also be mindful of how stubbornly flat overall pizza demand could challenge Domino’s ability to meet its growth ambitions…

Domino's Pizza's outlook anticipates $5.6 billion in revenue and $720.0 million in earnings by 2028. This implies a 5.5% annual revenue growth rate and a $122.9 million earnings increase from current earnings of $597.1 million.

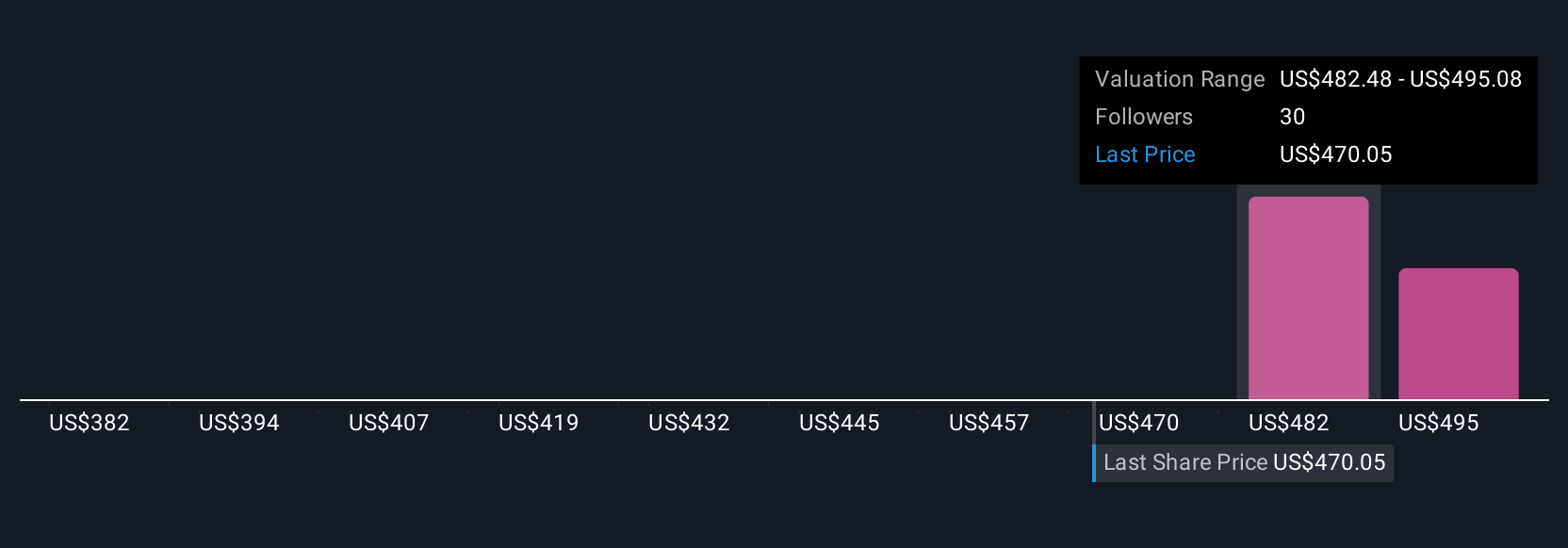

Uncover how Domino's Pizza's forecasts yield a $500.03 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community estimate fair value for Domino’s between US$341.98 and US$500.03. With pizza category growth stagnating, different views highlight why keeping an eye on demand trends is essential.

Explore 3 other fair value estimates on Domino's Pizza - why the stock might be worth 17% less than the current price!

Build Your Own Domino's Pizza Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Domino's Pizza research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Domino's Pizza research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Domino's Pizza's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 35 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.