Did DoorDash’s (DASH) Custom EV Partnership With ALSO Just Rewire Its Last‑Mile Economics?

DoorDash DASH | 0.00 |

- In late March 2026, Palo Alto–based EV maker ALSO announced a multi‑year commercial agreement and investment partnership with DoorDash to deploy purpose‑built small electric vehicles for dense urban delivery, alongside DoorDash co‑founder Stanley Tang joining ALSO as a Board Observer.

- This move highlights DoorDash’s push to reshape last‑mile logistics through custom electric fleets that could influence costs, reliability, and service quality in crowded cities.

- Next, we’ll examine how DoorDash’s push into purpose‑built electric delivery vehicles may influence its investment narrative and long‑term positioning.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe it can turn its large delivery footprint and software tools into sustainably profitable, higher margin commerce infrastructure. In the near term, the key catalyst is whether advertising, automation, and international expansion can keep lifting earnings, while the biggest risk remains cost pressure from labor and complex multi‑market operations. The ALSO partnership could be helpful over time but does not materially change those near term drivers or risks yet.

The MOST directly relevant recent development is DoorDash’s broader automation push, including partnerships with Waymo, Serve Robotics, Coco Robotics, and its DoorDash Dot robots. The ALSO agreement fits into this theme of testing different autonomous and small EV formats that might, over time, lower fulfillment costs per order. For now, these efforts are still early, so their impact sits more in the “potential long term efficiency lever” bucket than a clear short term catalyst.

Yet behind DoorDash’s automation push, investors should also be aware that rising regulatory and labor pressures on the gig model could...

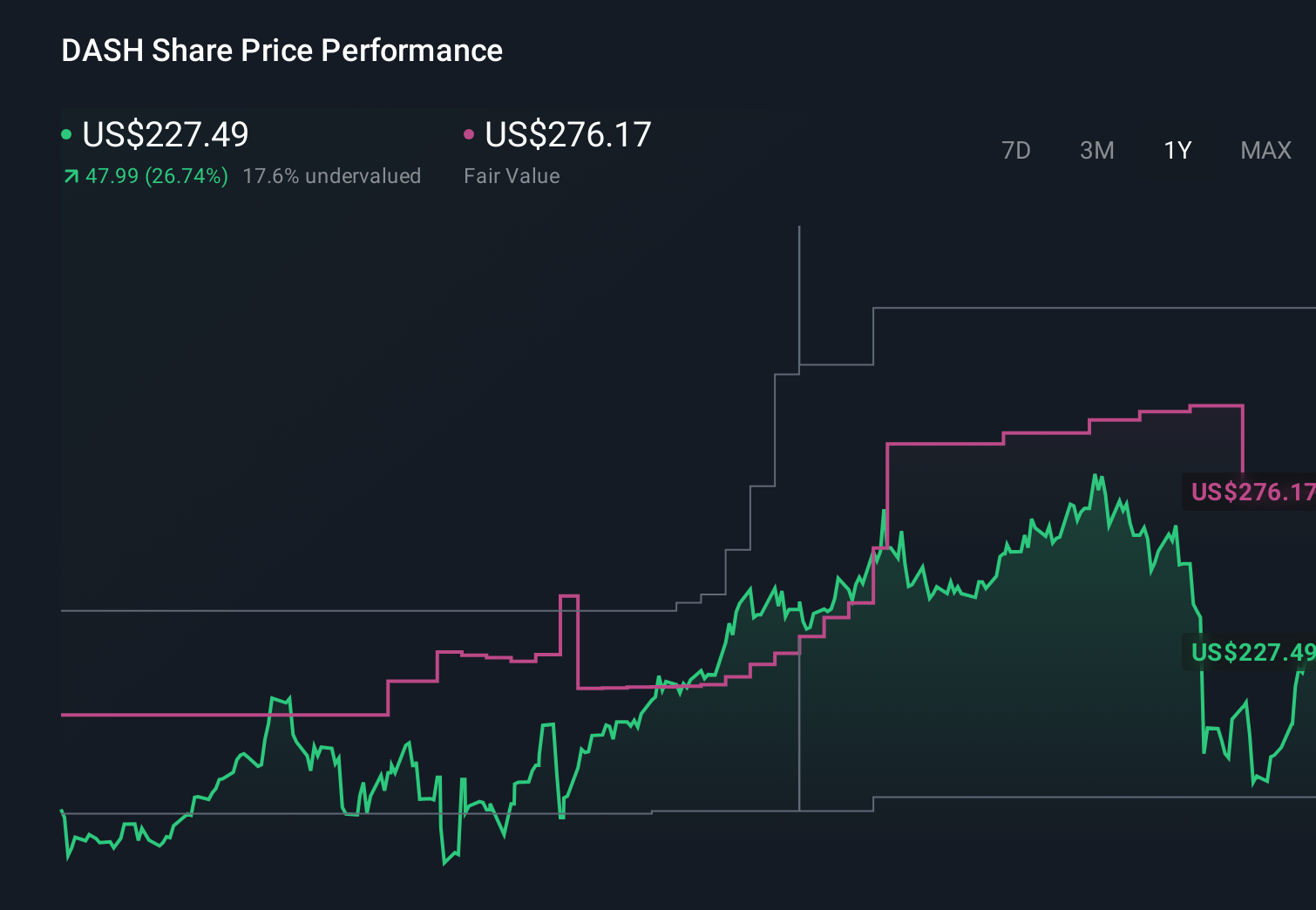

DoorDash’s narrative projects $20.4 billion revenue and $3.2 billion earnings by 2028. This requires 19.6% yearly revenue growth and about a $2.4 billion earnings increase from $781.0 million today.

Uncover how DoorDash's forecasts yield a $258.00 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$21.9 billion and earnings near US$4.8 billion by 2028, assuming automation sharply lifts margins; compared with the baseline view, that is a much more ambitious path that could either be reinforced or challenged as deals like ALSO evolve and you weigh them against concerns about tougher gig labor rules.

Explore 13 other fair value estimates on DoorDash - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

No Opportunity In DoorDash?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 61 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.