Did DoorDash’s New Retail Partnerships Shift the Valuation in 2025?

DoorDash, Inc. Class A DASH | 150.50 150.50 | +0.23% 0.00% Post |

- Wondering if DoorDash stock is a hidden bargain or already priced for perfection? Let’s break down the numbers and see what’s beneath the headlines.

- Shares have returned 7.0% over the past year and are up a staggering 241.9% over three years. There have been notable setbacks lately, including an 8.4% dip in the last week and a 24.8% slide this month.

- DoorDash has remained in the news thanks to its expanding partnerships with major retailers and ongoing investments in convenience offerings. These moves are adding momentum, even as the broader tech sector faces skepticism. Investors continue to debate the company’s long-term growth trajectory and how much is reflected in today’s price.

- On our valuation checks, DoorDash scores a 3 out of 6, suggesting there’s still plenty to unpack. In the sections ahead, we’ll walk through common valuation approaches and, by the end, reveal a smarter way anyone can judge if the stock really offers value right now.

Approach 1: DoorDash Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting future cash flows and discounting them back to their present value. This method aims to measure what the company is truly worth today, based on its ability to generate cash in the future.

For DoorDash, the latest Free Cash Flow (FCF) stands at $2.04 Billion. Analyst estimates and modeling forecast significant growth, with FCF expected to climb to $6.25 Billion by 2029. These projections rely on a combination of near-term analyst consensus and longer-term extrapolations, providing a balanced look at DoorDash’s profit potential.

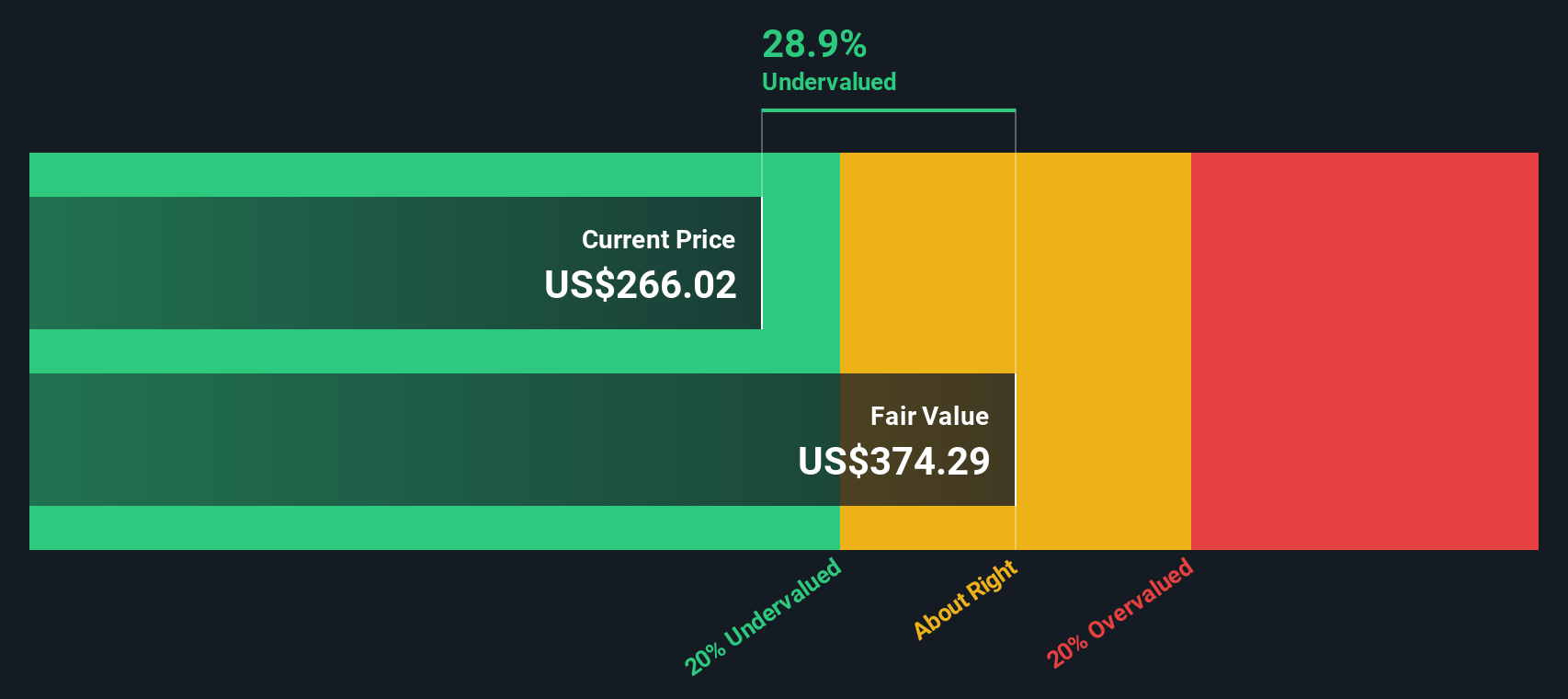

Applying the 2 Stage Free Cash Flow to Equity approach, the DCF analysis arrives at an intrinsic value of roughly $310.74 per share. This value is about 39.0% higher than the company’s current share price. According to this measure, the stock appears significantly undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DoorDash is undervalued by 39.0%. Track this in your watchlist or portfolio, or discover 918 more undervalued stocks based on cash flows.

Approach 2: DoorDash Price vs Earnings (PE) Ratio

For profitable companies, the Price-to-Earnings (PE) ratio is one of the most popular ways investors gauge valuation. It measures the price investors are willing to pay today for each dollar of current earnings, making it useful for companies like DoorDash that are now generating positive profits.

However, what constitutes a “normal” or “fair” PE ratio can vary depending on expectations for future growth and the level of risk investors perceive. Companies with higher growth prospects or lower risk tend to command higher PE ratios, while slower-growing or riskier companies are valued more conservatively.

Currently, DoorDash trades at a PE ratio of 94.7x, well above the Hospitality industry average of 20.8x and its peer group average of 33.4x. While this premium reflects optimism about DoorDash's growth, it also means a lot of future performance is already “priced in.”

This is where Simply Wall St's Fair Ratio comes in. The Fair Ratio, in this case 46.5x, is a proprietary estimate that considers DoorDash’s expected earnings growth, profit margins, market cap, risk profile, and its industry context. This metric offers a more tailored view of what is reasonable for the company, rather than relying solely on broad industry averages or peer comparisons, which may ignore unique company factors.

Compared to its Fair Ratio, DoorDash’s current PE is almost double what would be considered fair, suggesting that the stock may be trading at a substantial premium and is likely overvalued by this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1422 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your DoorDash Narrative

Earlier, we mentioned there is an even better way to understand valuation, and that brings us to Narratives. A Narrative is your personal investment story: a belief or perspective about DoorDash’s future that links company news and trends to your own financial forecasts and fair value estimate.

Narratives bridge the gap between what you believe will happen (such as growth in revenue, margins, or market share) and how that could influence DoorDash’s share price. This helps you move beyond generic metrics. On Simply Wall St's Community page, millions of investors use Narratives as an interactive tool to build, update, and compare real-time investment theses.

With Narratives, you can visualize whether DoorDash is a buy or sell for you, based on how your fair value compares with today’s market price. The interface adjusts dynamically as new information comes in, such as fresh earnings reports or breaking news.

For example, one investor might craft a bullish Narrative, projecting rapid expansion and setting a fair value above $360. Meanwhile, a more cautious investor, wary of competitive risks and cost pressures, could set their fair value closer to $205. Narratives put the decision-making power, and the reasoning behind it, firmly in your hands.

Do you think there's more to the story for DoorDash? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.