Did Eversource Energy's (ES) Strong Earnings Rebound Just Shift Its Long-Term Investment Narrative?

Eversource Energy ES | 0.00 |

- Eversource Energy recently reported third quarter and nine-month 2025 earnings, showing higher sales at US$3.22 billion and strong profitability, turning around from a net loss a year earlier.

- The company also reaffirmed its full-year and long-term earnings guidance, indicating confidence in the underlying strength of its core utility business and future earnings outlook.

- With quarterly net income rebounding sharply, we'll explore how this performance supports the company's investment narrative and future growth assumptions.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

Eversource Energy Investment Narrative Recap

To be a shareholder in Eversource Energy, you have to believe that demand for reliable regulated utilities in New England will keep growing, and that the company can execute large-scale capital projects while gaining timely regulatory approvals. The recent rebound in quarterly earnings lends support to this outlook, but the biggest immediate catalyst, clarity on Connecticut regulatory decisions, remains unchanged and the company still faces material risks if regulatory recovery or asset sales are delayed.

Among recent announcements, Eversource’s reaffirmed 2025 and long-term earnings guidance stands out as directly relevant given this quarter’s results. Management's confidence in maintaining its 5% to 7% EPS growth target highlights positive rate case developments and improved fundamentals following a period marked by a rare net loss and a significant one-off charge.

But investors shouldn't overlook the ongoing regulatory uncertainty in Connecticut, which could quickly shift the outlook if...

Eversource Energy's outlook anticipates $14.8 billion in revenue and $2.1 billion in earnings by 2028. This is based on a 4.4% annual revenue growth rate and an earnings increase of $1.24 billion from the current $858.0 million.

Uncover how Eversource Energy's forecasts yield a $75.60 fair value, a 3% upside to its current price.

Exploring Other Perspectives

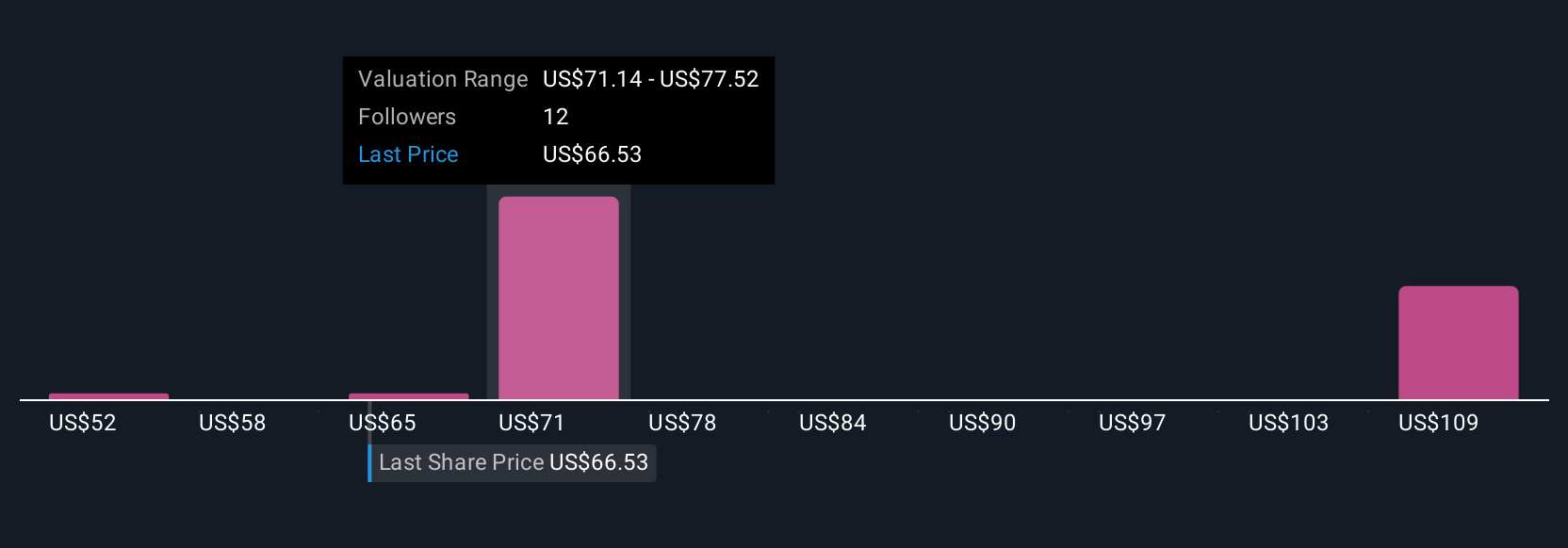

Simply Wall St Community members produced four fair value estimates for Eversource Energy, ranging from as low as US$52 to as high as US$229.47 per share. While earnings guidance boosts confidence in future growth, regulatory delays still cast a shadow on near-term predictability and could affect the company's ability to sustain EPS gains.

Explore 4 other fair value estimates on Eversource Energy - why the stock might be worth 29% less than the current price!

Build Your Own Eversource Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Eversource Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Eversource Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Eversource Energy's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.