Did Fresh Bullish Coverage on Post-Merger Execution Just Shift Permian Resources' (PR) Investment Narrative?

Permian Resources PR | 20.66 21.12 | +1.37% +2.25% Pre |

- In recent days, several Wall Street firms, including KeyBanc and Truist Securities, have initiated or reaffirmed positive coverage on Permian Resources, emphasizing its execution since the 2022 Centennial-Colgate merger and its focus on oil and natural gas development in the Permian Basin.

- This wave of analyst attention highlights growing institutional interest in the company’s operational progress and acquisition-driven model, potentially influencing how investors view its long-term growth profile and capital allocation.

- We’ll now explore how this increased analyst confidence, centered on post-merger operational execution, may reshape Permian Resources’ existing investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Permian Resources Investment Narrative Recap

To own Permian Resources, you need to believe in the resilience of its Permian Basin drilling program and its ability to convert production into durable free cash flow despite commodity price swings and ongoing capital needs. The recent cluster of upbeat ratings from firms such as KeyBanc and Truist largely reinforces, rather than changes, the near term picture, where oil price volatility remains the key catalyst and M&A and drilling intensity are the core risks.

The most directly relevant development is KeyBanc’s initiation with an Overweight rating and US$25.00 target, citing strong execution since the Centennial Colgate merger. Coming alongside Truist’s new coverage and Raymond James’ higher price target, this broad analyst support interacts with existing catalysts like efficiency gains and balance sheet strength by putting more attention on whether Permian can keep integrating assets and sustaining production within its current cost and regulatory constraints.

Yet behind this upbeat analyst wave, there is still the underappreciated risk that tighter environmental rules and higher compliance costs could materially affect margins that investors should be aware of...

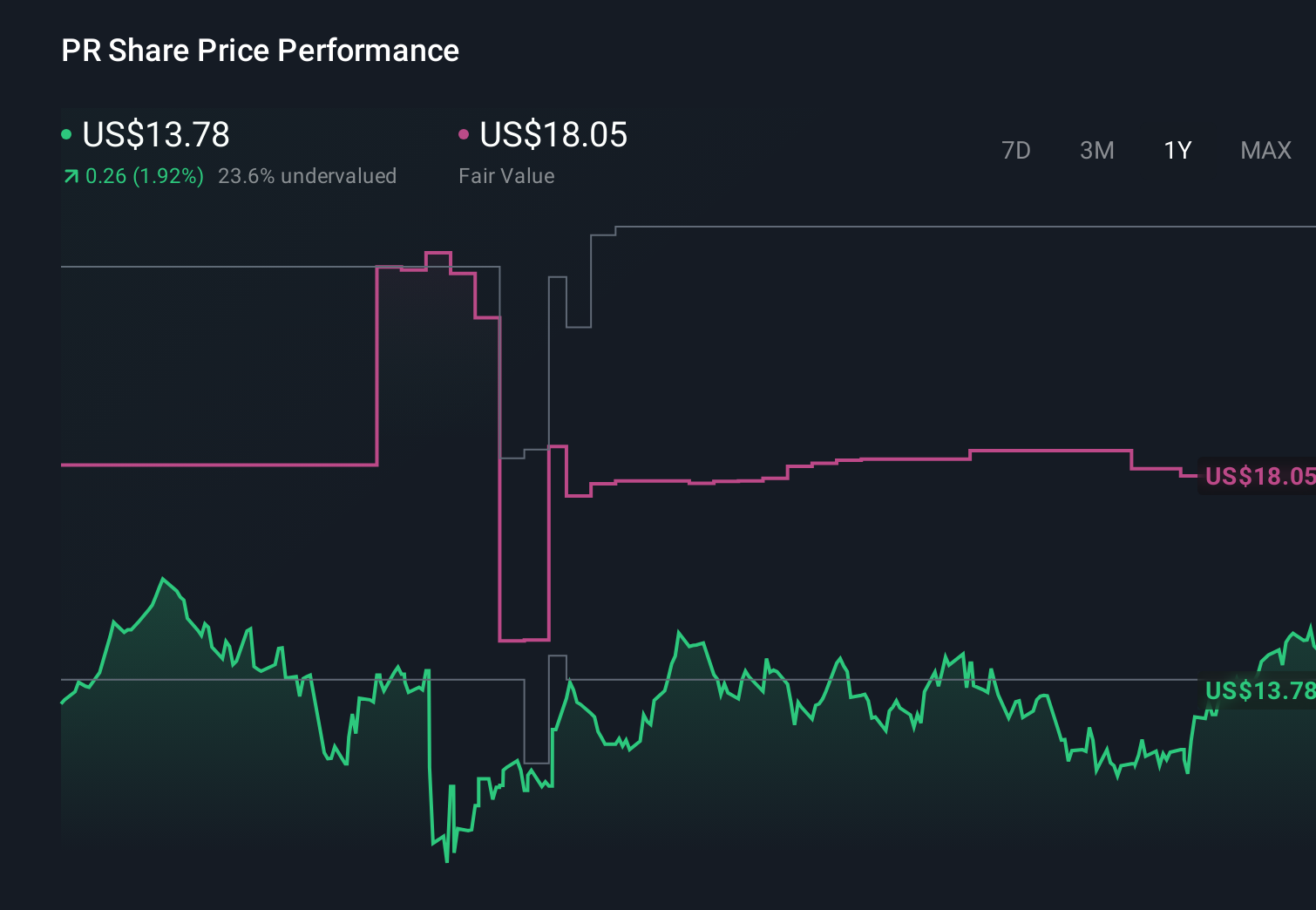

Permian Resources' narrative projects $6.4 billion revenue and $1.3 billion earnings by 2029.

Uncover how Permian Resources' forecasts yield a $23.90 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$7.1 billion and earnings US$3.0 billion by 2028, which contrasts sharply with the more cautious view that rising regulatory and environmental costs could pressure margins, reminding you that this new analyst enthusiasm might still reshape both the bullish and the more conservative narratives over time.

Explore 6 other fair value estimates on Permian Resources - why the stock might be worth 16% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Permian Resources research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.