Did GE’s (GE) New Defense Engine Order and Buybacks Just Reframe Its Aerospace Focus?

GE Aerospace GE | 0.00 |

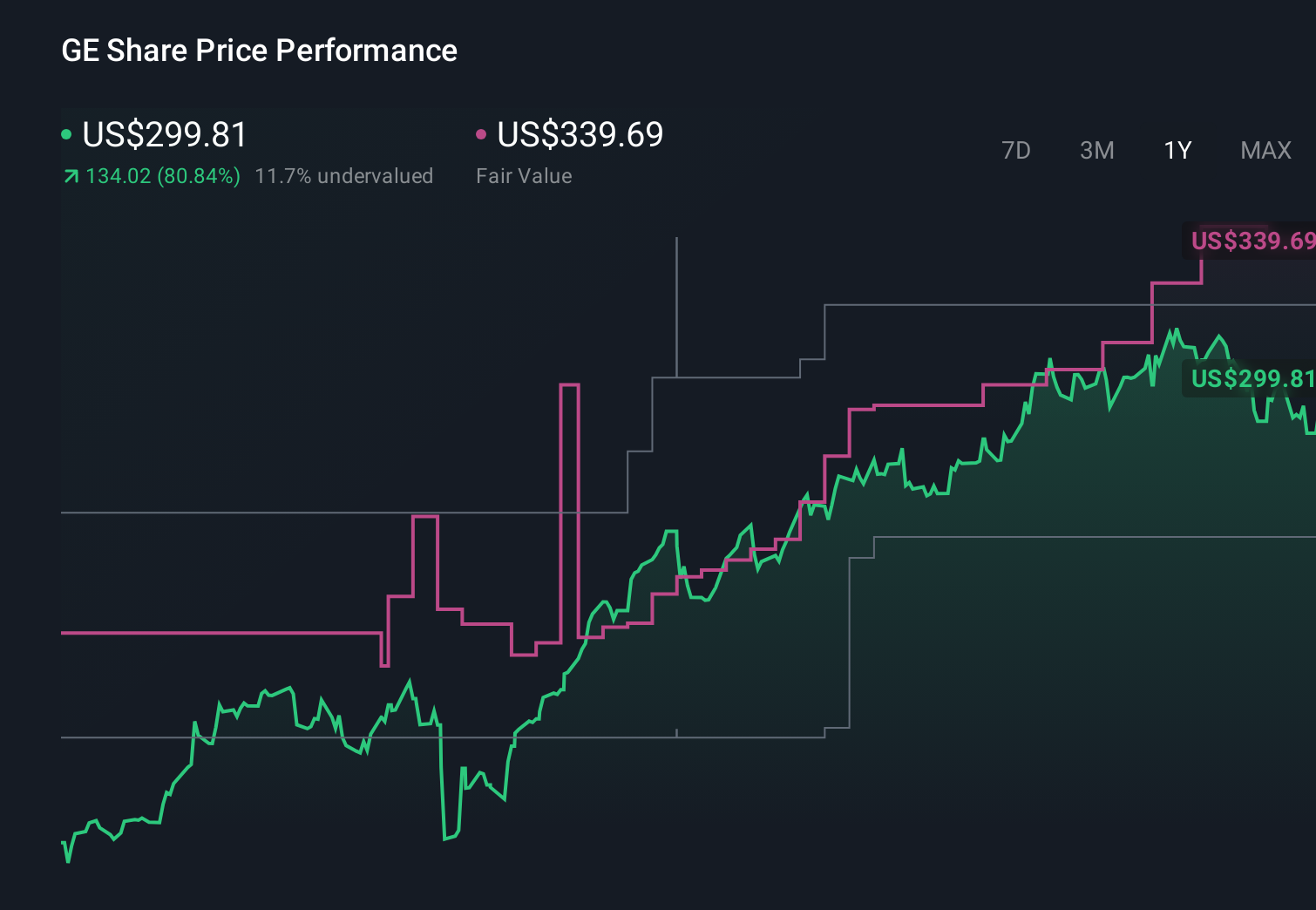

- In the first quarter of 2026, General Electric reported revenue of US$12,392 million, slightly lower net income of US$1,904 million, steady earnings per share, and continued its multi-year US$14.46 billion share repurchase program while securing a US$107.8 million U.S. defense engine contract.

- Beyond the headline numbers, the combination of expanding aerospace defense work and disciplined capital returns through buybacks highlights how GE is reinforcing its focus as a pure-play aerospace company.

- We’ll now examine how this new long-term U.S. defense engine order shapes General Electric’s existing investment narrative around aerospace growth.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

General Electric Investment Narrative Recap

To own General Electric today, you need to believe in its transformation into a focused aerospace engine and services business, with long-cycle defense and commercial contracts underpinning cash flows despite exposure to air travel trends and supply chain pressures. The new US$107.8 million J85 engine order modestly supports the near term defense catalyst, but does not materially change the biggest risk, which remains a potential prolonged slowdown in commercial aviation demand.

The most relevant recent announcement here is GE’s first quarter 2026 result, which showed US$12,392 million in revenue and US$1,904 million in net income, alongside ongoing share repurchases under the US$14.46 billion buyback. Together with the fresh J85 defense order, this underscores how current performance and capital returns are already tied to the core aerospace engine franchise that many investors view as the key earnings driver.

Yet even with these positives, investors should still be aware of how exposed GE remains to any sustained weakness in global air travel and tighter defense export scrutiny...

General Electric's narrative projects $59.2 billion revenue and $10.8 billion earnings by 2029. This requires 7.0% yearly revenue growth and about a $2.2 billion earnings increase from $8.6 billion today.

Uncover how General Electric's forecasts yield a $350.45 fair value, a 22% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts, who already saw revenue reaching about US$62.1 billion and earnings near US$12.1 billion by 2029, lean heavily on rapid services growth and advanced propulsion wins, while the latest defense engine award could either reinforce or temper that view depending on how you judge the added geopolitical and regulatory risks.

Explore 9 other fair value estimates on General Electric - why the stock might be worth as much as 48% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Electric research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.