Did New AI Partner Integrations Just Shift Snowflake's (SNOW) Enterprise Data Ecosystem Narrative?

Snowflake SNOW | 0.00 |

- In recent weeks, ManageMy and o9 Solutions have each announced past integrations with Snowflake’s AI Data Cloud, while Blend achieved Snowflake Elite Partner status and Crunchbase highlighted that more than 1,300 Snowflake Partner Network firms have raised over US$113.00 billions in funding since 2020.

- Together, these developments underscore Snowflake’s role at the center of an expanding enterprise data and AI ecosystem, where partners embed its platform into real-time insurance, supply chain, and decisioning workflows.

- Against this backdrop, we’ll examine how Snowflake’s deeper AI-focused integrations with partners like ManageMy and o9 Solutions may influence its existing investment narrative.

Find 49 companies with promising cash flow potential yet trading below their fair value.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe it can stay central to how enterprises store, govern, and activate data for AI, despite rising competition and ongoing losses. The near term catalyst is whether AI products like Cortex and Snowflake Intelligence can drive broader, durable usage beyond migration-led spikes. The biggest risk remains that AI-native and bundled cloud offerings compress Snowflake’s pricing power. The latest partner news reinforces the AI story but does not materially change that risk balance yet.

Among the latest announcements, o9 Solutions’ Connected Application for Snowflake looks especially relevant. By letting large manufacturers and retailers run AI-driven planning directly on governed data in Snowflake, it ties day to day supply chain and financial decisions more tightly to Snowflake’s platform. For investors focused on catalysts, this kind of closed loop integration shows how Snowflake can move from being a passive data warehouse to an active decisioning backbone across critical enterprise workflows.

Yet against this promise, investors should still watch how competition from AI native and bundled cloud platforms could quietly reshape Snowflake’s long term pricing power and customer loyalty...

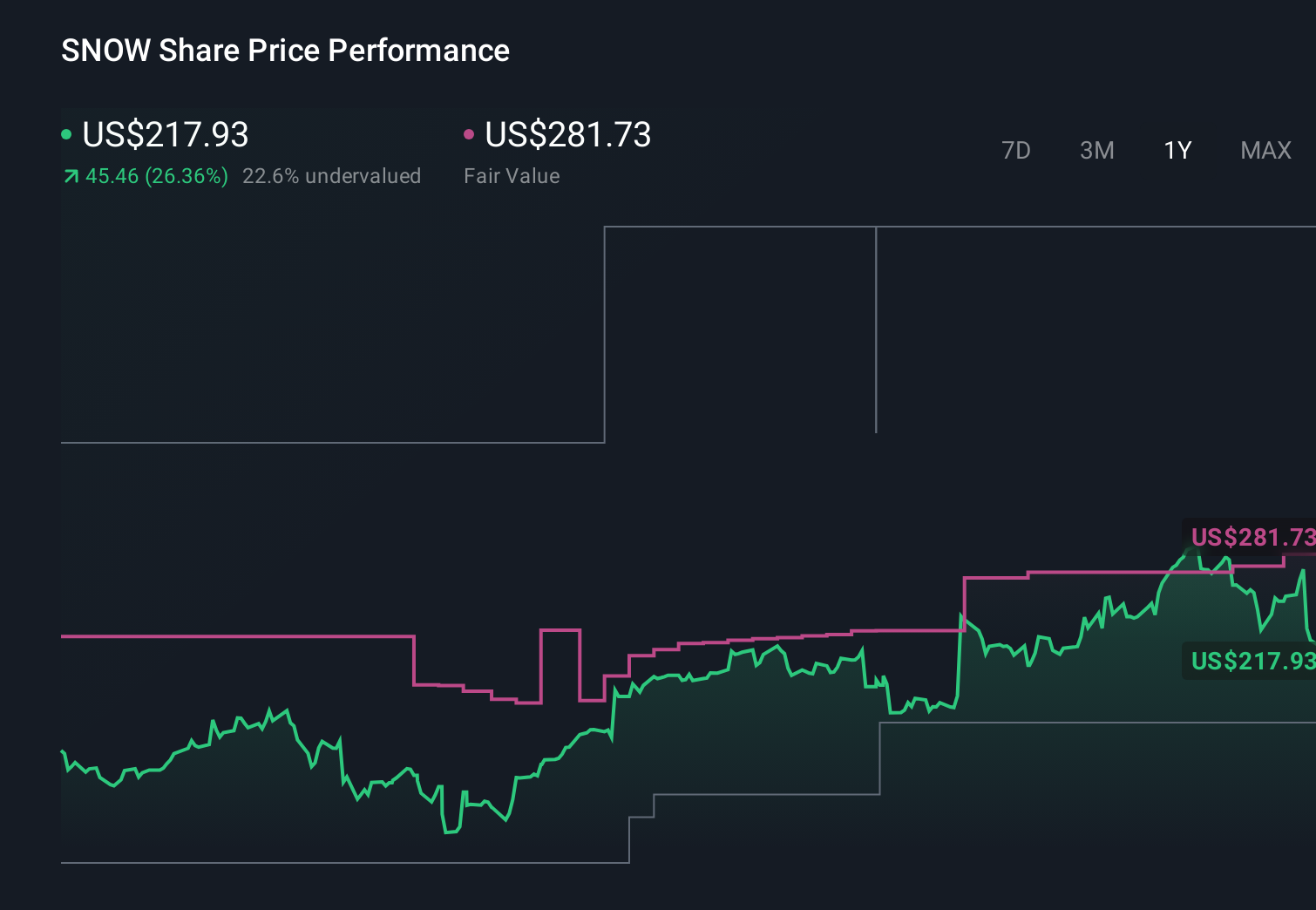

Snowflake’s narrative projects $9.0 billion revenue and $689.7 million earnings by 2029. This requires 24.5% yearly revenue growth and an earnings increase of about $2.0 billion from -$1.3 billion today.

Uncover how Snowflake's forecasts yield a $232.74 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were assuming about 22.6% annual revenue growth and no profits in three years, so compared with the partnership driven upside story, their view of AI driven competition and margin pressure is far more pessimistic and a useful reminder that your own opinion on Snowflake should be tested against very different forecasts.

Explore 14 other fair value estimates on Snowflake - why the stock might be worth 50% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Snowflake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.