Did Old National Bancorp’s (ONB) Top CRA Rating Just Recast Its Regulatory and Community Profile?

Old National Bancorp ONB | 23.64 23.64 | +1.68% 0.00% Pre |

- Old National Bank recently received an "Outstanding" overall rating, the highest possible, under the Community Reinvestment Act, recognizing its efforts to support affordable housing, economic development, and services for low- and moderate-income communities with nearly US$2.40 billion in qualifying loans from 2022 to 2024.

- This top-tier CRA rating highlights the bank’s governance and community focus, factors that can matter for how investors view regulatory quality and long-term franchise strength.

- We’ll now examine how Old National’s top-tier Community Reinvestment Act rating could influence the bank’s investment narrative and perceived risk profile.

Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

Old National Bancorp Investment Narrative Recap

To own Old National Bancorp, you need to believe in a disciplined regional bank that balances growth with credit and regulatory discipline, including meaningful engagement in its communities. The new “Outstanding” CRA rating reinforces perceptions of governance strength, but does not materially change the near term focus on integrating recent growth initiatives or the key risk around Old National’s concentrated exposure to commercial real estate and the Midwest centric footprint.

Among recent announcements, the “Outstanding” CRA rating stands out because it directly relates to regulatory quality, community relationships, and franchise reputation. For investors watching catalysts such as the Bremer expansion and ongoing digital investments, this endorsement from regulators can support confidence in Old National’s risk management framework at a time when the bank is still carrying a sizeable commercial real estate portfolio and managing through evolving industry regulation.

Yet against this positive backdrop, investors should also be aware of the heightened risk tied to Old National’s concentrated commercial real estate book and how it could...

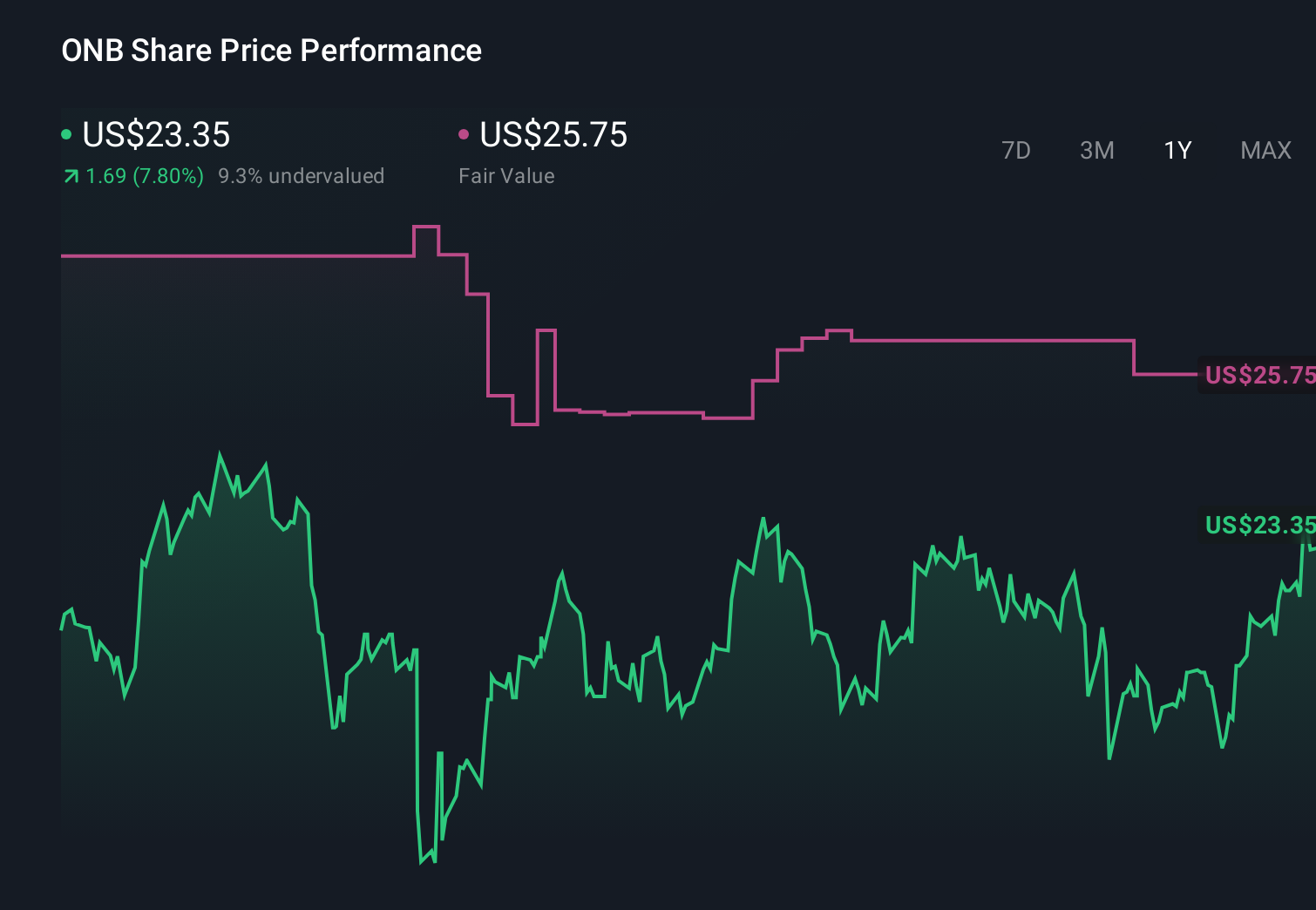

Old National Bancorp's narrative projects $3.2 billion revenue and $1.3 billion earnings by 2029.

Uncover how Old National Bancorp's forecasts yield a $27.38 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community range from about US$27 to over US$12,000 per share, underscoring how far apart individual views can be. Against this wide dispersion, Old National’s CRA “Outstanding” rating and its still meaningful commercial real estate exposure give you concrete factors to weigh as you compare these different perspectives on the bank’s future performance.

Explore 3 other fair value estimates on Old National Bancorp - why the stock might be a potential multi-bagger!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Old National Bancorp research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Old National Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Old National Bancorp's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 63 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.