Did Petrobras’ 3‑Year West Polaris Extension Just Shift Seadrill’s (SDRL) Offshore Investment Narrative?

Seadrill Limited SDRL | 47.05 | +2.17% |

- In early April 2026, Seadrill Limited announced that its ultra-deepwater drillship West Polaris secured a 1,095-day contract extension with Petrobras for the Búzios field in Brazil, adding about US$480 million to its backlog and updating dayrates through January 2028 to US$409,200 and then US$454,700.

- This long-term extension enhances Seadrill’s revenue visibility in a key offshore basin and underscores continued demand for high-spec ultra-deepwater capacity from major national oil companies.

- We’ll now examine how this long-duration Petrobras extension, and the added contract backlog, may influence Seadrill’s existing investment narrative.

Find 59 companies with promising cash flow potential yet trading below their fair value.

Seadrill Investment Narrative Recap

To own Seadrill, you need to believe that tight supply of modern ultra deepwater rigs and growing offshore activity can translate into a fuller backlog and better utilization, even as the company works through recent losses and an inexperienced management bench. The West Polaris extension strengthens near term revenue visibility but does not remove key risks around dayrate pressure, idle rigs, and legal or regulatory overhangs, so the core risk reward profile feels broadly intact for now.

The recent appointment of Samir Ali as CEO is particularly relevant alongside the West Polaris news. A new leader stepping in just as Seadrill secures multi year work with Petrobras puts execution squarely in focus: investors will be watching how effectively this management team converts the expanding backlog into steadier earnings, while balancing capital allocation choices such as buybacks against the need to manage legal exposures and aging assets.

Yet beneath the contract wins, investors should still be aware of how unresolved legal claims and potential cash outflows could...

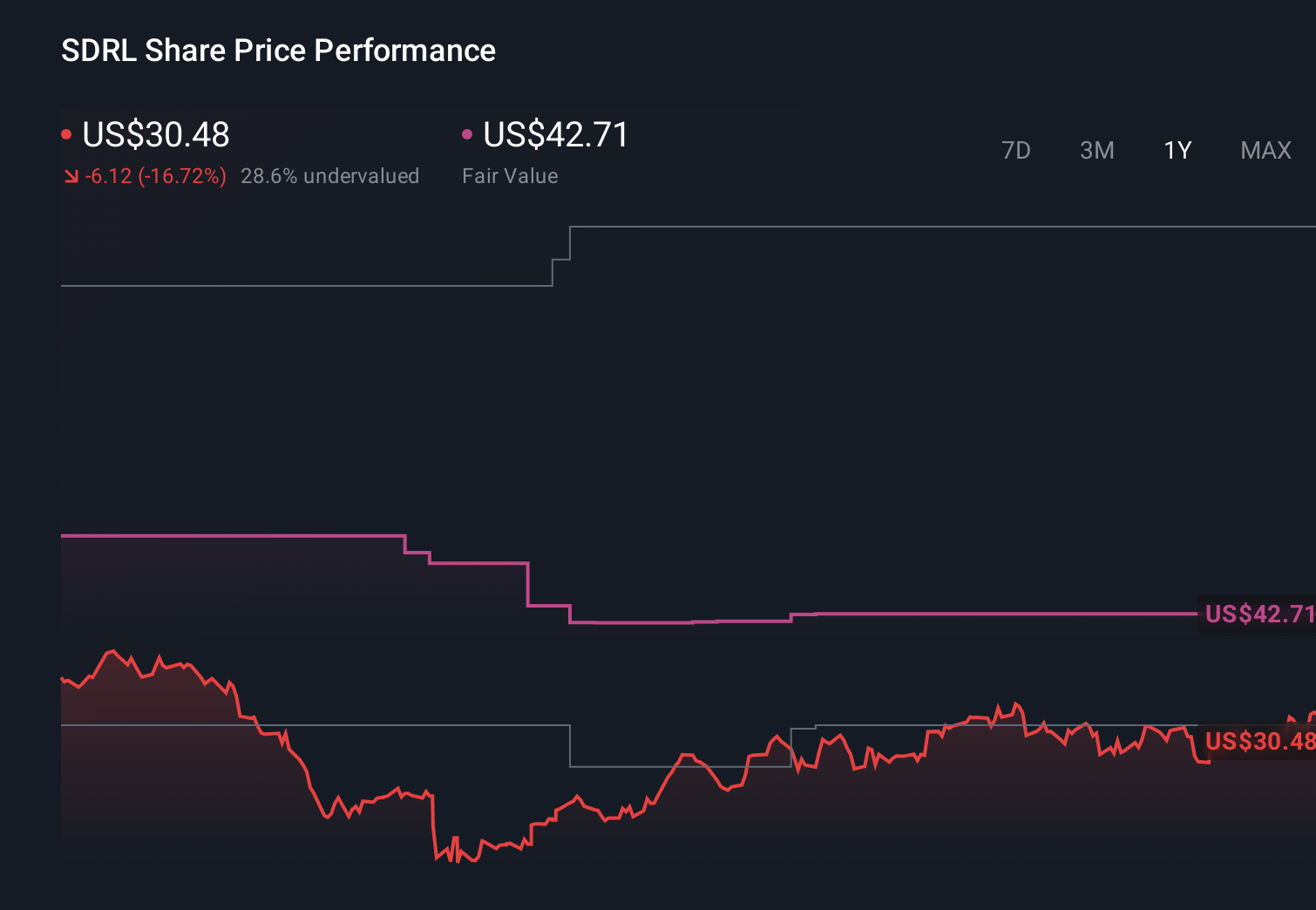

Seadrill's narrative projects $1.6 billion revenue and $231.6 million earnings by 2028. This requires 7.2% yearly revenue growth and a $154.6 million earnings increase from $77.0 million today.

Uncover how Seadrill's forecasts yield a $43.50 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 3.6 percent annual revenue growth to roughly US$1.5 billion and 2029 earnings of about US$219 million, highlighting how views on long term contract demand and cash flow resilience can differ sharply from the more optimistic backlog driven story around this Petrobras extension.

Explore 7 other fair value estimates on Seadrill - why the stock might be worth over 8x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

No Opportunity In Seadrill?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.