Did Pine Hill’s Weather-Driven Shutdown Just Recast International Paper’s (IP) Operational Resilience Narrative?

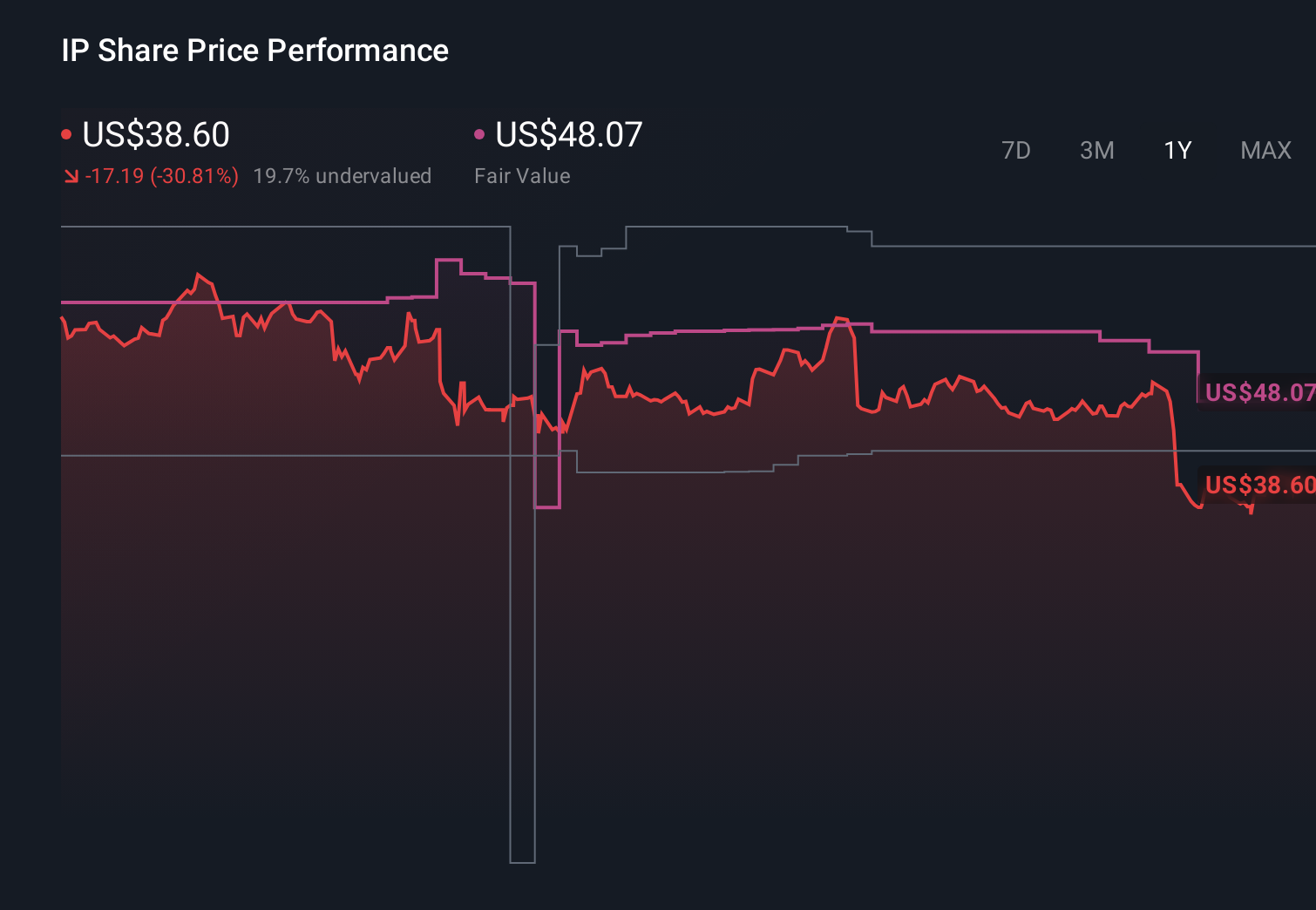

International Paper Company IP | 0.00 |

- International Paper recently suspended operations at its Pine Hill, Alabama mill after severe weather damaged a critical roof, and it is assessing repairs with an expectation of resuming manufacturing in August while coordinating closely with customers.

- This disruption, combined with ongoing North American facility closures and prior earnings pressures, highlights how operational resilience and network optimization remain central to International Paper’s story.

- We’ll now examine how the temporary Pine Hill shutdown, alongside broader footprint changes, affects International Paper’s investment narrative and risk profile.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

International Paper Investment Narrative Recap

To own International Paper, you need to believe its packaging-focused transformation, cost reductions, and mill reliability work can restore consistent profitability despite recent losses and industry headwinds. The Pine Hill shutdown spotlights operational resilience as the key short term catalyst and risk, but its temporary nature means the bigger question remains whether ongoing footprint changes and reliability investments can steadily translate into more durable earnings.

The recent decision to close several North American facilities by the end of the third quarter 2026 is particularly relevant here, as it underlines how International Paper is reshaping its network while simultaneously managing unplanned outages like Pine Hill. Those planned closures, alongside customer transitions to other plants, sit at the heart of the margin improvement and cost efficiency story many investors are watching most closely.

Yet, against this backdrop of transformation, investors should also be aware that...

International Paper's narrative projects $26.2 billion revenue and $1.7 billion earnings by 2029. This requires 2.5% yearly revenue growth and a $4.3 billion earnings increase from -$2.6 billion today.

Uncover how International Paper's forecasts yield a $39.36 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about 2 percent annual revenue growth and earnings of roughly US$1.8 billion by 2029, so events like Pine Hill could easily make their more pessimistic view on mill reliability and cash generation look more reasonable or too harsh, depending on how the recovery unfolds.

Explore 4 other fair value estimates on International Paper - why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your International Paper research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.