Did Q3 Results and EvolutionIQ Integration Just Shift CCC Intelligent Solutions Holdings' (CCC) Investment Narrative?

CCC Intelligent Solutions Holdings Inc CCC | 0.00 |

- CCC Intelligent Solutions Holdings Inc. recently announced its Q3 2025 results, exceeding revenue estimates while highlighting ongoing challenges from lower claims volumes and integration of the EvolutionIQ acquisition.

- Despite consolidating operations and increasing share buybacks to offset high stock-based compensation, the company continues to trade at a premium valuation amid slower growth and reduced retention rates.

- We will explore how the continued operational challenges and EvolutionIQ integration are now influencing CCC's broader investment outlook.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

CCC Intelligent Solutions Holdings Investment Narrative Recap

To believe in CCC Intelligent Solutions Holdings, shareholders must have confidence in the company’s ability to drive long-term growth through the digitization of auto insurance claims, even as transactional volumes decline. The Q3 2025 results confirmed revenue outperformance, but operational headwinds like persistent claims volume pressure and the integration of EvolutionIQ remain the key short-term risk; there is no indication these recent results materially shift the main catalyst, which is broad adoption of CCC’s advanced AI solutions.

The most relevant recent announcement is the continued execution of the company’s share buyback program, with over 22.7 million shares repurchased to date. This move speaks directly to management’s ongoing effort to offset high stock-based compensation and support shareholder value, though it does not alter the influence of ongoing claims softness or integration challenges, both critical to the near-term investment outlook.

In contrast, while the company’s recurring revenue model provides some resilience, investors should stay mindful of risks associated with concentrated customer exposure if…

CCC Intelligent Solutions Holdings' narrative projects $1.3 billion in revenue and $184.1 million in earnings by 2028. This requires 9.3% yearly revenue growth and a $182.2 million earnings increase from current earnings of $1.9 million.

Uncover how CCC Intelligent Solutions Holdings' forecasts yield a $11.75 fair value, a 62% upside to its current price.

Exploring Other Perspectives

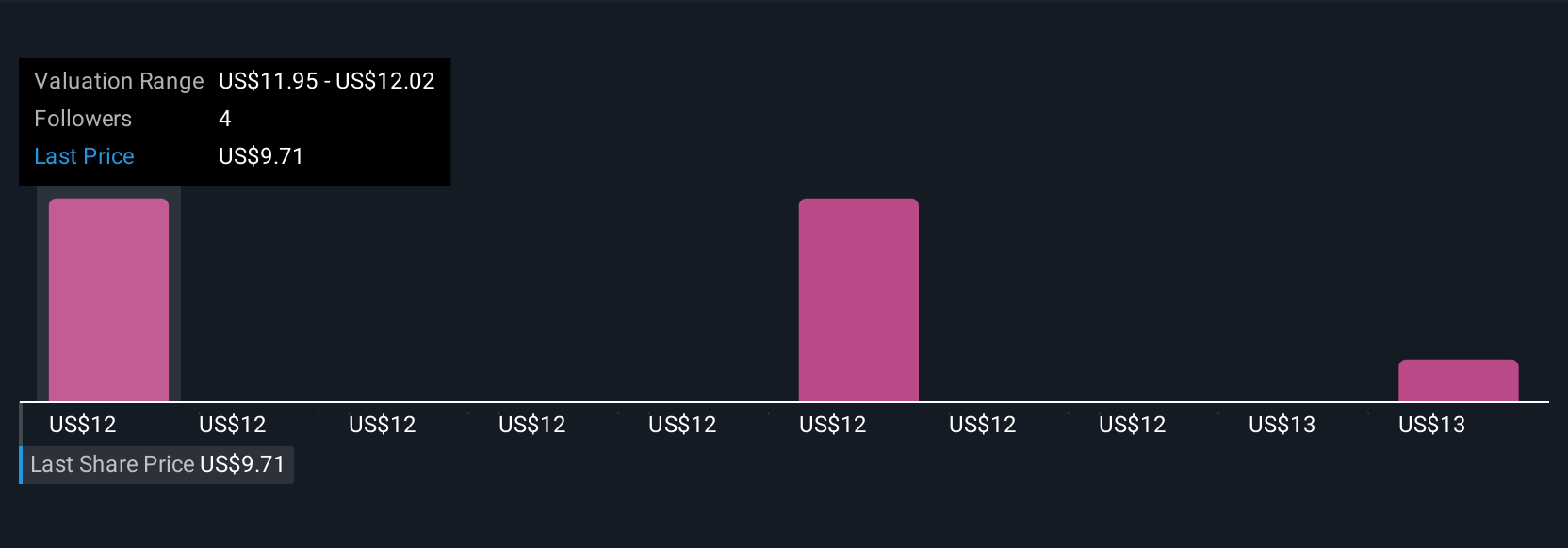

Four community members on Simply Wall St estimated CCC's fair value in a tight US$11.75 to US$12.65 range. Against this backdrop, ongoing integration challenges for EvolutionIQ may further differentiate opinions on CCC’s path to sustained growth.

Explore 4 other fair value estimates on CCC Intelligent Solutions Holdings - why the stock might be worth as much as 74% more than the current price!

Build Your Own CCC Intelligent Solutions Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CCC Intelligent Solutions Holdings research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free CCC Intelligent Solutions Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CCC Intelligent Solutions Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.