Did Recent Insider Sells and Sector Gains Just Shift Benchmark Electronics' (BHE) Investment Narrative?

Benchmark Electronics, Inc. BHE | 57.29 57.29 | +2.19% 0.00% Post |

- Recently, Jan Janick, Senior Vice President and Chief Technology Officer at Benchmark Electronics, sold 8,967 shares shortly after the company reported strong Q3 2025 results with notable gains in its medical and aerospace & defense segments.

- The move adds to a pattern of insider sells over the past year while Benchmark’s operational momentum in higher-growth sectors has drawn attention to its evolving market mix and leadership actions.

- We'll explore how Benchmark's robust performance in medical and aerospace & defense sectors may shape its outlook and investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Benchmark Electronics Investment Narrative Recap

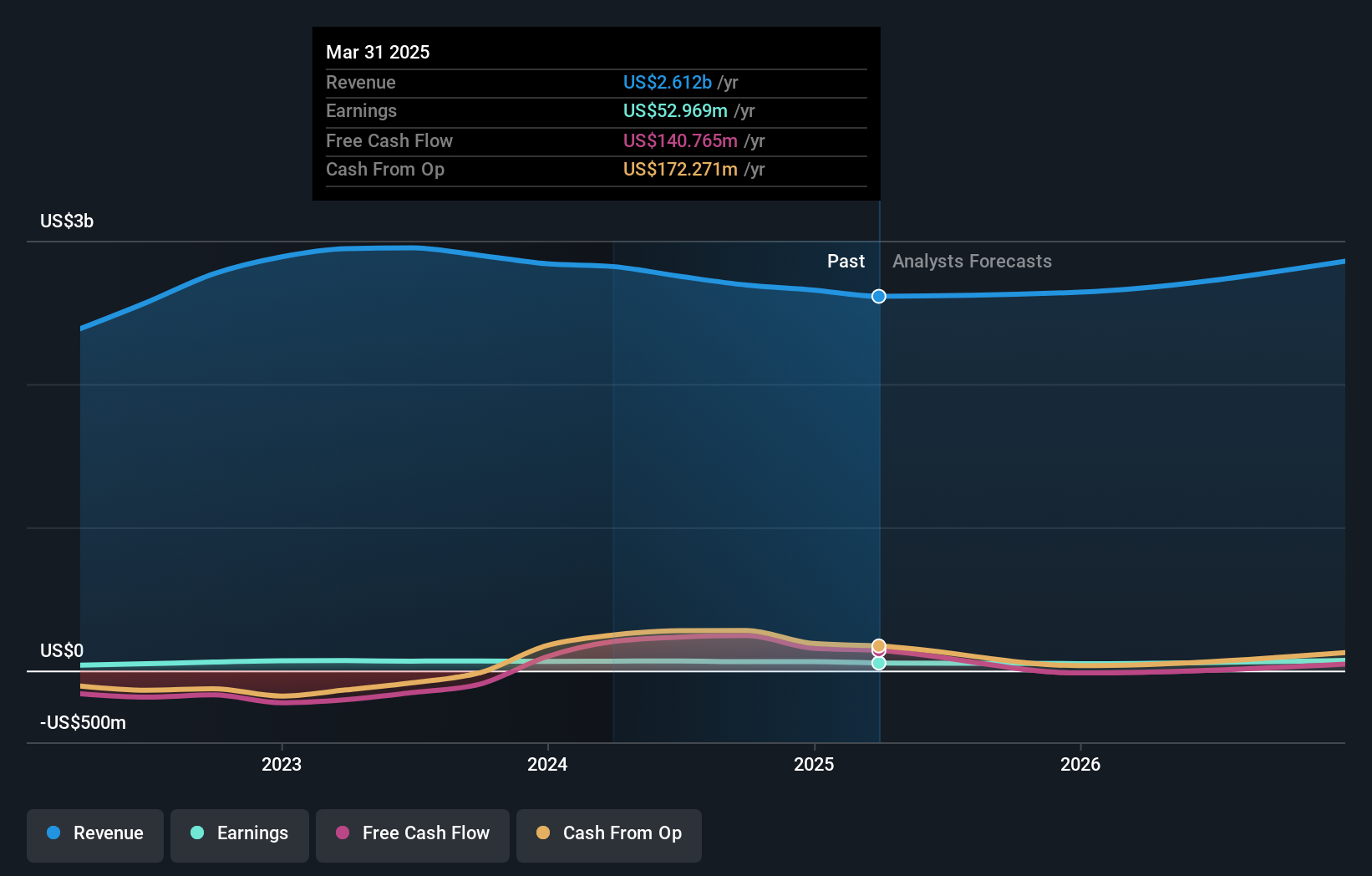

To be a shareholder in Benchmark Electronics, you need to believe the company can convert growth in medical and aerospace & defense into sustained profitability, even with pressures in other segments like semiconductors. The recent insider sale by a key executive shines a light on leadership activity, but it does not appear to alter near-term expectations tied to Benchmark’s recent sector gains; risks such as ongoing semi-cap weakness and margin stresses remain the more pressing issues to watch. The company’s upbeat Q3 2025 results, where robust medical and aerospace & defense growth offset softness elsewhere, highlight why these segments are front and center as Benchmark’s main short-term drivers. Continued momentum here is meaningful, given guidance for higher Q4 earnings per share and resilience despite margin challenges in legacy business lines. Yet, in contrast to recent positive headlines, the risk of renewed inventory build-up in the medical segment is an area investors should be aware of…

Benchmark Electronics' outlook anticipates $3.0 billion in revenue and $95.5 million in earnings by 2028. This is based on a 5.3% annual revenue growth rate and an increase in earnings of $57.1 million from the current $38.4 million.

Uncover how Benchmark Electronics' forecasts yield a $47.33 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Fair value estimates from three Simply Wall St Community members range from US$17.20 to US$47.33. While some expect high earnings growth in coming years, sector headwinds and margin pressures could challenge sustained performance.

Explore 3 other fair value estimates on Benchmark Electronics - why the stock might be worth less than half the current price!

Build Your Own Benchmark Electronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Benchmark Electronics research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Benchmark Electronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Benchmark Electronics' overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.