Did Repeated Earnings Beats and a Positive ESP Just Shift Crescent Energy's (CRGY) Investment Narrative?

Crescent Energy CRGY | 0.00 |

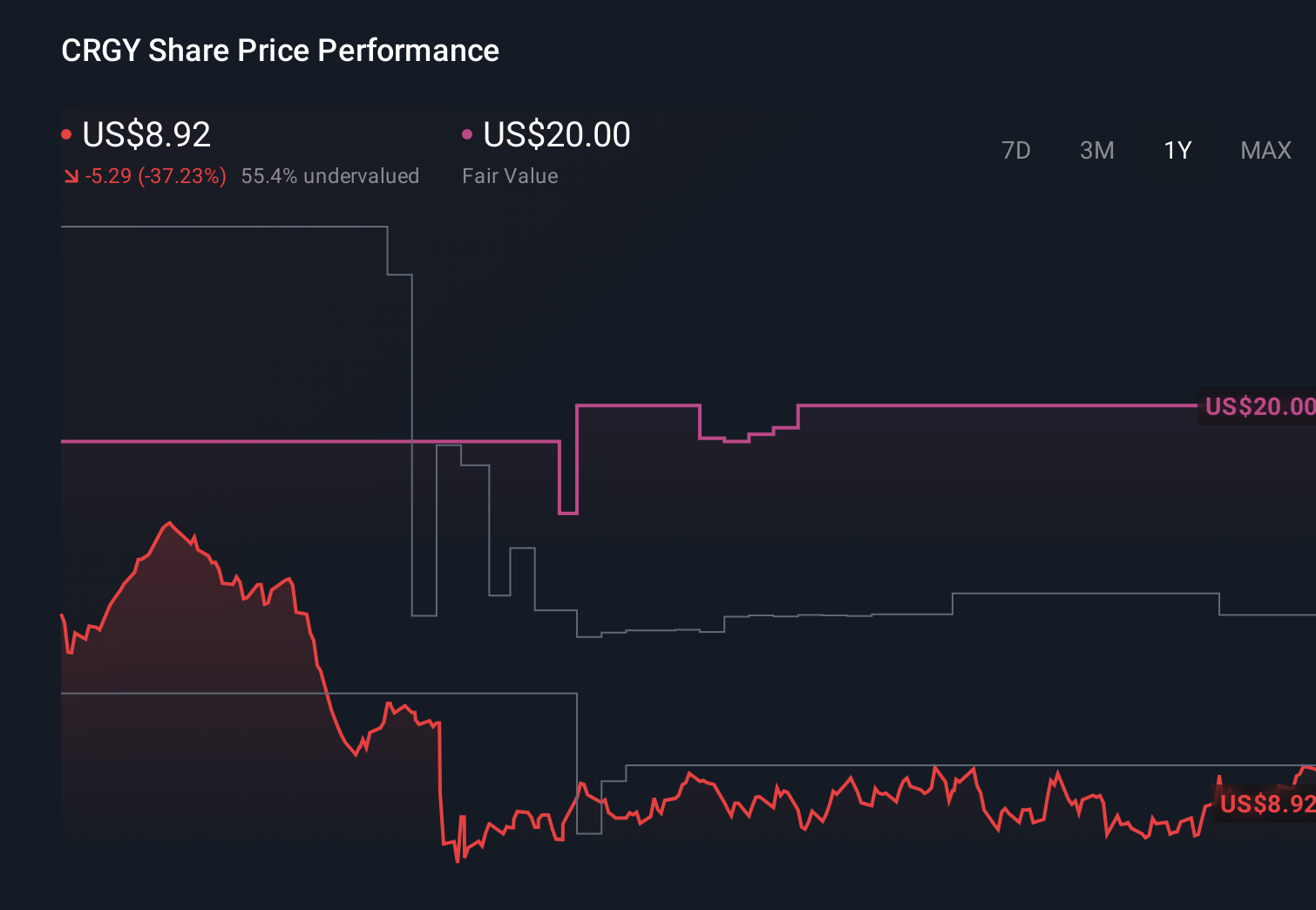

- Recently, Crescent Energy’s earnings reports have come in well ahead of analyst expectations, with the company outperforming consensus estimates by an average of very large in the last two quarters.

- With a positive Zacks Earnings ESP and a Zacks Rank #3 (Hold), recent analyst commentary points to growing confidence that Crescent Energy could once again exceed near-term earnings expectations.

- Next, we’ll examine how this pattern of recent earnings outperformance and a positive Earnings ESP may influence Crescent Energy’s investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Crescent Energy Investment Narrative Recap

To own Crescent Energy, you need to believe its acquisition driven model and U.S. oil and gas footprint can translate improving operations into durable cash generation, despite commodity and regulatory uncertainty. The recent pattern of earnings beats and a positive Zacks Earnings ESP sharpens the focus on near term earnings execution as a key catalyst, while the biggest risk remains that deals or capital intensity fail to translate into consistent, high quality profitability. So far, this news does not materially change that risk profile.

One recent development that ties closely to this earnings focused story is Crescent’s expanded US$400 million share buyback authorization, with an indefinite duration. When paired with stronger than expected earnings, this capital return tool can reinforce the investment case that management is confident in underlying cash flows. At the same time, using buybacks alongside ongoing acquisitions raises fair questions about balance sheet resilience if commodity prices soften or acquired assets underperform.

Yet behind the upbeat earnings surprises, investors should also be aware of the risk that rising leverage and acquisition dependence could...

Crescent Energy's narrative projects $4.4 billion revenue and $625.9 million earnings by 2029. This requires 4.7% yearly revenue growth and a $910.7 million earnings increase from -$284.8 million today.

Uncover how Crescent Energy's forecasts yield a $17.36 fair value, a 84% upside to its current price.

Exploring Other Perspectives

While recent earnings surprises look encouraging, the most pessimistic analysts once projected US$4.4 billion revenue and US$575.3 million earnings by 2029, reminding you that views can diverge sharply and may shift again after this news.

Explore 4 other fair value estimates on Crescent Energy - why the stock might be worth over 4x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crescent Energy research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.