Did Strong Billings Growth Just Shift Braze's (BRZE) Investment Narrative?

Braze, Inc. Class A BRZE | 23.61 | +0.51% |

- Recently, coverage highlighted that Braze achieved billings growth of 24.4% over the past year and is projected to deliver 19.2% revenue growth in the next 12 months.

- This reinforces a positive perspective on Braze's potential in the highly competitive customer engagement software sector, emphasizing its strong momentum in expanding customer adoption and recurring revenues.

- We'll now assess how the upbeat outlook for Braze’s billings and revenue growth may shape its overall investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Braze Investment Narrative Recap

For shareholders in Braze, the core belief centers on the company’s ability to cement its position as a leading customer engagement platform amid tough competition. The recent news of strong billings and projected revenue growth underscores the appeal of Braze’s momentum, yet does not fundamentally change the main immediate catalyst, expanding enterprise adoption, or the biggest risk, which remains the potential impact of integrating new technologies like OfferFit on operating margins and scalability.

Among Braze’s recent updates, the launch of BrazeAI products stands out as most connected to the current growth narrative. These AI-driven offerings aim to strengthen Braze’s ability to deliver more personalized and efficient customer campaigns, directly supporting the case for accelerating customer adoption, a key short-term catalyst highlighted by the latest growth figures.

In contrast, investors should keep a close eye on how integration challenges, particularly with...

Braze's narrative projects $1.0 billion revenue and $133.0 million earnings by 2028. This requires 17.9% yearly revenue growth and a $236.9 million increase in earnings from -$103.9 million.

Uncover how Braze's forecasts yield a $45.11 fair value, a 57% upside to its current price.

Exploring Other Perspectives

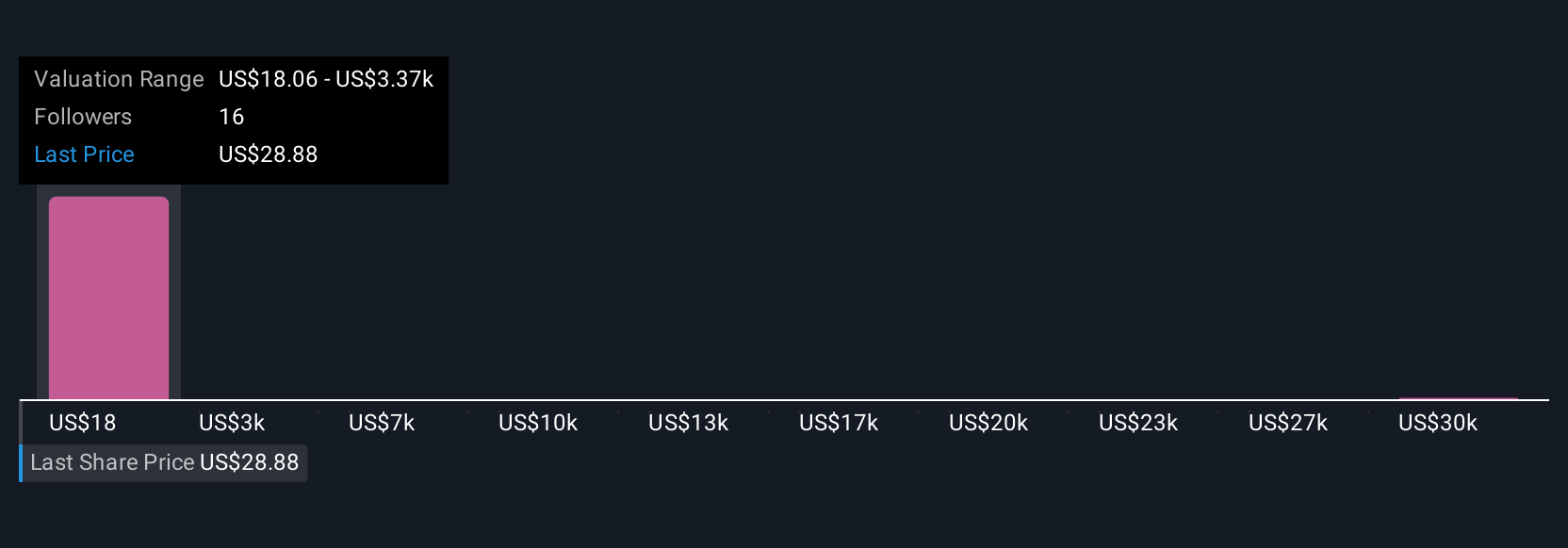

Five community-sourced fair value estimates for Braze range from US$25 to over US$33,500, reflecting exceptionally broad perspectives within the Simply Wall St Community. Yet, concerns remain about the company’s ability to achieve and sustain profitable growth alongside its ambitious AI and product roadmap, emphasizing the importance of considering multiple viewpoints.

Explore 5 other fair value estimates on Braze - why the stock might be a potential multi-bagger!

Build Your Own Braze Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Braze research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Braze research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Braze's overall financial health at a glance.

No Opportunity In Braze?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.