Did Strong Core Insurance Results Just Shift Mercury General's (MCY) Investment Narrative?

Mercury General Corporation MCY | 0.00 |

- Mercury General recently reported resilient core business performance in its personal auto and homeowners insurance lines, with operational results excluding catastrophe losses showing positive trends and underlying strength.

- This improvement in fundamental insurance metrics has captured market interest and may influence future confidence in Mercury General's growth prospects and earnings stability.

- Next, we'll explore how the company's solid underlying combined ratios signal potential implications for Mercury General's investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Mercury General Investment Narrative Recap

To be a shareholder in Mercury General, one needs to believe in the underlying resilience of its core personal auto and homeowners insurance business, especially as operational results excluding catastrophe losses remain favorable. The recent strong performance in underlying combined ratios has drawn attention, but ongoing exposure to catastrophic wildfires continues to represent the most significant short-term risk, while the main near-term catalyst is further improvement in core margins. The latest announcement does not materially alter these key factors.

Of recent updates, the Q2 2025 earnings report stands out, showing a sharp growth in quarterly net income to US$166.47 million from US$62.57 million a year ago. This financial recovery aligns with positive operational news and improves investor confidence in the company’s ability to withstand volatility from high-severity events, reinforcing the catalyst around core earnings growth.

In contrast, investors should be aware that the risk stemming from potential additional assessments through the California FAIR Plan could...

Mercury General's outlook anticipates $6.7 billion in revenue and $452.5 million in earnings by 2028. This projection relies on 5.1% annual revenue growth and a $62.4 million increase in earnings from the current $390.1 million.

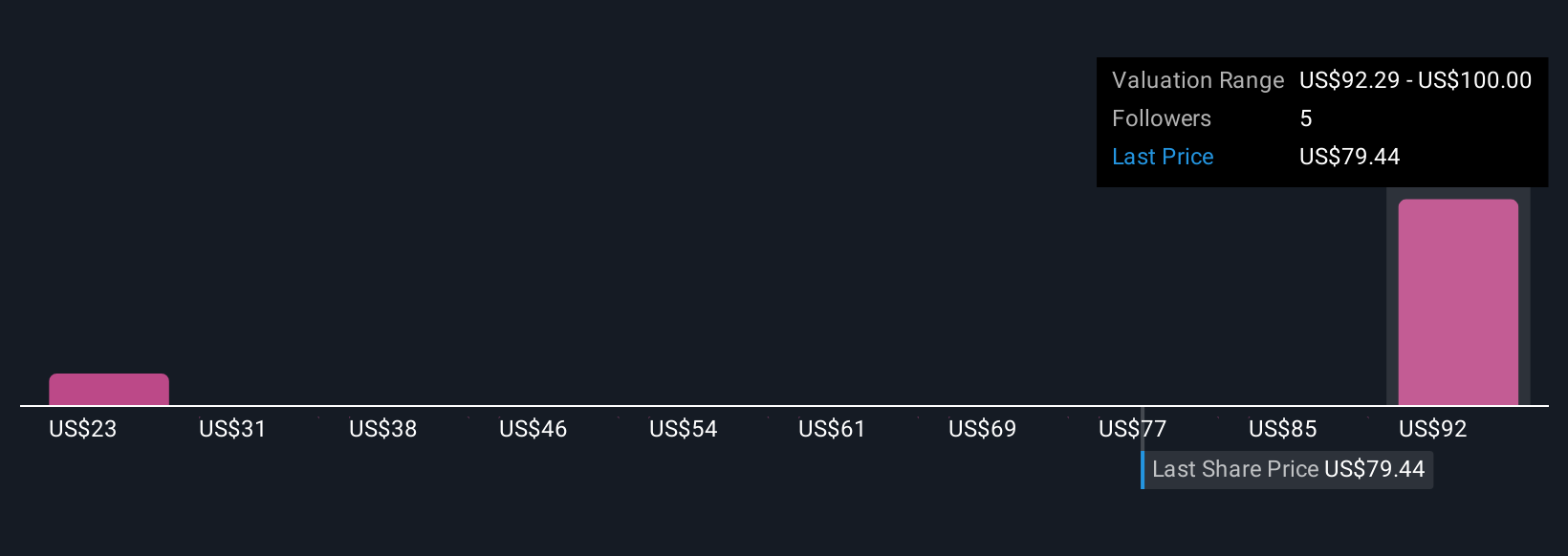

Uncover how Mercury General's forecasts yield a $100.00 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Fair value analyses from two Simply Wall St Community members put Mercury General between US$22.93 and US$100 per share. While opinions vary, the ongoing risk of increased reinsurance costs due to recent wildfires could influence long-term profitability and capital strength.

Explore 2 other fair value estimates on Mercury General - why the stock might be worth as much as 23% more than the current price!

Build Your Own Mercury General Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mercury General research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Mercury General research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mercury General's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.