Did Vulcan Materials' (VMC) Russell 1000 Dynamic Exit Just Reframe Its Demand-Resilience Story?

Vulcan Materials Company VMC | 0.00 |

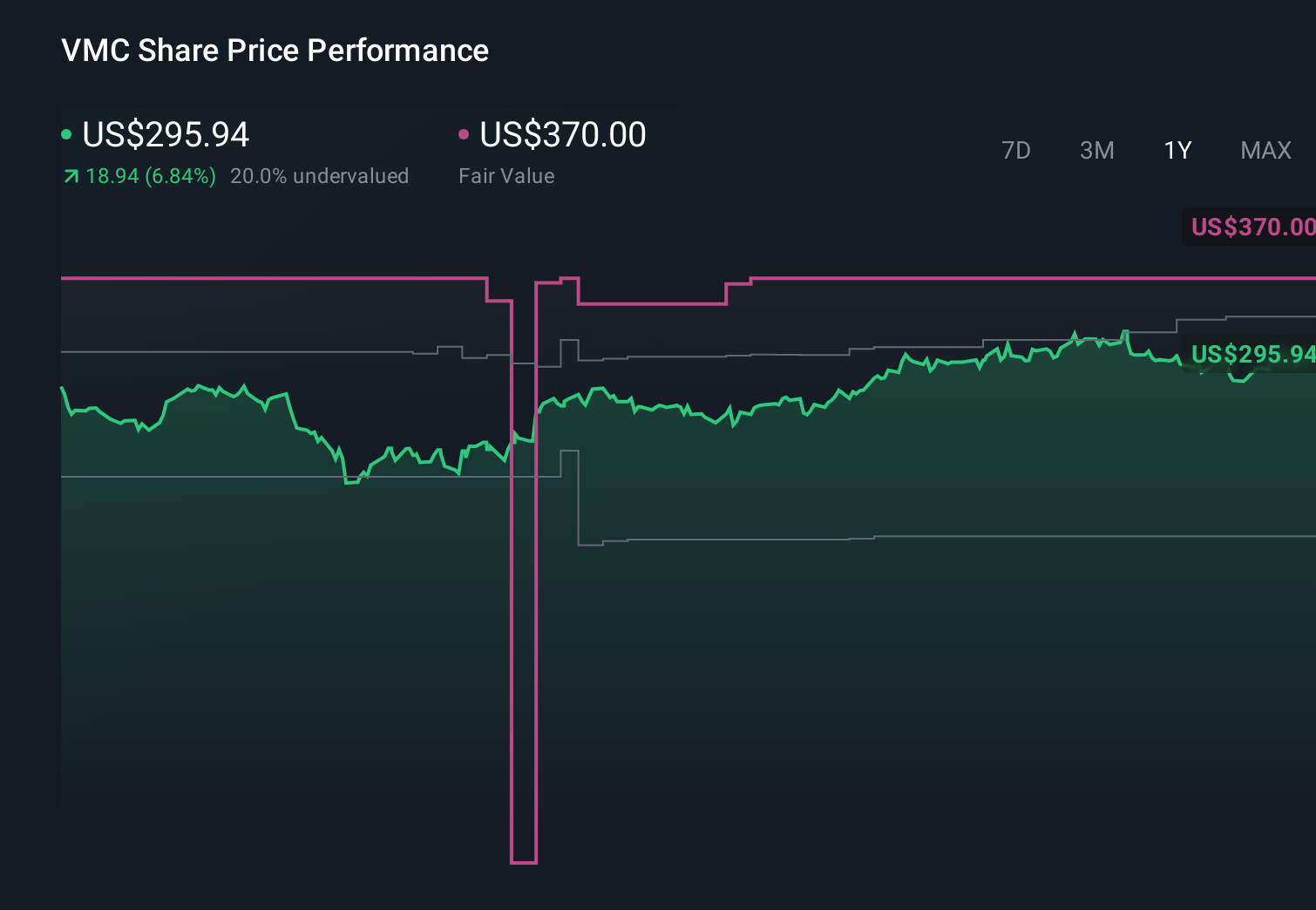

- Vulcan Materials Company (NYSE: VMC) was recently removed from the Russell 1000 Dynamic Index, prompting index-tracking investors to rebalance their holdings away from the stock.

- This index exit comes as Vulcan shows a mix of long-term financial strength and softer near-term demand signals, making the timing particularly important for portfolio positioning.

- We’ll now examine how Vulcan’s removal from the Russell 1000 Dynamic Index may influence its investment narrative and investor expectations.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you generally have to believe in steady, aggregate-driven cash generation tied to long-lived infrastructure and construction demand, even when near-term volumes soften. The removal from the Russell 1000 Dynamic Index is more about technical flows than fundamentals, and it does not materially change the key short term swing factor: how quickly softer demand in tons shipped stabilizes. The biggest risk right now remains any prolonged weakness or delays in Vulcan’s core construction end markets.

The most relevant recent announcement against this backdrop is Vulcan’s Q1 2026 earnings release, which showed US$1,755.9 million in sales and US$165.5 million in net income. Those results sit beside the softer tons shipped, highlighting how pricing, cost control and mix have supported profitability even as demand signals cool. For investors focused on catalysts, the question is whether that earnings resilience can hold if project delays in residential and public infrastructure persist or broaden.

Yet beneath Vulcan’s apparent resilience, there is a concentration and regulatory risk profile that investors should be aware of if...

Vulcan Materials’ narrative projects $9.6 billion revenue and $1.7 billion earnings by 2029. This requires 6.0% yearly revenue growth and about a $0.6 billion earnings increase from $1.1 billion today.

Uncover how Vulcan Materials' forecasts yield a $328.81 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some analysts are far more optimistic than consensus, assuming revenue can reach about US$9.6 billion and earnings US$1.9 billion before this index change, which may prompt you to ask how those upbeat expectations stack up against softer near term demand and the fresh signal from the Russell removal, and whether both bullish and cautious views might need to shift as the story evolves.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth 25% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.