Did Weak Billings and Margin Pressure Just Shift Teradata's (TDC) Investment Narrative?

Teradata TDC | 0.00 |

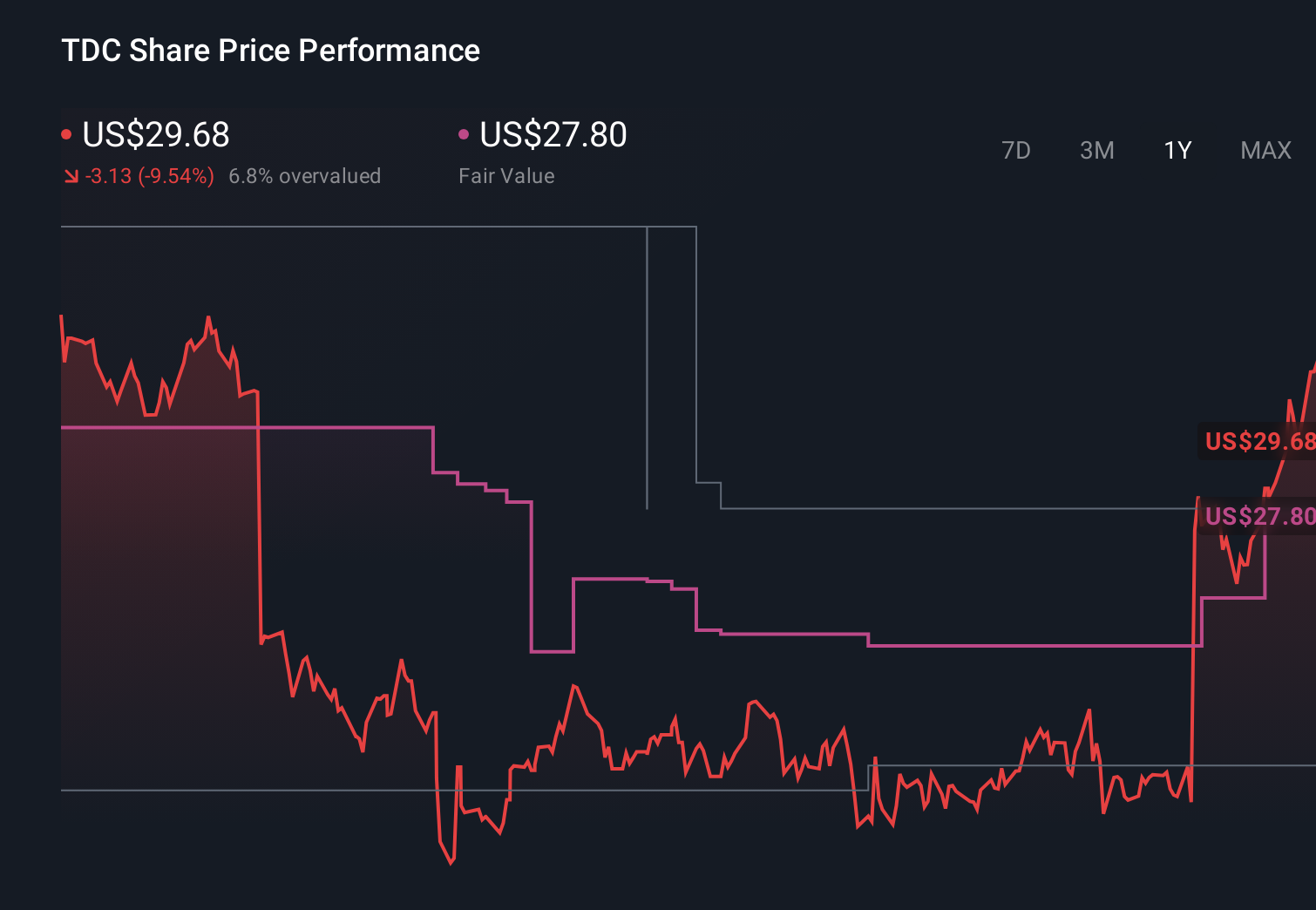

- In late May 2026, analysts expressed concern that Teradata’s weak billings, shrinking operating margin, and declining cash flow margin point to weakening fundamentals despite a reasonable valuation.

- This shift in sentiment highlights growing doubt about the strength and durability of Teradata’s business model at a time of elevated investor focus on profitability.

- We’ll now examine how these concerns about soft billings and margin pressure may affect Teradata’s previously outlined investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Teradata Investment Narrative Recap

To own Teradata today, you need to believe its AI and hybrid-cloud platform can sustain solid recurring revenues despite modest top-line growth. The recent worries about weak billings and compressing margins cut close to that thesis, because they touch both the key short term catalyst (profitable AI and cloud workload adoption) and the biggest current risk (evidence that demand and cash generation are softening). If these trends persist, they could materially alter the risk profile rather than being a passing blip.

The launch of the Teradata Autonomous Knowledge Platform in May 2026 is especially relevant here, as it is meant to concentrate data, analytics, and production AI across cloud and on-prem environments. This offering sits at the heart of the AI and GenAI catalyst many shareholders are counting on, but the latest concerns about underwhelming billings and cash flow margins raise a fair question about how quickly such new products are translating into durable, profitable customer demand.

Yet beneath the AI story, there is a separate risk investors should be aware of around weakening cash flow and what it could mean for...

Teradata's narrative projects $1.7 billion revenue and $102.4 million earnings by 2029. This implies fairly flat yearly revenue growth and an earnings decrease of $318.6 million from $421.0 million today.

Uncover how Teradata's forecasts yield a $33.44 fair value, in line with its current price.

Exploring Other Perspectives

The lowest analysts are far more pessimistic than consensus, assuming revenue slips to about US$1.6 billion and earnings fall to roughly US$87 million, which could look closer to reality if weak billings and margin pressure persist, so you should recognize how widely views on Teradata differ and be open to revisiting your own assumptions as new data comes in.

Explore 5 other fair value estimates on Teradata - why the stock might be worth 38% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Teradata research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Teradata research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradata's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Outshine the giants: these 12 early-stage AI stocks could fund your retirement.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.