Did Zscaler’s (ZS) Higher Revenue Outlook and Wider Losses Just Rewrite Its Zero‑Trust AI Story?

Zscaler, Inc. ZS | 0.00 |

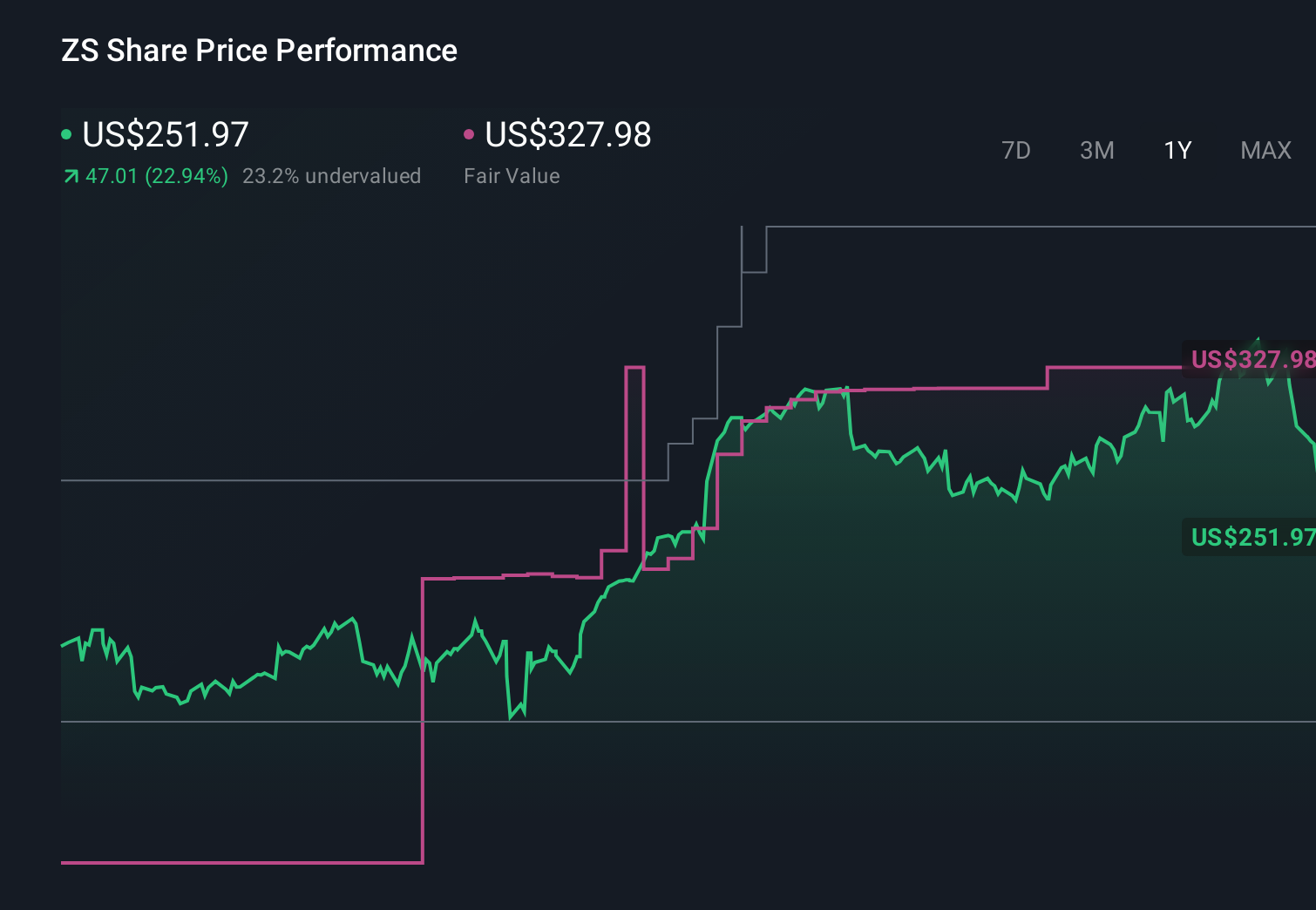

- In late May 2026, Zscaler reported third-quarter fiscal 2026 results showing sales rising to US$850.48 million while losses widened, and the company modestly raised full-year revenue guidance to about US$3.33 billion alongside new fourth-quarter guidance of US$875 million to US$878 million.

- This combination of faster top-line growth guidance, ongoing losses, analyst rating changes, and even a shareholder investigation is reshaping how investors think about Zscaler’s AI-focused zero-trust security platform and its risk profile.

- We’ll now examine how Zscaler’s updated revenue outlook and mixed profitability picture affect the earlier investment narrative around zero trust AI security.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe its AI-led zero trust platform can keep winning enterprise security budgets even as big cloud providers and rivals bundle more capabilities. The key near term catalyst is sustained revenue growth from newer AI and data security offerings, while the biggest risk is that continued net losses and widening EPS shortfalls dull confidence in the path to profitability. The latest results and guidance modestly upgrade growth expectations but do not yet change that risk balance in a material way.

The most directly relevant announcement is Zscaler’s decision to lift full year fiscal 2026 revenue guidance to about US$3.33 billion, alongside new fourth quarter guidance of US$875 million to US$878 million. This matters because it reinforces the revenue side of the thesis at the same time that losses increased, sharpening the trade off between investing for AI driven growth and improving margins, which is central to how near term catalysts and risks are now being weighed.

Yet against this stronger top line story, investors should still be aware that widening losses and a fresh shareholder investigation could...

Zscaler's narrative projects $5.2 billion revenue and $152.9 million earnings by 2029. This requires 19.9% yearly revenue growth and a $220.5 million earnings increase from -$67.6 million today.

Uncover how Zscaler's forecasts yield a $227.67 fair value, a 68% upside to its current price.

Exploring Other Perspectives

The most bearish analysts were already assuming revenue growth of about 19.7% a year and no profits within three years, so their focus on high spending and margin strain from aggressive AI investments may look even more cautious after this guidance lift, reminding you that reasonable people can read the same numbers very differently and that it is worth weighing several viewpoints before deciding what this latest quarter really means.

Explore 5 other fair value estimates on Zscaler - why the stock might be worth just $193.79!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Zscaler research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.