DiDi Global (OTCPK:DIDI.Y): Revisiting Valuation After Q2 Results, Lawsuit Reserve, and EV Expansion

DiDi Global’s Bold Moves: Growth, Losses, and a Strategic Crossroads

If you are watching DiDi Global (OTCPK:DIDI.Y), recent headlines likely have you weighing your next steps. The company just reported its second quarter results, with standout year-over-year sales growth set against the backdrop of a net loss. The loss stemmed largely from a hefty legal reserve as DiDi aims to resolve a lawsuit linked to its 2021 IPO. This adds a complex layer to an already dynamic story.

Even with ongoing legal and profitability challenges, DiDi’s share price has climbed an impressive 78% over the past year, with momentum accelerating in recent months. Much of this optimism seems to be fueled by tangible progress in electric vehicle initiatives, fresh partnerships, and efforts to expand into European and US markets. While excitement about the future is building, the market’s valuation of DiDi remains careful. Shares trade at a price-to-sales ratio below many of its peers, reflecting skepticism about how soon profitability will materialize.

After such a dramatic run and mixed signals on profitability, the key question for investors is whether DiDi is truly undervalued now, or if the market is already pricing in most of its growth story.

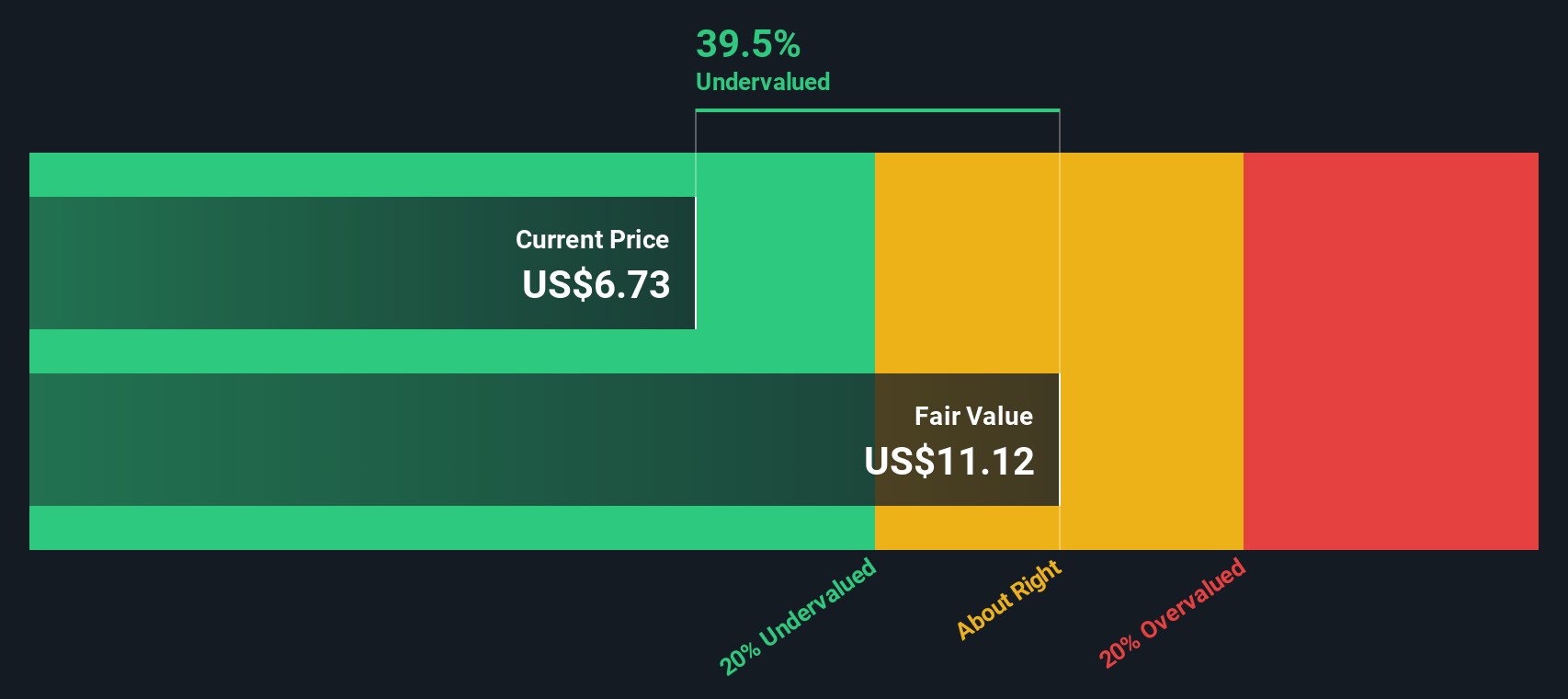

Price-to-Sales of 1.1x: Is it justified?

Based on the Price-to-Sales (P/S) ratio, DiDi Global is trading at a meaningful discount to both industry averages and peer companies. The P/S is a metric that compares a company's current stock price to its revenues, providing a relatively straightforward measure of valuation, especially for businesses that are not yet consistently profitable like DiDi.

For the US Transportation industry, a typical P/S ratio sits around 1.2x, with DiDi currently at 1.1x. More notably, DiDi trades well below the peer average P/S of 3.5x, and also at a 39.4% discount to certain fair value estimates. This suggests the market remains skeptical about DiDi’s near-term profitability despite healthy top-line growth and improving loss reduction.

The implication? Investors may be underestimating DiDi’s recovery prospects, or the risks of its unproven profit trajectory are still commanding a discount. As earnings momentum builds, this valuation gap could narrow if the company delivers on its financial promises.

Result: Fair Value of $11.46 (UNDERVALUED)

See our latest analysis for DiDi Global.However, regulatory uncertainties and intense competition in ride-hailing could quickly challenge DiDi’s path to profitability if market dynamics shift unexpectedly.

Find out about the key risks to this DiDi Global narrative.Another View: Discounted Cash Flow Perspective

Taking a look through the lens of our DCF model offers another way to view DiDi’s value. This method also points to the shares trading below estimated fair value. Is that enough to sway investors on the fence?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own DiDi Global Narrative

If you want to take a different perspective or dive deeper into the numbers yourself, you can quickly craft your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding DiDi Global.

Looking for More Winning Investment Ideas?

Don’t let opportunities pass you by. There’s a universe of fast-moving companies beyond DiDi. Use these powerful tools to focus your search and get ahead now:

- Spot cash-flow bargains with real upside by starting your hunt for undervalued stocks based on cash flows making waves in the market.

- Uncover small-cap standouts destined for growth when you track penny stocks with strong financials built on solid financials.

- Tap into the world’s most disruptive tech trends by following quantum computing stocks set to transform industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.