Discovering US Undiscovered Gems in July 2025

EVI Industries, Inc. EVI | 0.00 |

As the U.S. market navigates a landscape marked by cautious optimism surrounding corporate earnings and economic growth, investors are keenly watching the Federal Reserve's interest rate decisions and their potential impact on small-cap stocks. In this environment, identifying promising opportunities often involves seeking out companies that demonstrate resilience and innovation amidst broader market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 73.89% | 1.93% | -1.42% | ★★★★★★ |

| Southern Michigan Bancorp | 117.38% | 8.87% | 4.89% | ★★★★★★ |

| Affinity Bancshares | 43.51% | 4.54% | 8.05% | ★★★★★★ |

| FineMark Holdings | 115.14% | 2.22% | -28.34% | ★★★★★★ |

| FRMO | 0.09% | 44.64% | 49.91% | ★★★★★☆ |

| Valhi | 43.01% | 1.55% | -2.64% | ★★★★★☆ |

| Pure Cycle | 5.02% | 4.35% | -2.25% | ★★★★★☆ |

| Gulf Island Fabrication | 19.65% | -2.17% | 42.26% | ★★★★★☆ |

| Solesence | 82.42% | 23.41% | -1.04% | ★★★★☆☆ |

| Linkhome Holdings | 1.64% | 391.96% | 428.09% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

G. Willi-Food International (WILC)

Simply Wall St Value Rating: ★★★★★★

Overview: G. Willi-Food International Ltd. is a company that designs, imports, markets, and distributes food products globally under the Willi-Food and Euro European Dairies brand names, with a market cap of $297.36 million.

Operations: WILC generates revenue primarily from the import-export, marketing, and distribution of food products, amounting to ₪584.60 million. The company's financial performance is highlighted by its net profit margin trends over recent periods.

G. Willi-Food International, a nimble player in the consumer retailing sector, boasts an impressive earnings growth of 81% over the past year, outpacing the industry average of 7.4%. With no debt on its books, interest coverage isn't a concern for this company. Its price-to-earnings ratio stands at 14.2x, presenting a more attractive valuation compared to the broader US market's 18.6x. Despite not being free cash flow positive recently, its high level of non-cash earnings underscores robust operational efficiency and profitability potential in a competitive landscape.

Central Securities (CET)

Simply Wall St Value Rating: ★★★★★★

Overview: Central Securities Corp. is a publicly owned investment manager with a market capitalization of $1.40 billion.

Operations: Central Securities generates revenue primarily from its financial services segment, specifically closed-end funds, amounting to $23.70 million.

Central Securities, a smaller player in the financial sector, has shown impressive earnings growth of 28.8% over the past year, outpacing the Capital Markets industry average of 14.5%. This growth is bolstered by a substantial one-off gain of US$272.5M that impacted recent financial results. Trading at nearly half its estimated fair value, it seems undervalued to some analysts. The company remains debt-free for five years now and enjoys positive free cash flow, which could suggest robust operational health and potential resilience against market fluctuations. Recent dividend increases further highlight its shareholder-friendly approach with a US$0.25 per share payout announced for June 2025.

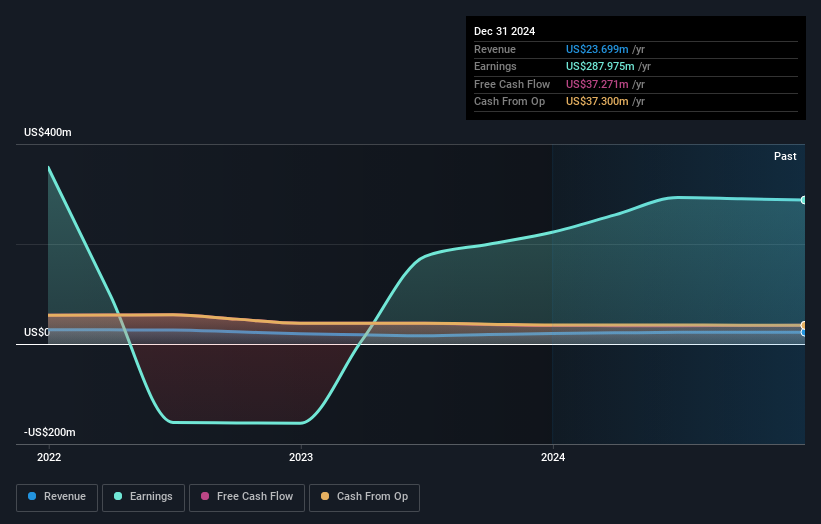

EVI Industries (EVI)

Simply Wall St Value Rating: ★★★★★★

Overview: EVI Industries, Inc. operates through its subsidiaries to distribute, sell, rent, and lease commercial and industrial laundry and dry-cleaning equipment across the United States, Canada, the Caribbean, and Latin America with a market cap of $298.30 million.

Operations: EVI generates revenue primarily from the wholesale distribution of machinery and industrial equipment, totaling $370.02 million.

EVI Industries, a nimble player in the trade distributors sector, is making strategic moves with acquisitions and digital integration to broaden its market reach. Recent earnings growth of 34.5% outpaced the industry average of -0.9%, showcasing its competitive edge. The company reports a satisfactory net debt to equity ratio at 12.9%, reflecting prudent financial management over five years as it reduced from 34.1% to 17.1%. Despite being dropped from several Russell indices recently, EVI's EBIT covers interest payments by 6.2 times, indicating robust financial health amidst ambitious expansion plans in healthcare and hospitality sectors.

Summing It All Up

- Take a closer look at our US Undiscovered Gems With Strong Fundamentals list of 293 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.