Dividend Move And Capital Return Focus Might Change The Case For Investing In Huntington Bancshares (HBAN)

Huntington Bancshares Incorporated HBAN | 0.00 |

- Huntington Bancshares Incorporated previously announced that its Board of Directors declared and set aside a quarterly cash dividend on its 5.70% Series I Non-Cumulative Perpetual Preferred Stock (Nasdaq: HBANM) of US$356.25 per share (equivalent to US$0.35625 per depositary share), payable on September 1, 2026, to shareholders of record on August 15, 2026.

- Alongside this, fresh analyst coverage emphasizing improving operating leverage and expectations for stronger capital returns has spotlighted how management is seeking to balance income to preferred holders with broader capital allocation priorities.

- Next, we’ll examine how the focus on improved operating leverage and capital returns may reshape Huntington Bancshares’ investment narrative.

Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you need to be comfortable with a regional bank that is actively expanding, while still heavily tied to its core Midwest footprint and interest rate dynamics. The latest preferred dividend and renewed analyst coverage support an orderly capital return story, but do not materially change the near term focus on executing the Veritex expansion and managing the risk of margin pressure from funding costs and interest rate volatility.

The newly declared quarterly dividend on the 5.70% Series I preferred stock fits into a longer history of regular preferred payouts, underlining how Huntington is funding income for preferred holders alongside common equity capital needs. For investors watching operating leverage as a key catalyst, this consistency in preferred distributions sits in the background while attention remains on how earnings and efficiency trends evolve through the Texas and Carolinas build out.

Yet alongside these potential benefits, investors should be aware that margin compression risk could still...

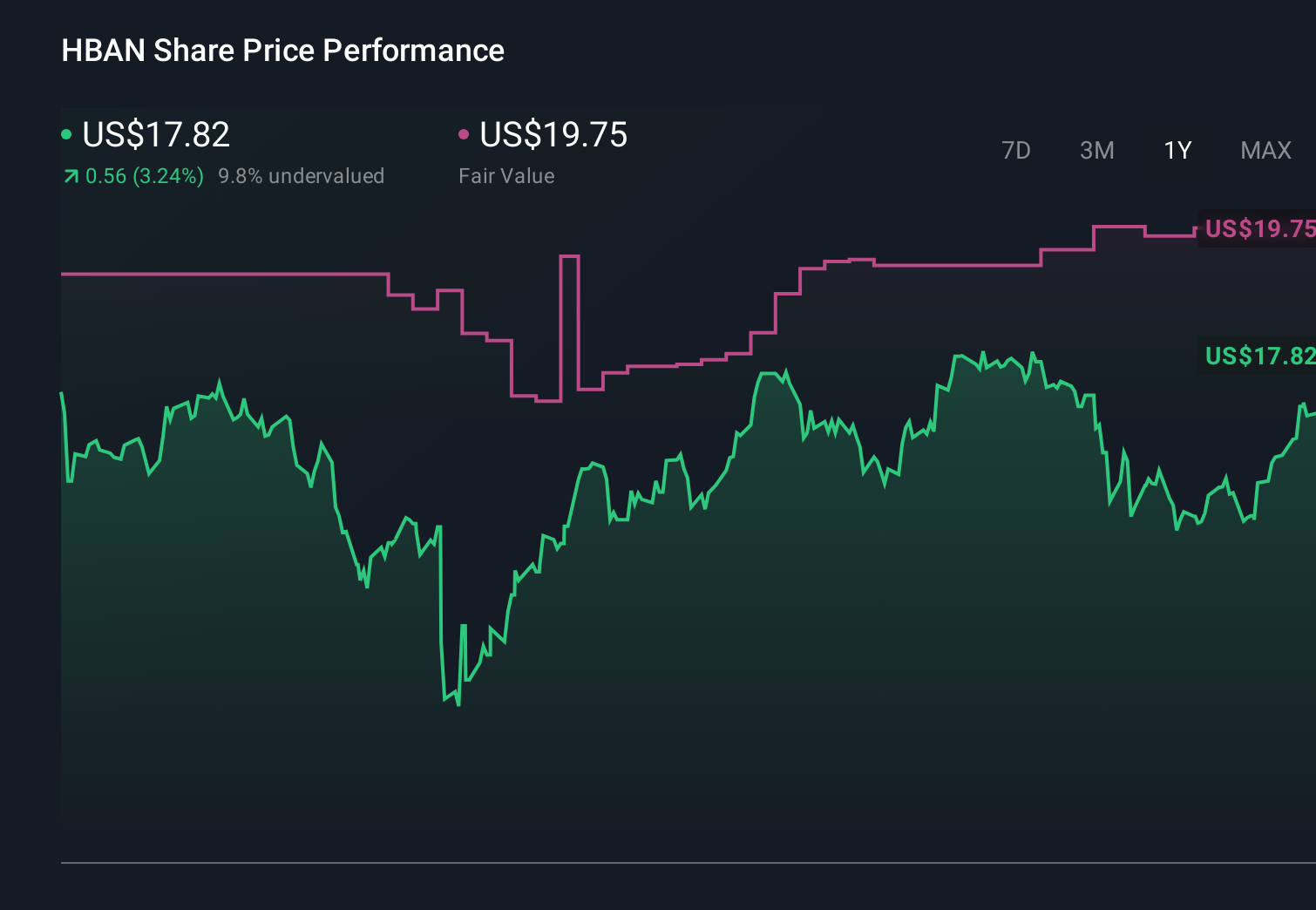

Huntington Bancshares' narrative projects $14.5 billion revenue and $3.7 billion earnings by 2029. This requires 20.3% yearly revenue growth and about a $1.6 billion earnings increase from $2.1 billion today.

Uncover how Huntington Bancshares' forecasts yield a $19.84 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently estimate Huntington’s fair value between US$19.84 and US$33.51, reflecting a wide spread of individual views. When you set those against the emphasis on improved operating leverage and capital returns, it underlines how differently investors can weigh expansion benefits versus interest rate and margin risks, and why comparing several viewpoints can help frame your own expectations.

Explore 3 other fair value estimates on Huntington Bancshares - why the stock might be worth just $19.84!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.