Do Analyst Downgrades And Weaker Coal Outlook Change The Bull Case For Warrior Met Coal (HCC)?

Warrior Met Coal, Inc. HCC | 92.69 | -2.01% |

- In recent days, analyst downgrades for Warrior Met Coal have cut consensus earnings estimates for 2026 and 2027, reflecting mounting concerns about weaker demand for coal amid the global shift toward cleaner energy and tightening environmental regulations.

- This reassessment of Warrior Met Coal’s earnings outlook, coupled with a bearish industry stance from Zacks Equity Research, highlights how sector-wide decarbonization pressures may be reshaping expectations for the company’s long-term role in steelmaking supply chains.

- Now, we'll examine how sharply reduced earnings estimates and a weaker coal outlook may alter Warrior Met Coal's previously balanced investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal today, you have to believe that metallurgical coal will remain essential to steelmaking long enough for the Blue Creek expansion and new U.S. tax credits to matter, even as decarbonization and recycling gain ground. The recent 2026 and 2027 earnings estimate cuts and Zacks’ Strong Sell rating directly challenge that view in the near term, making demand uncertainty the key catalyst and regulatory and decarbonization pressure the most immediate risk.

Against this weaker industry backdrop, the early, under budget completion of the Blue Creek mine and its contribution of 1.3 million tons in Q4 2025 stand out. This project underpins Warrior’s 2026 production guidance of 12.0 to 13.0 million short tons, but the fresh estimate cuts raise harder questions about how quickly those new tons can be placed at attractive prices if coal demand continues to soften.

Yet beneath this expansion story, investors should be aware that...

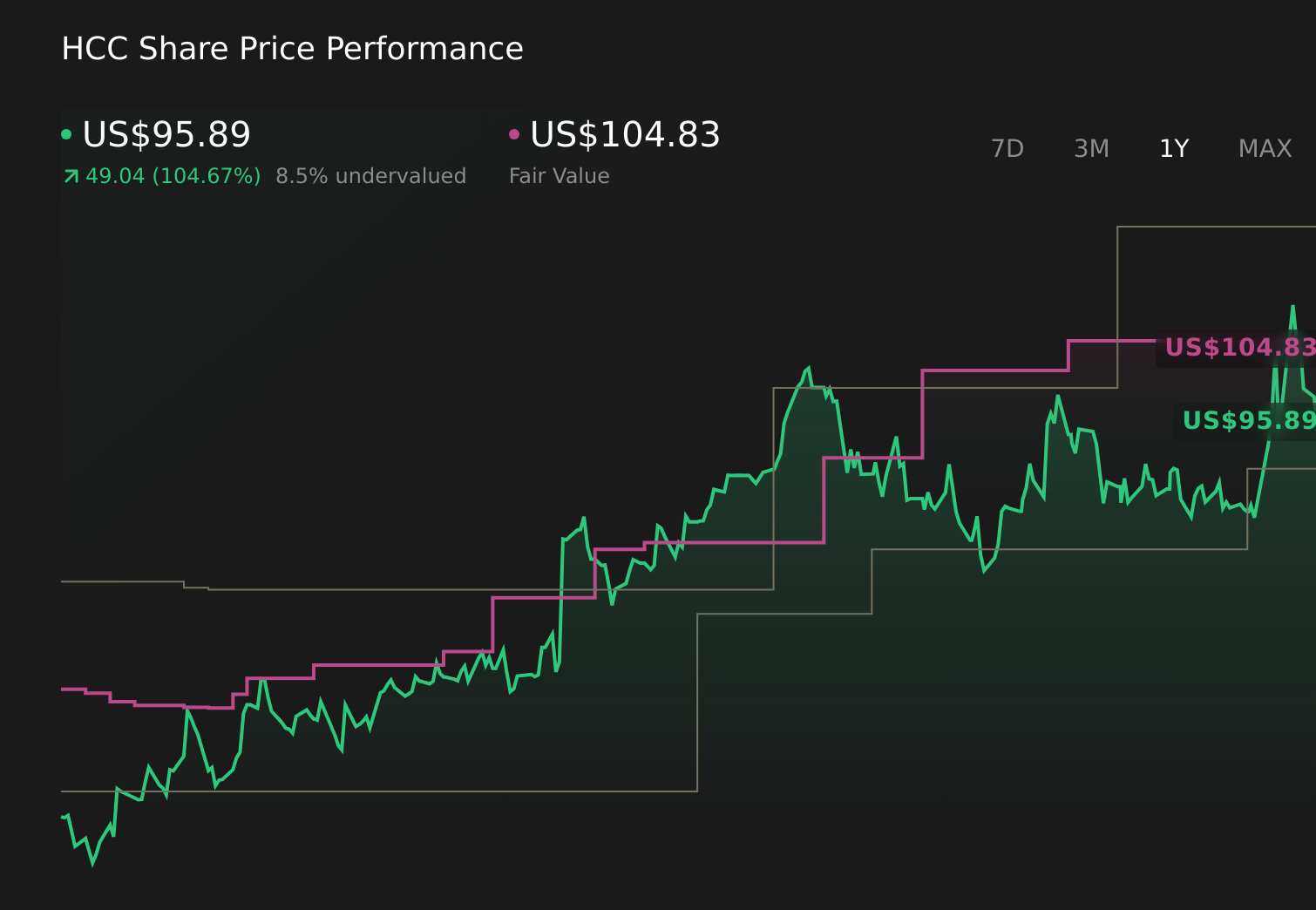

Warrior Met Coal's narrative projects $2.3 billion revenue and $481.3 million earnings by 2029.

Uncover how Warrior Met Coal's forecasts yield a $105.83 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Before this downgrade, the most pessimistic analysts were already assuming Warrior would need US$1.9 billion in revenue and US$264.0 million in earnings by 2028, so you should expect that both their cautious view and the more constructive case built around Blue Creek’s ramp up could shift meaningfully as the new coal demand signals sink in.

Explore 3 other fair value estimates on Warrior Met Coal - why the stock might be worth as much as 12% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.