Do Cava’s Insider Sales and Volatile Earnings Bets Reframe Its Growth Story for Investors (CAVA)?

CAVA Group, Inc. CAVA | 0.00 |

- Cava Group recently saw increased attention ahead of its past May 19 earnings release, with analysts projecting higher revenue but lower year-over-year earnings per share alongside brisk options trading that pointed to a potentially sharp post-report price move.

- Insider share sales tied to vested restricted stock units and rising analyst earnings estimates highlighted how tax-driven transactions and shifting expectations can both influence how investors interpret the company’s growth and profitability outlook.

- Against this backdrop of heightened options-implied volatility, we’ll examine how the anticipated earnings reaction may reshape Cava’s growth-focused investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 33 companies in the world exploring or producing it. Find the list for free.

CAVA Group Investment Narrative Recap

To own CAVA, you need to believe its fast casual Mediterranean concept, expansion plan toward 1,000 restaurants, and tech investment can offset margin pressure, rising costs, and menu fatigue risk. The immediate catalyst is the May 19 earnings release and any update to growth and margin guidance, while the biggest near term risk is that aggressive expansion and higher costs weigh on already pressured earnings; this latest pre earnings volatility does not materially change that setup.

The most relevant development is the options market implying roughly a 12 percent swing around earnings, with recent history showing actual moves often outpacing expectations. Coupled with tax driven insider sales of vested RSUs and higher analyst earnings estimates, this raises the stakes around same restaurant sales trends and any commentary on margins, making the coming report a key test of whether CAVA’s growth story still justifies its elevated valuation.

Yet alongside this growth story, investors should be aware of how a weak operating margin combined with rapid expansion could...

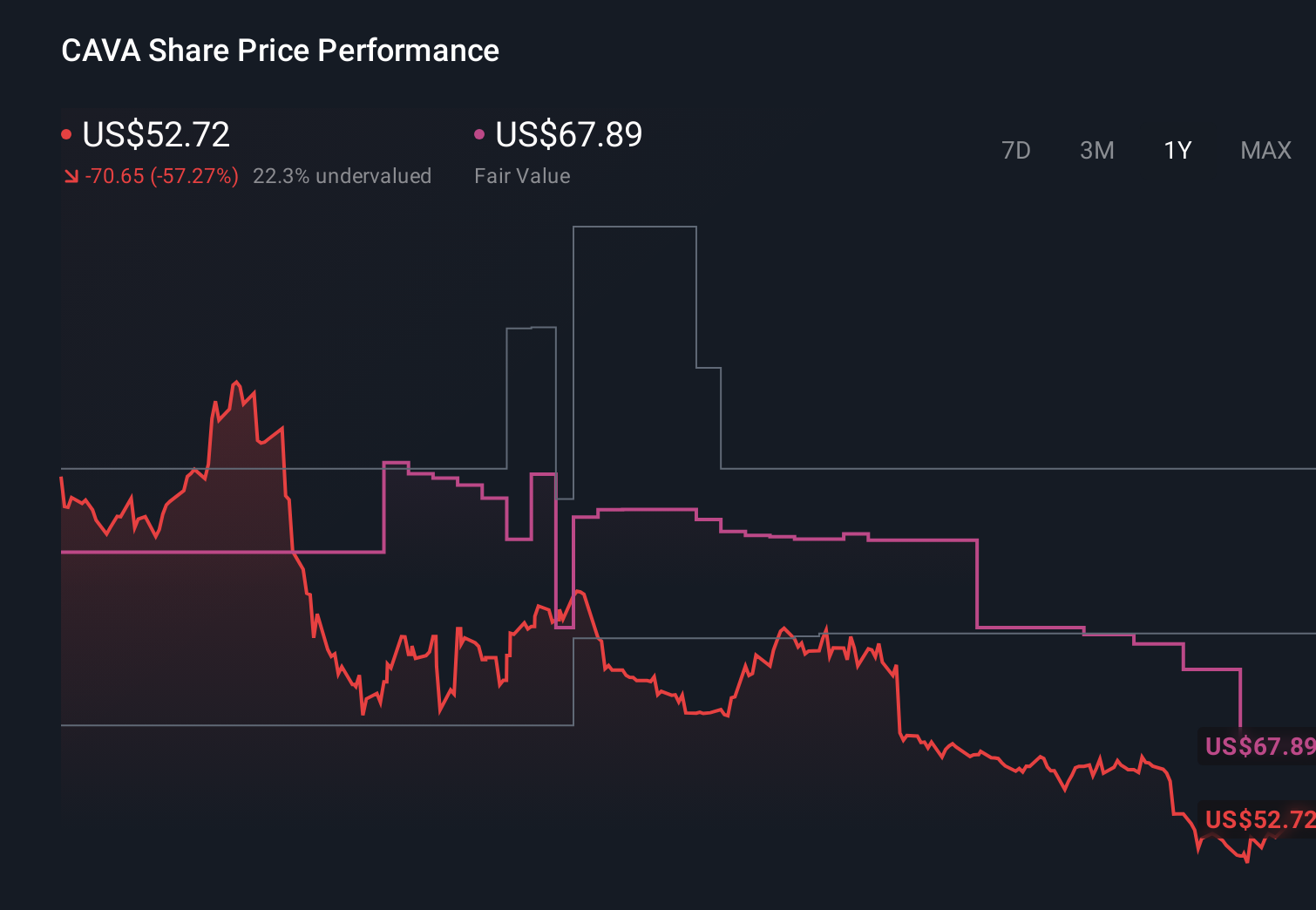

CAVA Group's narrative projects $2.1 billion revenue and $122.3 million earnings by 2029. This requires 21.8% yearly revenue growth and a $58.6 million earnings increase from $63.7 million today.

Uncover how CAVA Group's forecasts yield a $87.27 fair value, a 21% upside to its current price.

Exploring Other Perspectives

The most cautious analysts already assumed CAVA would need about US$2.1 billion of revenue and roughly US$120.7 million of earnings by 2029, so if same restaurant sales or margins disappoint, their concerns about traffic and cost pressures could gain traction and you may see those more pessimistic views revisited after this earnings release.

Explore 8 other fair value estimates on CAVA Group - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.