Do Empire State Realty Trust's New NYC Leases and Buybacks Reshape ESRT's Core Investment Story?

Empire State Realty Trust, Inc. Class A ESRT | 0.00 |

- Empire State Realty Trust reported fourth-quarter 2025 results with higher revenue and net income, renewed and expanded major Manhattan leases with tenants including Burlington, TJ Maxx, JP Morgan Chase, and Nespresso, and completed a US$6,000,000 share repurchase program that retired 891,530 shares.

- In February 2026, the company reinforced its income profile with first-quarter 2026 common and preferred dividends and highlighted a fully New York City-focused portfolio and award-winning health and sustainability credentials across 100% of its properties.

- With these lease renewals and expansions underpinning occupancy, we’ll examine how this leasing momentum affects Empire State Realty Trust’s investment narrative.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

Empire State Realty Trust Investment Narrative Recap

To own Empire State Realty Trust, you need to be comfortable with a fully New York City focused REIT that leans on high quality office, retail, multifamily, and the Empire State Building Observatory for income. The key near term catalyst is whether strong leasing can support occupancy and cash flow, while the biggest current risk remains pressure on earnings from higher operating costs and a still recovering Observatory segment. The latest results and leasing wins do not remove these risks.

The recent long term lease renewals and expansion with Burlington, TJ Maxx, JP Morgan Chase, and Nespresso are especially relevant here, because they directly support occupancy in flagship Midtown assets and reinforce ESRT’s pitch as a modern, amenity rich landlord. At the same time, the continued US$0.035 quarterly common dividend and preferred payouts show management keeping income distributions in place while balancing buybacks and reinvestment against those same cost and Observatory pressures.

But against this progress, investors should be aware that sustained tourism softness and rising expenses could still pressure margins and Observatory earnings...

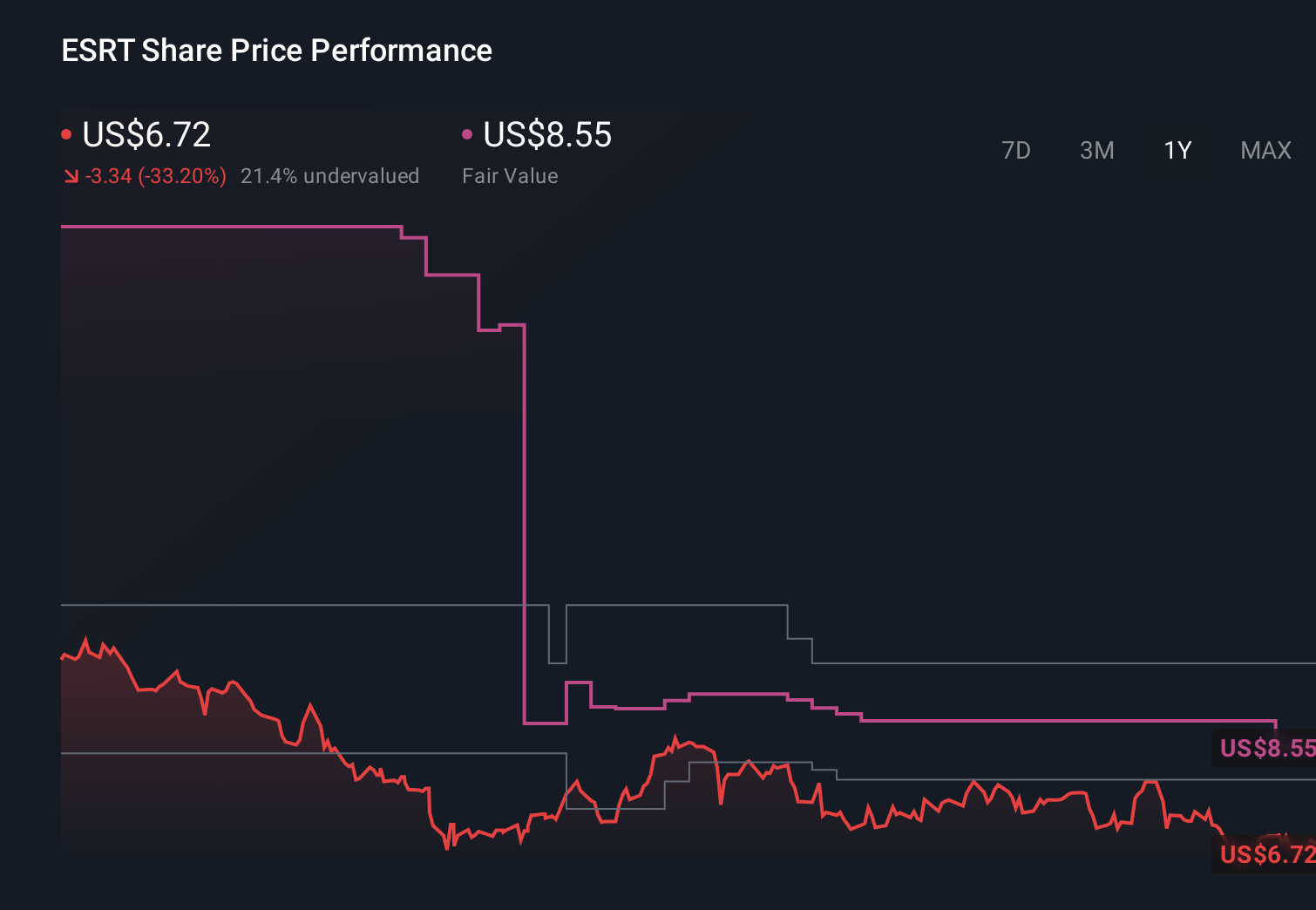

Empire State Realty Trust's narrative projects $797.6 million revenue and $13.7 million earnings by 2028.

Uncover how Empire State Realty Trust's forecasts yield a $7.36 fair value, a 24% upside to its current price.

Exploring Other Perspectives

While recent leasing strength highlights ESRT’s occupancy catalyst, the lowest analysts were the most cautious, assuming revenue growth of about 2.0% and earnings around US$18.8 million, so this new information may lead some of them to reassess how severe that downside really looks.

Explore 2 other fair value estimates on Empire State Realty Trust - why the stock might be worth as much as 24% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Empire State Realty Trust research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Empire State Realty Trust research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Empire State Realty Trust's overall financial health at a glance.

No Opportunity In Empire State Realty Trust?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.