Do Hormuz-Driven Earnings Make Frontline (FRO) More Attractive or More Exposed to Geopolitics?

Frontline Plc FRO | 0.00 |

- Earlier this year, Frontline reported a surge in earnings after Iran’s attempted transit tolls in the Strait of Hormuz lengthened key tanker shipping routes and drove market repricing.

- This episode underlined how sensitive Frontline’s revenues are to shifts in geopolitical risk and trade patterns along critical oil chokepoints.

- Now, we’ll explore how earnings boosted by Hormuz-related route lengthening interact with Frontline’s existing investment narrative and risk profile.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

Frontline Investment Narrative Recap

To own Frontline, you need to believe that tight tanker supply and complex oil trade routes can keep utilization and day rates supportive, even as global decarbonization pressures build. The Hormuz-related route lengthening has clearly boosted recent earnings, but it does not remove the central near term risk: exposure to volatile spot markets if geopolitical disruptions ease or shift elsewhere.

The Q1 2026 results are the clearest link to this Hormuz episode, with revenue of US$929.33m and net income of US$559.12m reflecting the repricing of longer routes. This print also supports Frontline’s recent step up in dividends, including the US$1.55 per share Q1 2026 payout, which ties shareholder returns more directly to swings in geopolitically driven freight markets.

Yet beneath strong recent earnings, investors should be aware of Frontline’s heavy reliance on volatile spot charter rates and how quickly route patterns can change...

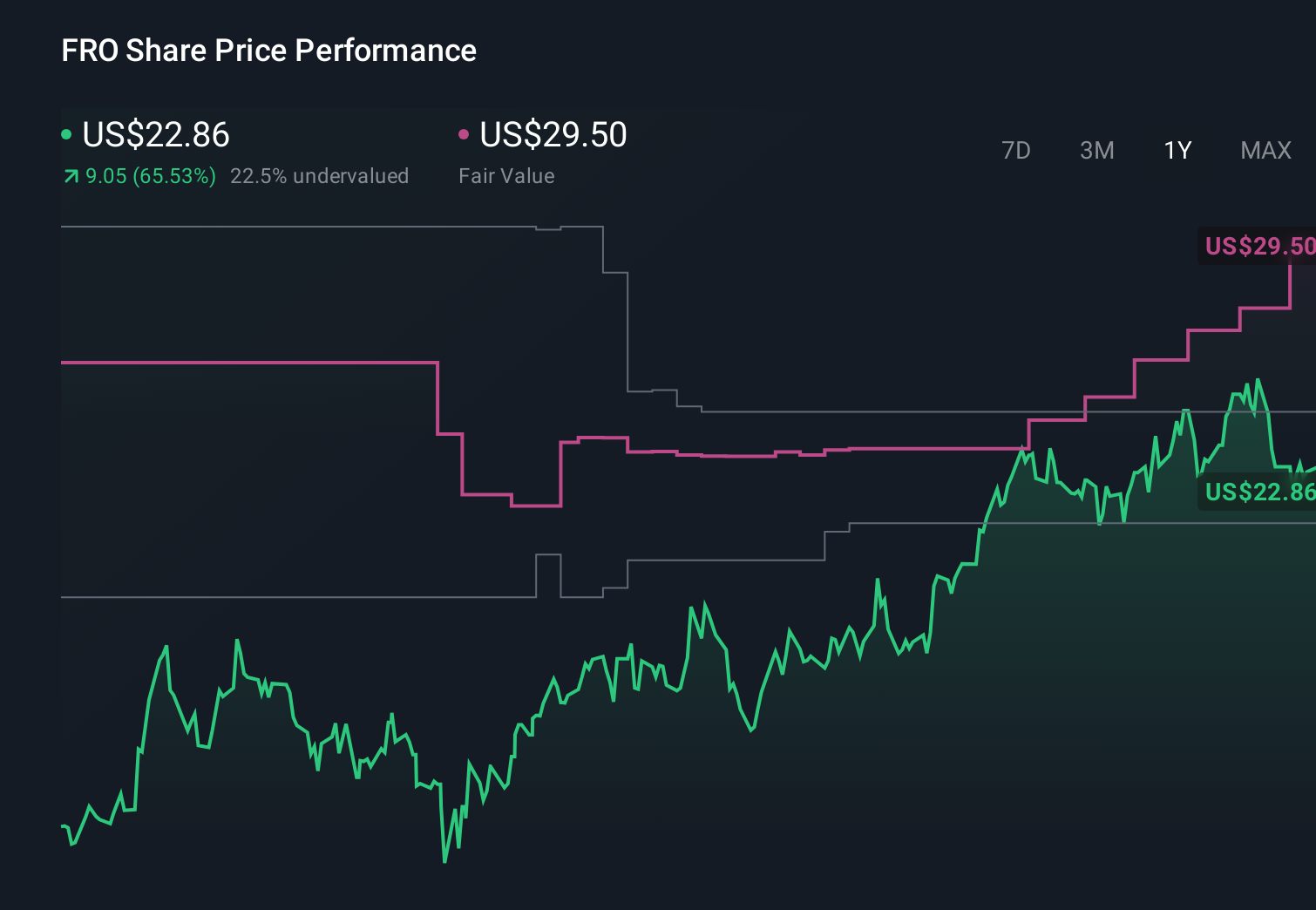

Frontline's narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline but an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 7% upside to its current price.

Exploring Other Perspectives

While consensus focuses on spot market risk, the most optimistic analysts lean into longer trade routes and had penciled in about US$1.4b revenue and US$786.8m earnings, reminding you that views and valuations can shift quickly as the Hormuz situation evolves.

Explore 5 other fair value estimates on Frontline - why the stock might be worth as much as 69% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Frontline research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.