Do Leadership Shifts at Hartford (HIG) Clarify or Complicate Its Underwriting Profitability Narrative?

Hartford Insurance Group, Inc. HIG | 0.00 |

- Hartford Financial Services Group recently confirmed Dave Draper as chief underwriting officer for its UK operations and appointed Bertie Troughton as head of upstream energy, international, after Draper had served as interim CUO and previously led third-party lines.

- These leadership moves come as analysts anticipate a softer second-quarter 2026 earnings result, raising fresh questions about underwriting discipline and profitability amid higher claims and operating costs.

- Next, we will examine how anticipated earnings pressure, driven by rising claims and operating costs, may influence Hartford’s existing investment narrative.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Hartford Insurance Group Investment Narrative Recap

To own Hartford, you need to believe in its core underwriting and capital discipline, even as higher claims and costs pressure near term earnings. The UK underwriting appointments look incremental rather than transformative, so the most immediate catalyst remains the upcoming Q2 2026 results, while the key risk is that rising loss costs and expenses continue to compress margins if pricing and underwriting do not keep pace.

In this context, Hartford’s April 2026 Q1 result, with revenue of US$7,226 million and net income of US$856 million, offers a useful reference point. It shows how the group has recently managed profitability ahead of the anticipated softer Q2 print, helping investors judge whether recent leadership changes in UK specialty and energy underwriting align with the broader effort to sustain margins.

Yet beneath the headline earnings pressure, investors should be aware that rising claims and operating costs could...

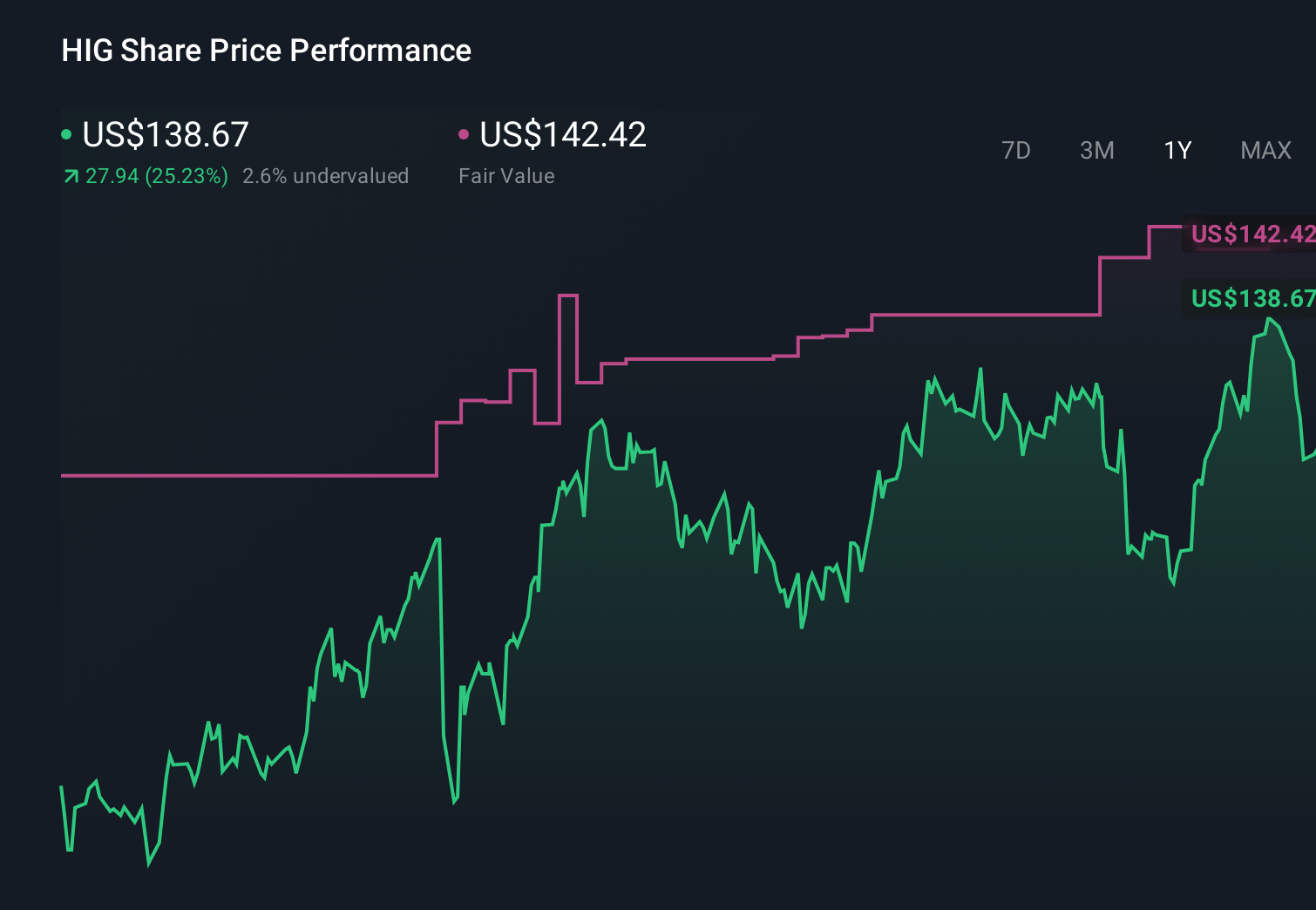

Hartford Insurance Group's narrative projects $31.7 billion revenue and $3.9 billion earnings by 2029. This requires 3.3% yearly revenue growth and a $0.1 billion earnings decrease from $4.0 billion today.

Uncover how Hartford Insurance Group's forecasts yield a $147.65 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$141 to US$320 per share, showing how far apart individual views can be. Against that backdrop, concerns about rising operating and claims costs give you a concrete issue to weigh as you compare these different viewpoints.

Explore 4 other fair value estimates on Hartford Insurance Group - why the stock might be worth just $141.25!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hartford Insurance Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Hartford Insurance Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hartford Insurance Group's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.