Do Moelis’ (MC) Strong Earnings and Neutral Ratings Point To Different Stories On Margins?

Moelis & Co. Class A MC | 0.00 |

- In recent days, Moelis & Company reported strong Q4 earnings and highlighted its strongest coverage platform to date, with management emphasizing momentum and long-term value creation.

- At the same time, several major banks reiterated neutral views on Moelis, revealing a tension between upbeat internal commentary and cautious external assessments.

- Next, we'll examine how upbeat earnings alongside cautious analyst sentiment may influence Moelis' existing investment narrative around growth and margins.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Moelis Investment Narrative Recap

To own Moelis, you need to believe in its advisory-focused model, the buildout of Private Capital Advisory, and its ability to convert a strong coverage platform into sustainable fee income despite deal cyclicality. The latest Q4 beat and upbeat management tone support that thesis, but the cluster of Neutral ratings and reduced price targets suggest that, in the near term, the key catalyst remains consistent deal flow, while the biggest risk is margin pressure if hiring and compensation outpace actual revenue.

The most relevant recent announcement is UBS cutting its Moelis price target from US$74 to US$59 while reiterating a Neutral rating, even as the firm reported strong Q4 2025 earnings and highlighted record coverage strength. This mix of solid reported results and tempered analyst expectations frames how investors might think about Moelis’ growth and margin story, especially with continued investment in PCA and senior hires requiring clear evidence of durable, high quality advisory activity.

Yet behind the upbeat earnings, investors should be aware of the risk that rising compensation and expansion costs could...

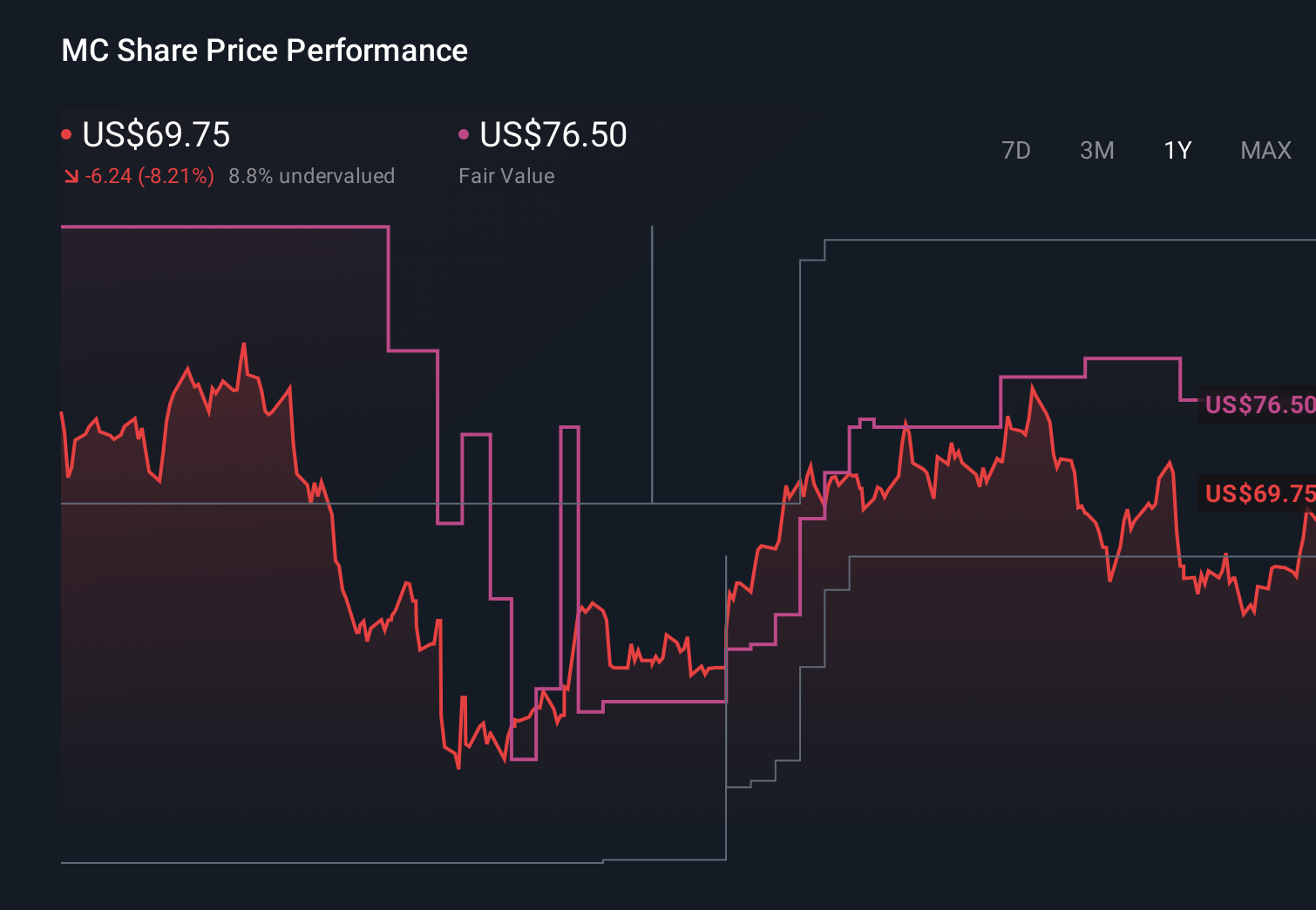

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and about a $183.6 million earnings increase from $198.1 million today.

Uncover how Moelis' forecasts yield a $76.50 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were once modeling Moelis toward about US$2.4 billion of revenue and roughly US$395 million of earnings, which contrasts sharply with concerns about dependence on large, irregular deals and shows how widely your views on risk and reward can differ as fresh earnings and analyst updates come through.

Explore 2 other fair value estimates on Moelis - why the stock might be worth as much as 82% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Moelis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.