Does ADMA Biologics' (ADMA) High Institutional Ownership Reflect Deeper Confidence in Its Biopharma Strategy?

ADMA Biologics, Inc. ADMA | 9.01 9.13 | -1.53% +1.32% Pre |

- Recently, ADMA Biologics received a more favorable valuation grade following a review of its financial standing, underpinned by 17 consecutive quarters of positive results and robust institutional investor confidence at 98.05% ownership.

- This significant show of support among large investors underscores a strong belief in ADMA’s fundamentals and sustained operational momentum within the biopharmaceutical sector.

- With institutional confidence bolstered by clear and consistent financial performance, we'll explore how this development informs ADMA's broader investment narrative.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

ADMA Biologics Investment Narrative Recap

For a shareholder in ADMA Biologics, the core belief centers on confidence in the expansion of plasma-derived therapies, underpinned by visible demand trends in immunodeficiency treatment and an expectation that ADMA’s innovative manufacturing process and robust cash position will allow it to outgrow risks from larger competitors. While the upgraded valuation grade and strong recent financial track record highlight operational health, this development does not alter the primary short-term catalyst, commercial rollout of the new FDA-approved yield enhancement process, nor does it eliminate significant operating risks related to product concentration or supply constraints.

Among ADMA’s recent announcements, the FDA’s April approval of its yield enhancement process stands out as most relevant. This directly supports both the company’s upgraded valuation and the key narrative catalyst: scaling production by over 20 percent to drive gross margin expansion and profit growth, all while addressing some competitive threats from established plasma industry peers.

On the flip side, investors should be aware of ongoing supply chain and plasma collection challenges that...

ADMA Biologics' outlook anticipates $904.6 million in revenue and $350.9 million in earnings by 2028. Achieving this would require 24.0% annual revenue growth and a $142 million increase in earnings from the current level of $208.9 million.

Uncover how ADMA Biologics' forecasts yield a $27.81 fair value, a 83% upside to its current price.

Exploring Other Perspectives

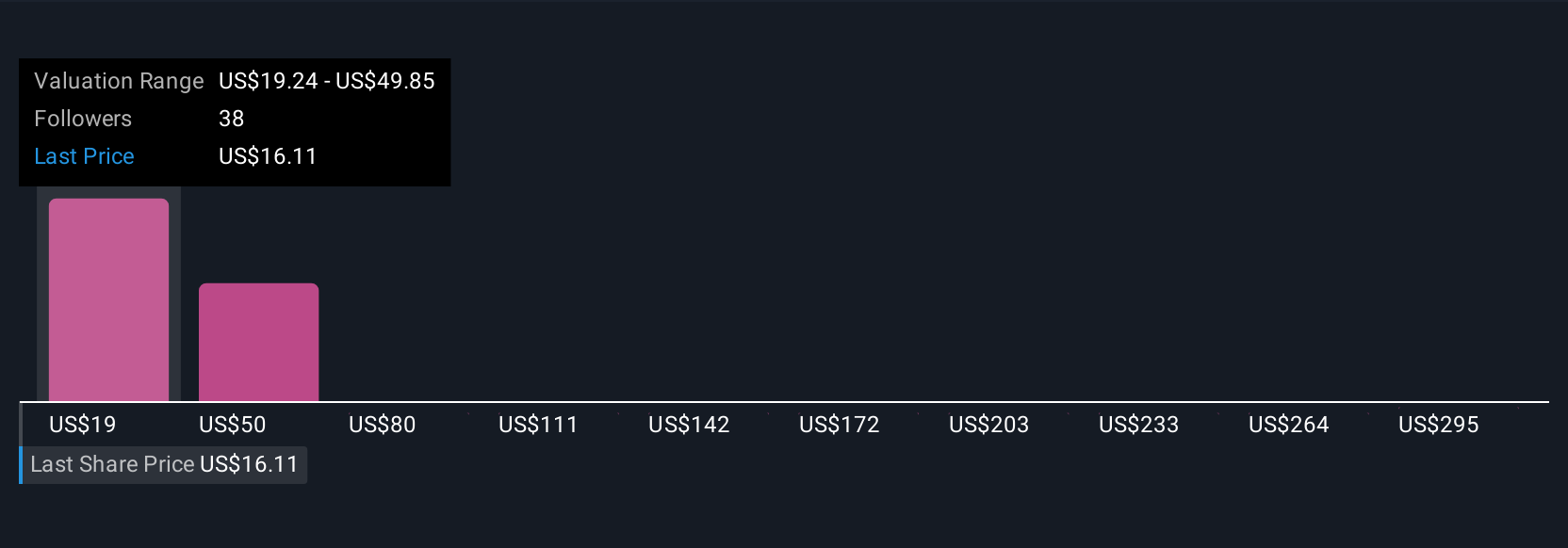

Ten Simply Wall St Community members assigned ADMA fair values ranging from US$19.24 to US$325.32 per share, reflecting diverse expectations. While many expect higher output to drive future earnings, these wide-ranging views highlight the importance of considering multiple scenarios for operational and product risks.

Explore 10 other fair value estimates on ADMA Biologics - why the stock might be a potential multi-bagger!

Build Your Own ADMA Biologics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ADMA Biologics research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ADMA Biologics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ADMA Biologics' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.