Does AES’s Recent Stock Slide Signal an Opportunity for Investors in 2025?

AES Corporation AES | 14.09 14.14 | +0.50% +0.35% Pre |

- Thinking about whether AES is a good buy? You're not alone. If you're searching for value, there are some surprising signals just beneath the surface.

- AES stock has had a turbulent ride, slipping 7.1% over the past week and 7.8% in the last month. However, it's still managed a 3.0% gain year-to-date.

- Recent headlines have focused on changes in the renewable energy landscape and evolving regulatory support, both of which have added fuel to speculation around utility stocks. Developments in U.S. energy policy and global demand for clean power have kept AES in the conversation among transformation-focused investors.

- When it comes to valuation, AES scores a 5 out of 6 based on common methods for finding undervalued stocks. Next, I'll break down how these valuation checks stack up and why the best way to judge value might be even more nuanced than you think.

Approach 1: AES Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This method helps investors determine if a stock is trading below or above its estimated true worth.

For AES, the DCF model uses the 2 Stage Free Cash Flow to Equity approach. The starting point is the company's latest twelve months free cash flow, which was negative at $3.03 billion. Analysts have issued forecasts for the next few years, with projections showing significant improvement, estimating free cash flow to reach $1.38 billion by 2028. Beyond these analyst-covered years, Simply Wall St extrapolates further, expecting continued growth in free cash flows through 2035, though with a more moderate pace each year.

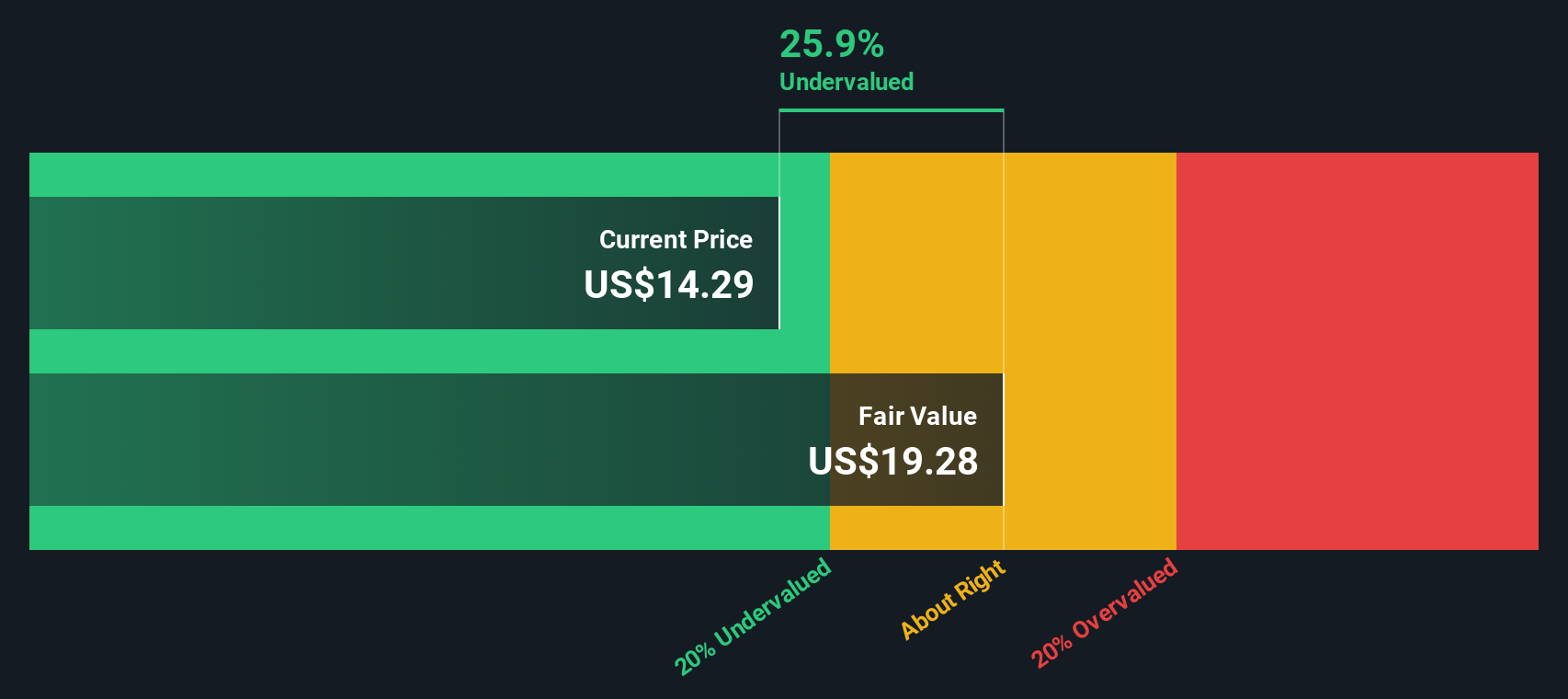

Based on all these projections and the DCF model’s calculations, the estimated intrinsic value of AES shares is $19.28. This result suggests the stock is about 30.3% undervalued compared to its recent market price, indicating a strong margin of safety for potential investors.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AES is undervalued by 30.3%. Track this in your watchlist or portfolio, or discover 843 more undervalued stocks based on cash flows.

Approach 2: AES Price vs Earnings

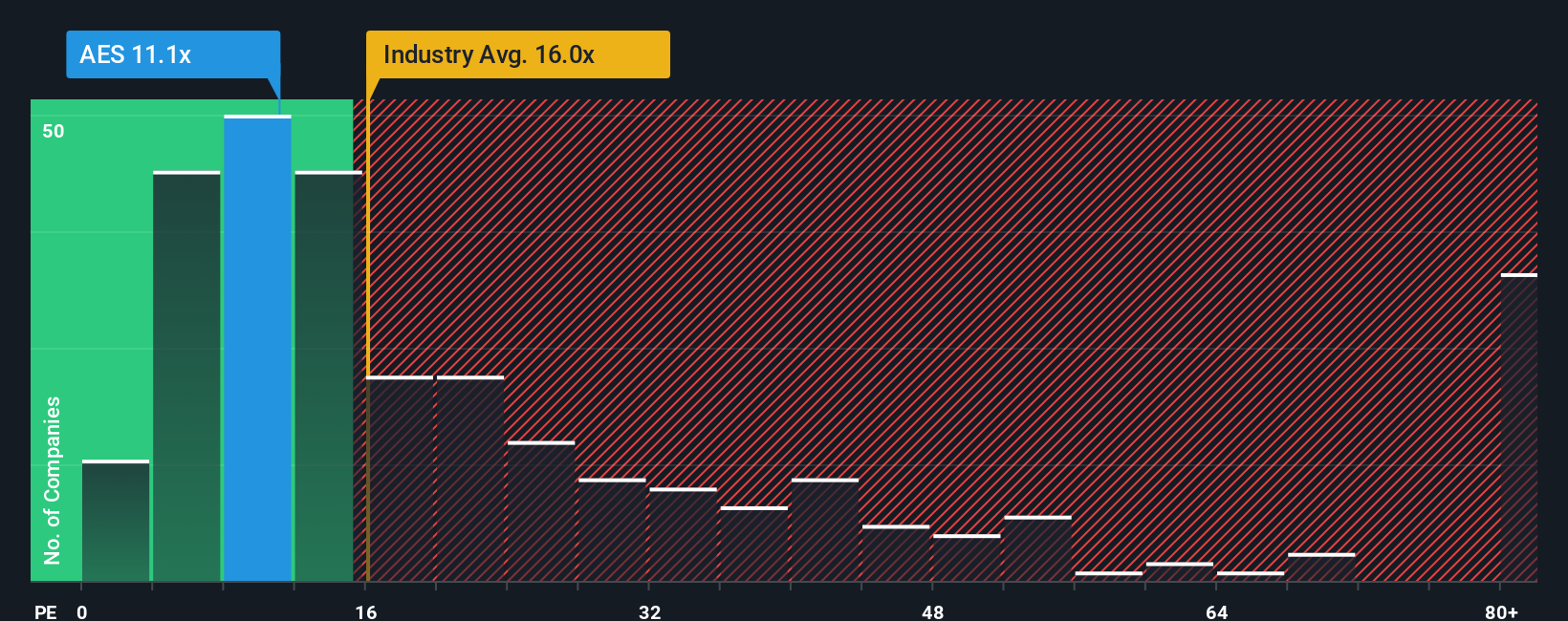

The Price-to-Earnings (PE) ratio is widely used for valuing companies that are consistently profitable, like AES. This metric helps investors understand how much they are paying for each dollar of earnings, which is especially relevant when those earnings are steady and meaningful. Since AES has reported solid profits, using PE offers a straightforward snapshot of its relative value.

What constitutes a "normal" or "fair" PE ratio depends on how investors see a company's future growth prospects and potential risks. Higher growth companies tend to command higher PE ratios, while additional risks or weaker growth prospects usually warrant a lower multiple. For AES, its current PE ratio stands at 10.41x. This is significantly below the Renewable Energy industry average of 17.60x, and well below the average of its major peers at 55.53x.

Simply Wall St also calculates a proprietary "Fair Ratio" for AES, which in this case is 30.81x. This Fair Ratio is designed to be more insightful than a simple industry or peer comparison because it considers AES's unique combination of earnings growth, profit margins, market cap, risk profile, and the industry landscape. By integrating these variables, the Fair Ratio helps clarify whether the current valuation is justified for AES's specific situation rather than relying on averages that might not reflect its realities.

When comparing AES's current PE ratio of 10.41x to its calculated Fair Ratio of 30.81x, the stock looks attractively priced. This suggests it may be undervalued based on its fundamentals and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1409 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AES Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative distills your perspective on a company into a clear story behind the numbers, connecting your own assumptions about AES's future, such as revenue growth, profit margins, and risks, to a fair value calculation that matches your outlook.

By anchoring the company’s story to a financial forecast, Narratives make the connection between what you believe will happen and what the stock is actually worth. They are easy to use and available within the Community page on Simply Wall St, a platform trusted by millions of investors.

Narratives help simplify your buy or sell decisions by directly comparing your calculated Fair Value to the current market Price, and they update automatically when news or results change the investment landscape. For example, some investors are optimistic about AES, targeting a fair value as high as $23, reflecting expectations for strong renewable growth, while others are more cautious, using a fair value as low as $5 due to risks like subsidies and legacy fossil assets. Narratives let each investor quickly sense check, refine, and act on their viewpoint with confidence.

Do you think there's more to the story for AES? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.