Does AI-Fueled Guidance And Nvidia Deal Reshape The Bull Case For Lumentum Holdings (LITE)?

Lumentum Holdings, Inc. LITE | 0.00 |

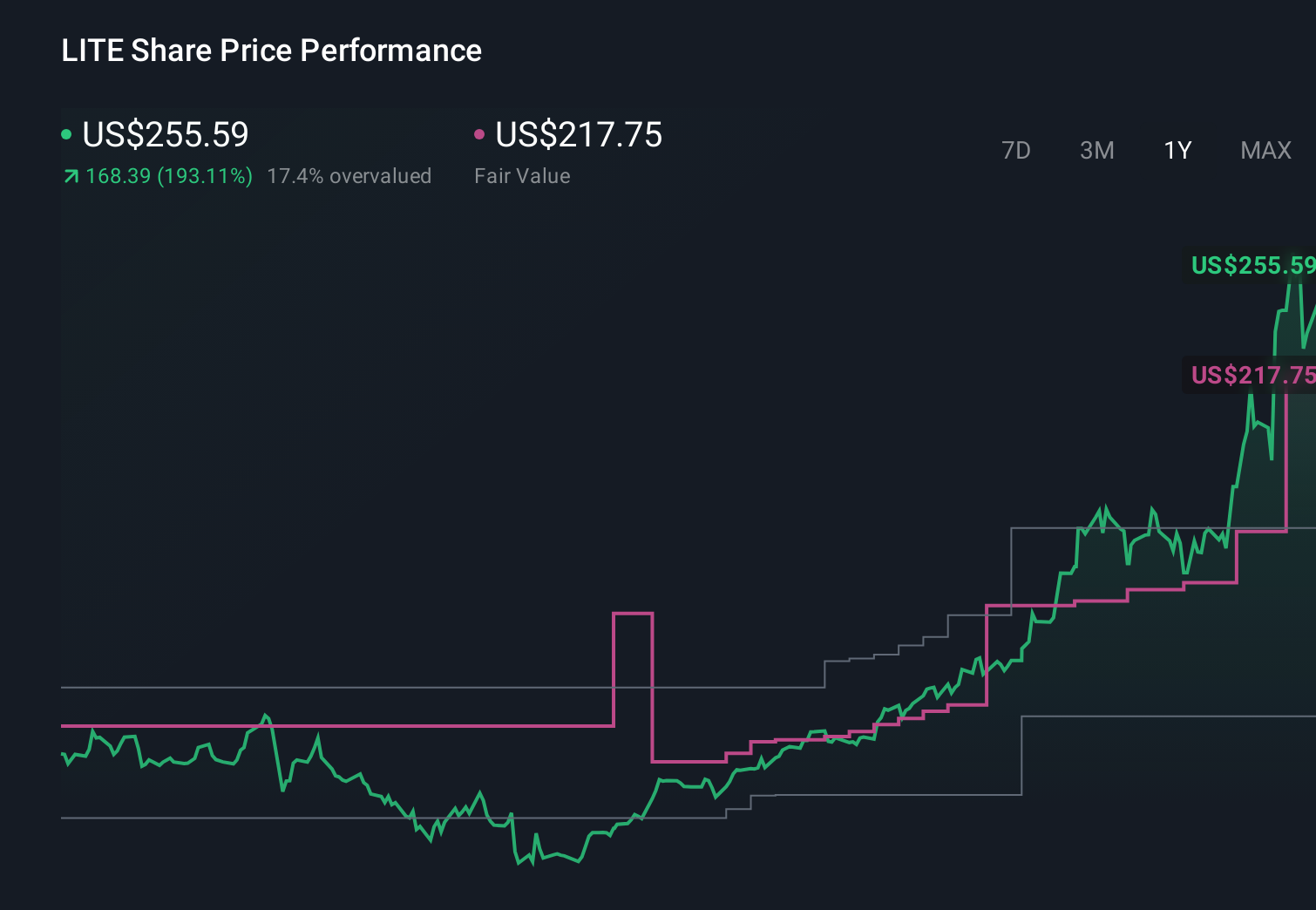

- Lumentum Holdings recently raised its fourth-quarter guidance and reported very large year-over-year revenue growth, citing intense AI-driven demand for its cloud networking and optical components, while also executing a US$650.4 million private exchange of convertible notes for equity to reduce debt.

- At the same time, the company secured a multi-year US$2 billion agreement with Nvidia and is expanding manufacturing capacity, including an indium phosphide fab in North Carolina, highlighting how AI infrastructure build-outs are increasingly tied to specialized optical technology suppliers.

- We’ll now examine how this stronger AI infrastructure demand and raised guidance might reshape Lumentum’s existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

Lumentum Holdings Investment Narrative Recap

To own Lumentum today, you have to believe AI data centers will keep pulling in ever more complex optics and that Lumentum can stay at the center of that spend. The near term catalyst is management’s sharply higher Q4 guidance on the back of AI infrastructure demand, while the biggest risk remains heavy reliance on a small set of hyperscale customers whose orders could swing revenues sharply if priorities or supplier choices change.

The recent US$2 billion multi year agreement with Nvidia goes straight to that catalyst, effectively tying Lumentum’s cloud optics roadmap to one of AI’s largest buyers. It reinforces the raised guidance story and, together with the US$650.4 million convertible note exchange into equity, underlines how the company is aligning its balance sheet and capacity expansion with what it sees as sustained AI optics demand.

Yet alongside this stronger outlook, investors should be aware that customer concentration remains high and any shift in large buyer behavior could...

Lumentum Holdings’ narrative projects $11.7 billion revenue and $4.2 billion earnings by 2029.

Uncover how Lumentum Holdings' forecasts yield a $1105 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 18 percent annual revenue growth and earnings near US$276 million by 2028, which sits well below the AI driven upside many investors now focus on and highlights how views on customer risk and long term demand for Lumentum’s optics can differ widely.

Explore 10 other fair value estimates on Lumentum Holdings - why the stock might be worth over 5x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lumentum Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Lumentum Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lumentum Holdings' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.