Does AI Push and Pricing Probe Reshape GoDaddy’s (GDDY) Recurring-Revenue Investment Story?

GoDaddy, Inc. Class A GDDY | 0.00 |

- Earlier this month, GoDaddy launched Airo for WordPress, an AI-powered experience that helps small businesses and web professionals rapidly build, manage and evolve WordPress sites, while a law firm began investigating whether the company’s promotional pricing strategy for dotcom domains was properly disclosed to investors.

- Together, these developments highlight GoDaddy’s push to embed AI across its ecosystem while raising fresh questions about how its pricing tactics affect revenue visibility and investor confidence.

- Now we’ll examine how the promotional pricing investigation might affect GoDaddy’s investment narrative built around AI-powered offerings and higher-margin recurring revenue.

AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

GoDaddy Investment Narrative Recap

To own GoDaddy, you need to believe its shift from basic domains to AI-enabled, higher-margin, recurring services can offset competition and customer churn. In the near term, the key catalyst is execution on AI products like Airo, while the biggest risk now is how the promotional dotcom pricing and related securities investigation might affect revenue visibility and investor trust. So far, the investigation looks more like a disclosure and expectations issue than a fundamental change to the business model.

The launch of Airo for WordPress is especially relevant here, because it reinforces the core investment argument around AI-powered tools that support the full website lifecycle. If Airo for WordPress gains traction with small businesses and agencies, it could deepen customer relationships and support recurring revenue, which matters even more when pricing choices on core domains are under scrutiny for their impact on short term bookings and reported growth.

But despite these AI opportunities, investors should be aware that questions around promotional pricing disclosure could still...

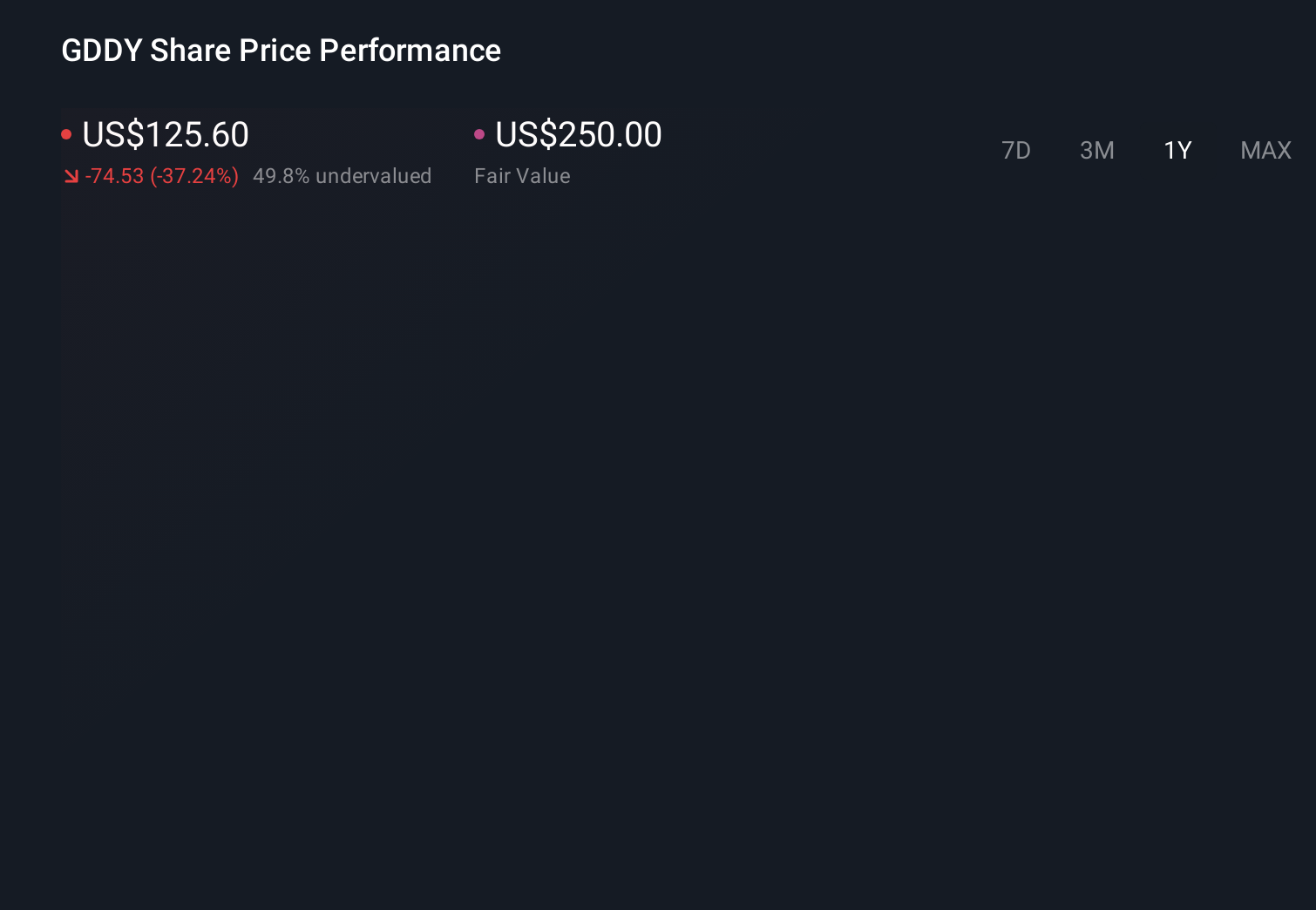

GoDaddy's narrative projects $5.9 billion revenue and $1.3 billion earnings by 2028. This requires 7.7% yearly revenue growth and an earnings increase of about $0.5 billion from $808.5 million.

Uncover how GoDaddy's forecasts yield a $119.43 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the most pessimistic analysts were already assuming only about US$5.8 billion in 2029 revenue and US$1.3 billion in earnings, so this pricing investigation and AI competition could easily lead them to sharpen concerns about early stage product risk and recurring revenue pressure.

Explore 4 other fair value estimates on GoDaddy - why the stock might be worth just $99.99!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your GoDaddy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free GoDaddy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GoDaddy's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.