Does Airbnb Offer Value After International Expansion Push and Recent Price Drop?

Airbnb, Inc. ABNB | 126.28 127.16 | +2.58% +0.70% Pre |

- Ever wondered if now is the right time to jump into Airbnb or if the stock is truly offering value that justifies the buzz around it?

- While Airbnb’s shares are down 3.1% over the past week and 6.8% since the year began, they have still managed to climb a substantial 27.9% over the last three years.

- Recently, headlines have focused on Airbnb’s push to expand in international markets, along with regulatory updates and partnerships that could reshape future growth. These developments are affecting sentiment and may help explain the tug-of-war seen in the stock price in recent weeks.

- Currently, Airbnb scores a 4 out of 6 on our value checks, which means it is considered undervalued by several key measures. Let’s break down how different valuation models approach Airbnb’s worth, and later on, I will share an even more insightful way to look at value that most investors miss.

Approach 1: Airbnb Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and then discounting them back to today’s dollars. This approach seeks to answer what Airbnb is truly worth right now, based on expectations for its business over the next decade and beyond.

Airbnb’s current Free Cash Flow stands at $4.31 billion. Analysts forecast annual growth, projecting cash flows to reach about $6.76 billion by 2029. Notably, analyst estimates only go out five years, so figures beyond that are projected by Simply Wall St. These long-term projections suggest Airbnb’s cash flows could rise to over $9 billion by 2035 if current trends continue.

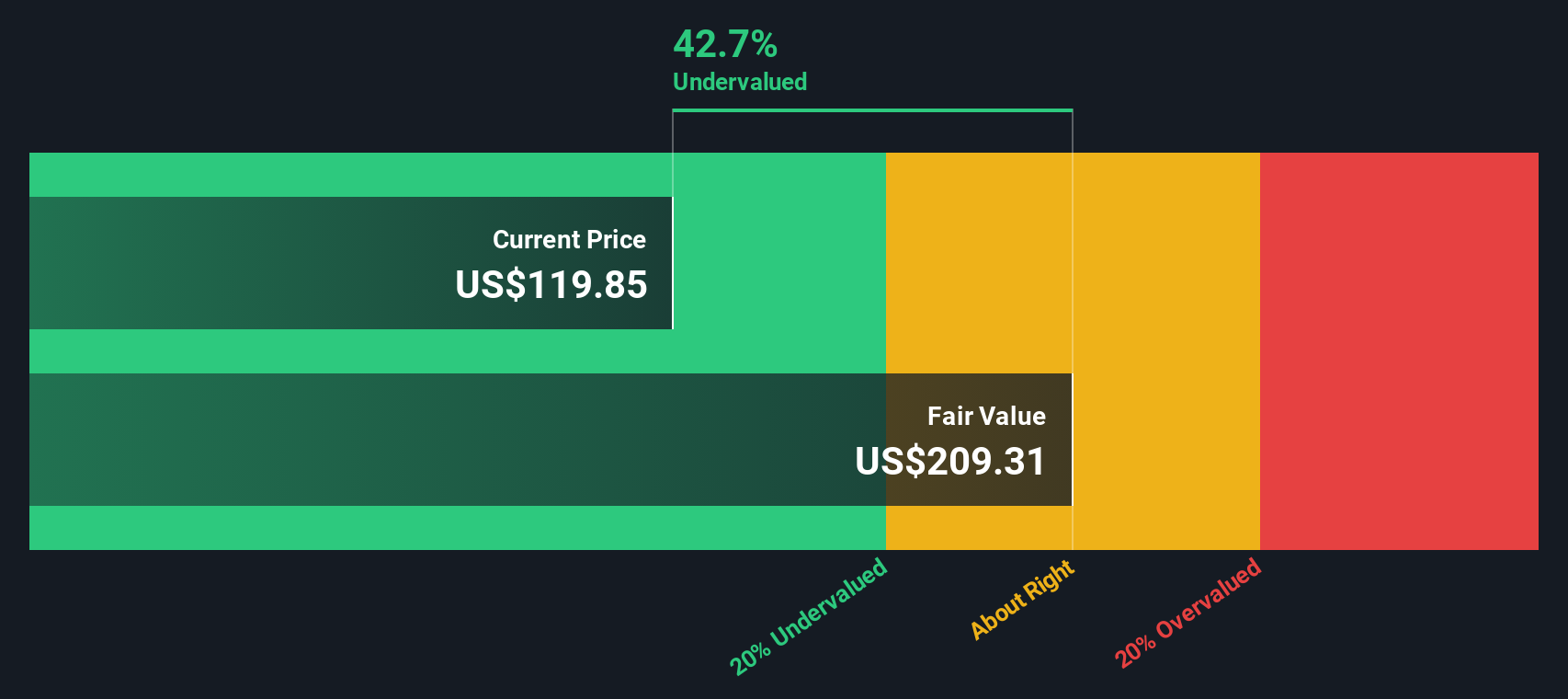

According to the DCF analysis using the 2 Stage Free Cash Flow to Equity model, Airbnb’s intrinsic value per share is estimated at $218.39. This implies the stock is trading at a 43.9 percent discount to its calculated fair value, meaning it appears significantly undervalued compared to its fundamentals right now.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Airbnb is undervalued by 43.9%. Track this in your watchlist or portfolio, or discover 849 more undervalued stocks based on cash flows.

Approach 2: Airbnb Price vs Earnings (PE)

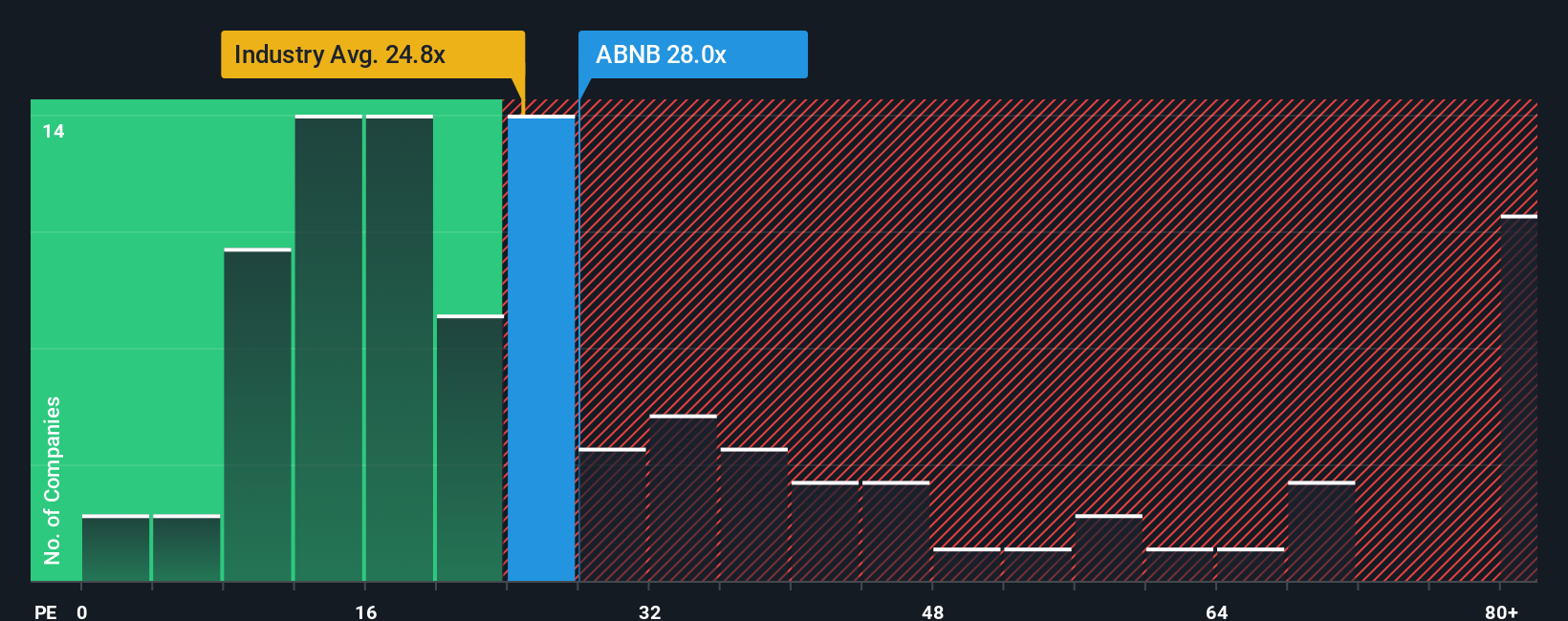

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Airbnb. It shows how much investors are willing to pay per dollar of earnings, making it especially useful for comparing companies that generate meaningful profits and are expected to grow those profits over time.

A fair or “normal” PE ratio will often vary depending on a company’s expected earnings growth, stability, risk profile, and broader industry trends. Companies with faster growth prospects and lower risk typically command higher PE multiples, while those facing uncertainty or slower growth tend to have lower ratios.

Currently, Airbnb is trading at a PE ratio of 28.6x. This sits almost exactly in line with its peer average of 28.7x and is notably higher than the hospitality industry average of 23.7x. However, Simply Wall St’s proprietary Fair Ratio for Airbnb is 29.3x, which factors in not just peer and industry multiples but also Airbnb’s own growth outlook, risk, profitability, and market cap. This Fair Ratio offers a more tailored and accurate benchmark than simple comparisons because it adjusts for the company’s unique strengths and risks rather than just relying on a basic industry snapshot.

Comparing Airbnb’s actual PE of 28.6x to its Fair Ratio of 29.3x, the difference is minimal—less than 0.10—suggesting the stock is currently valued about right based on profits and future growth expectations.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1407 companies where insiders are betting big on explosive growth.

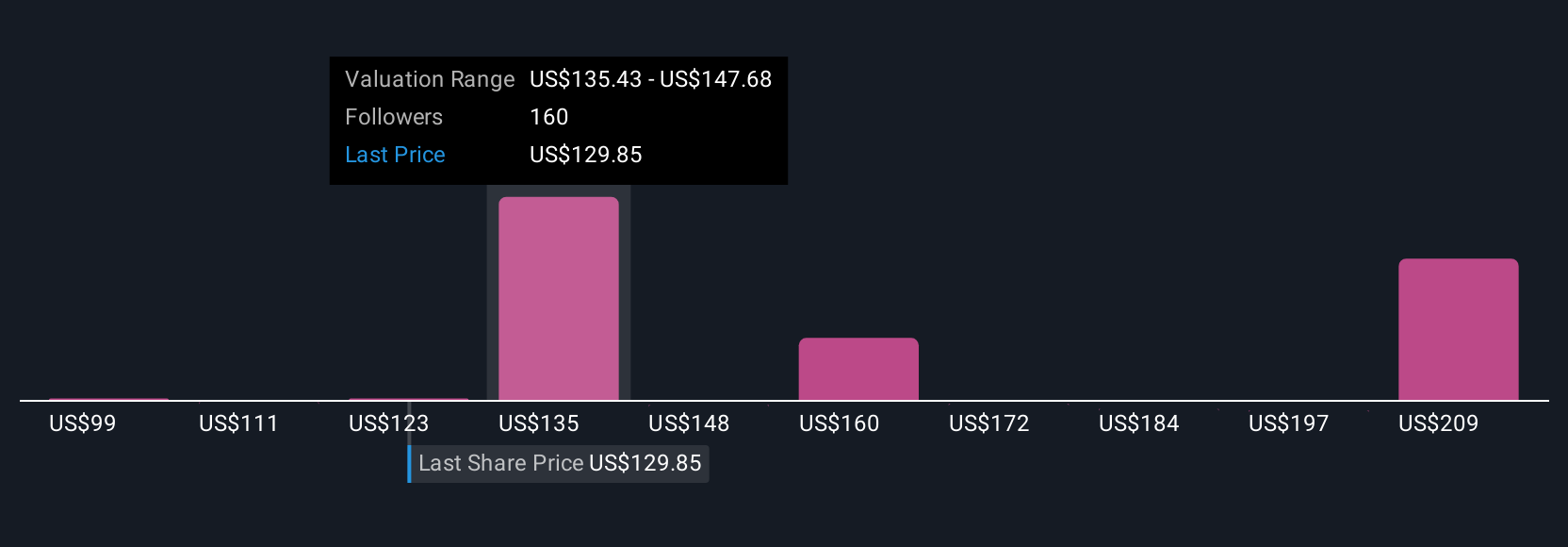

Upgrade Your Decision Making: Choose your Airbnb Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your own investment story, describing how you translate your view of Airbnb’s future into specific financial forecasts, like expected revenue, profit margins, and fair value. This approach grounds the numbers in real-world assumptions rather than guesswork.

Narratives go beyond just crunching numbers; they connect what you believe about Airbnb, such as how fast it will expand internationally or respond to new regulations, to a clear financial outlook and a justified price. On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors that let you build, share, and compare different stories for Airbnb. These Narratives are all updated automatically as new information surfaces.

By creating or following a Narrative, you can see how your fair value stacks up against Airbnb’s current share price, helping you decide not just what the company is worth, but also when you might want to buy or sell. Narratives are dynamic, constantly reflecting changes in news and earnings, so your outlook always stays relevant. For example, one Narrative assumes Airbnb could be worth $98 a share if risks weigh heavily, while another sees upside to $200 by factoring in international strength and product expansion.

Do you think there's more to the story for Airbnb? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.