Does Analyst Optimism on New Acquisitions Reframe Celsius (CELH) as a Portfolio or Integration Story?

Celsius Holdings, Inc. CELH | 35.25 34.48 | +1.15% -2.18% Pre |

- In early April 2026, analysts reiterated positive views on Celsius Holdings after its acquisitions of Rockstar Energy and Alani Nu, emphasizing the company’s expanding energy drink portfolio and distribution partnership with PepsiCo.

- An interesting angle is how this analyst optimism persists despite concerns around integrating the new brands and questions about whether Celsius’s valuation already reflects much of its growth potential.

- Now we’ll explore how this continued analyst confidence amid integration and valuation concerns may influence Celsius Holdings’ broader investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Celsius Holdings Investment Narrative Recap

To own Celsius today, you have to believe that its expanded energy drink portfolio, powered by the PepsiCo partnership, can keep attracting health focused consumers while the company manages integration costs and margin pressure. The recent analyst moves, including UBS trimming its target while keeping a positive rating, highlight that the key near term catalyst is still successful integration of Rockstar and Alani Nu, and the biggest current risk remains whether the stock’s rich valuation already prices in much of that execution.

The most relevant recent development here is Deutsche Bank’s upgrade after the stock’s 32.6% drop following Q3 results, even as it cut its target from US$56 to US$44 and flagged private label pressure at Costco. That combination of cautious targets and supportive ratings sits right alongside today’s debate around valuation and integration, and it matters because club channels and large distributors are central to both Celsius’s growth story and its customer concentration risk.

Yet behind the upbeat analyst views, investors should be aware of how quickly heavy promotional spending in club channels could start to...

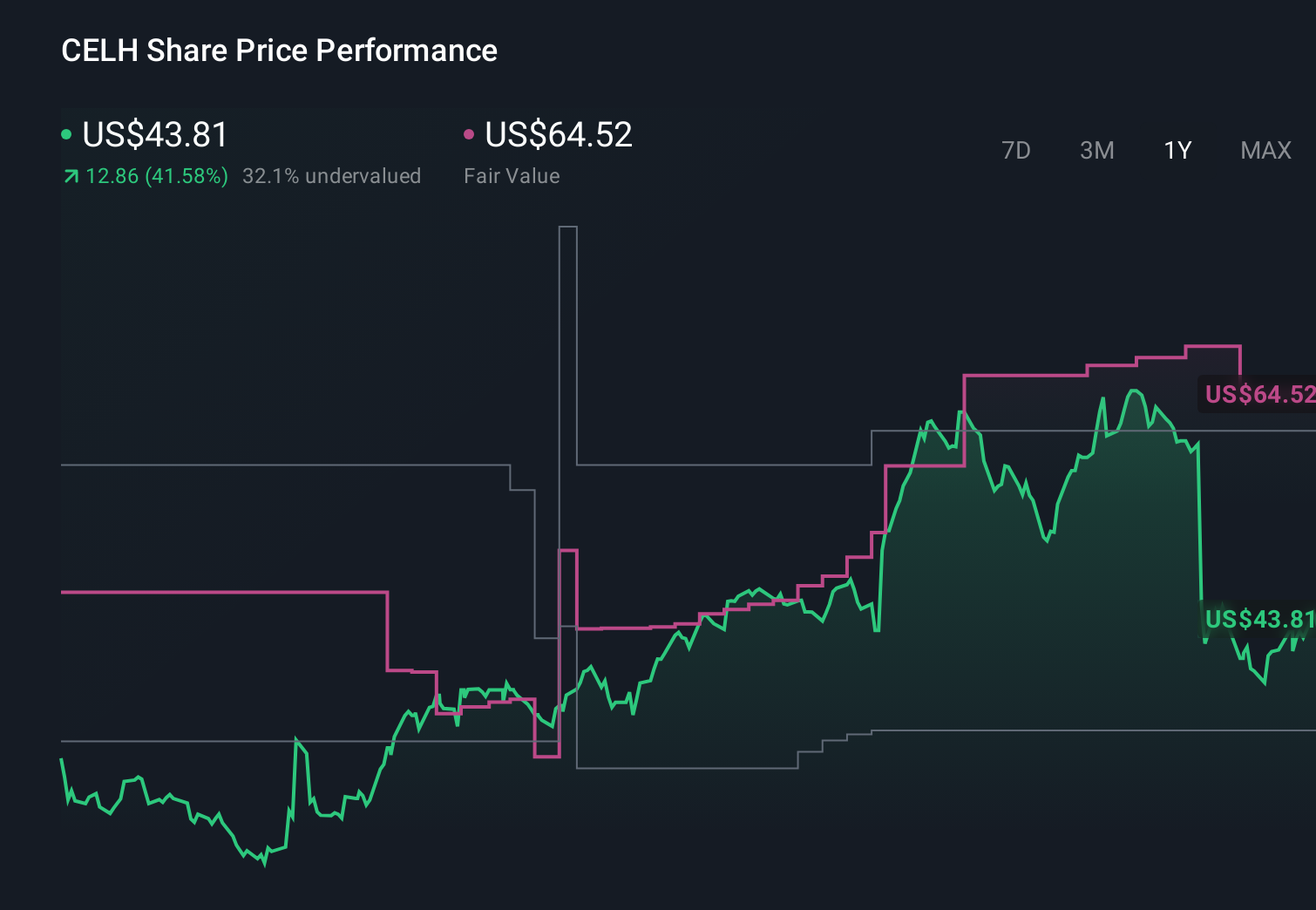

Celsius Holdings' narrative projects $3.7 billion revenue and $532.9 million earnings by 2028. This requires 30.1% yearly revenue growth and about a $437 million earnings increase from $95.9 million today.

Uncover how Celsius Holdings' forecasts yield a $64.00 fair value, a 76% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting revenue near US$4.5 billion and earnings above US$760 million by 2029, which is far more bullish than the baseline story and hinges on risks like heavy reliance on trend driven limited time flavors; with the latest analyst actions, it is a reminder that your own view may sit anywhere between these extremes and could shift again as new information emerges.

Explore 16 other fair value estimates on Celsius Holdings - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Celsius Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Celsius Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Celsius Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 64 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.