Does Analyst Praise For EMCOR’s Data Center Role Change The Bull Case For EME?

EMCOR Group, Inc. EME | 0.00 |

- In recent weeks, EMCOR Group has been highlighted as a leading provider of complex data center cooling and infrastructure services, drawing an Outperform rating from Oppenheimer and a Zacks Rank of #2 (Buy) on the back of an improving earnings outlook.

- This recognition underscores how EMCOR’s role as a comprehensive mechanical and electrical contractor for high-tech facilities, rather than a pure-play equipment vendor, is becoming increasingly important to analysts watching data center and critical infrastructure trends.

- We’ll now examine how EMCOR’s growing data center infrastructure exposure and supportive analyst sentiment could shape its existing investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe that its role as a full-service mechanical and electrical contractor in data centers, healthcare, and complex facilities can support a large, diversified project backlog and solid profitability, even as labor and project mix pressures remain key risks. The recent recognition around data center cooling aligns with this thesis but does not materially change the near term focus on executing its record backlog and managing wage and integration pressures.

The most relevant recent announcement in this context is EMCOR’s Q1 2026 update, where management raised full year 2026 revenue guidance to US$18.50 billion to US$19.25 billion and EPS guidance to US$28.25 to US$29.75. That higher bar sits alongside the data center driven optimism from Oppenheimer and Zacks, reinforcing how investors are watching whether complex technology projects can be delivered at targeted margins without aggravating labor cost and project concentration risks.

Yet behind the upbeat data center story, investors should also be aware of the growing risk that large, project based work could magnify earnings swings if sector momentum stalls...

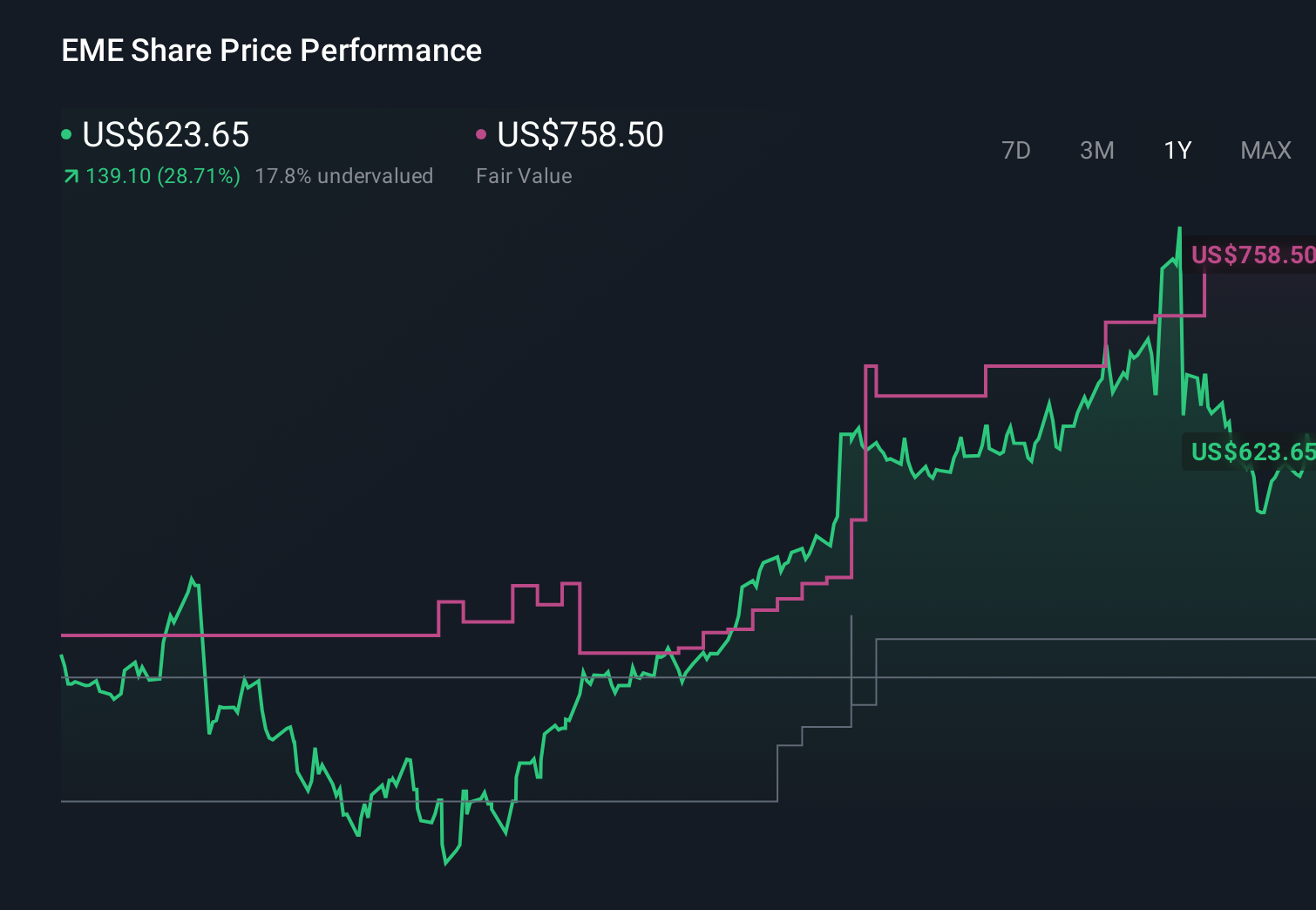

EMCOR Group's narrative projects $21.5 billion revenue and $1.6 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $983.50 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$21.2 billion and earnings of roughly US$1.6 billion by 2029, and their concerns about automation and prefabrication replacing traditional service work offer a useful counterpoint to the current enthusiasm around EMCOR’s growing data center exposure.

Explore 5 other fair value estimates on EMCOR Group - why the stock might be worth as much as 39% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your EMCOR Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.